2025: Year of Spice

2025 is shaping up to be a year of volatility...

Author’s Note: I will continue releasing free content where I can provide value to everyone. Posts will include premium content for paid subscribers at the end of emails or as separate write-ups. Free content will focus on macro views, whereas the paid content will focus more on the tactical trades I’m making.

Serious traders or investors should join Premium to get the best, most timely information.

2025 is here, and everyone is wondering, “What’s next for markets?”

December was a rocky month for the indices. The S&P500 and Russell 2000 closed down 2.6% and 7.5%, respectively. The Russell fell almost 10% from its high!

The Nasdaq was able to eke out a small gain but closed about 5% off the highs.

There have been small gains in January in the indices, with RTY barely leading the way.

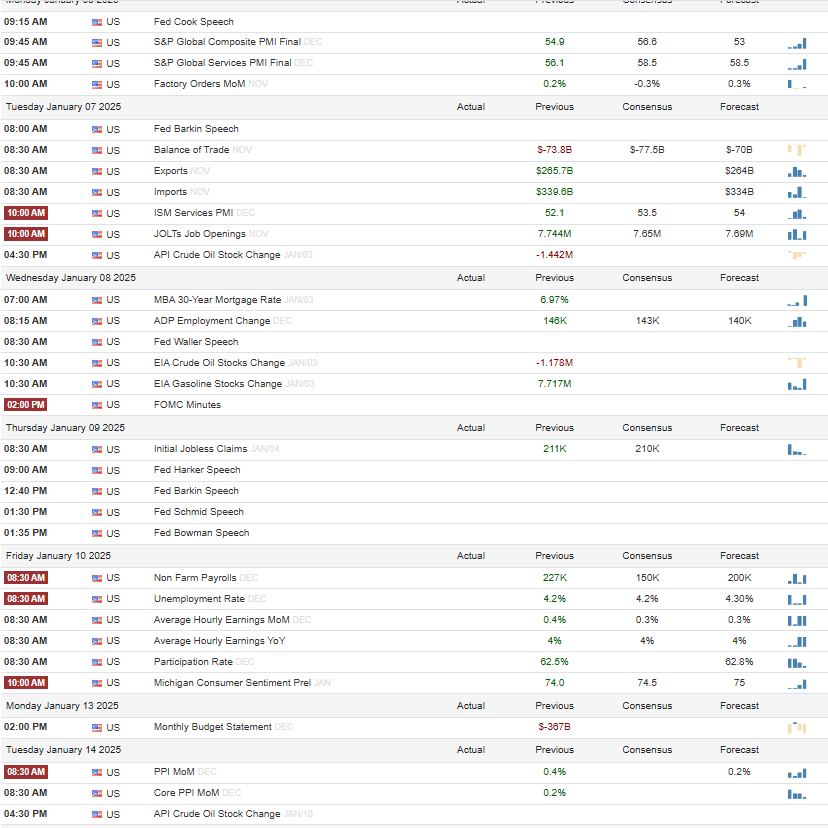

Next week is an eventful one. It’s the macro event of the season. It’s Non-Farm Payrolls again!

ISM Services on Tuesday and Non-Farm Payrolls on Friday will be key to watch. Because the last Fed meeting was especially hawkish, economic data is back at the forefront of the collective consciousness.

Soft, but not recessionary, data might well be bullish again because it will price in more Fed cuts.

Continued hot prints will reassure markets that the economy is strong, but they will also convey the impression that the Fed is continuing to be hawkish.

However, too soft data is still scary because it could signal recession!

Hence, we are entering another period of…

It’s So Over, We’re So Back

To say that “all eyes are back on the Fed and the economy” would be to imply those eyes ever wandered. They didn’t, but they are looking more sharply here in Q1 than in the Q4 post-Trump euphoria.

While all signs still point to a strong economy, I think we are in for more of 2024’s Q3 chop that characterized the last period of “It’s so over, we’re so back.”

What do I mean by “It’s so over, we’re so back?”

I mean that we are in for a period of volatile market PA that whipsaws on every piece of data.

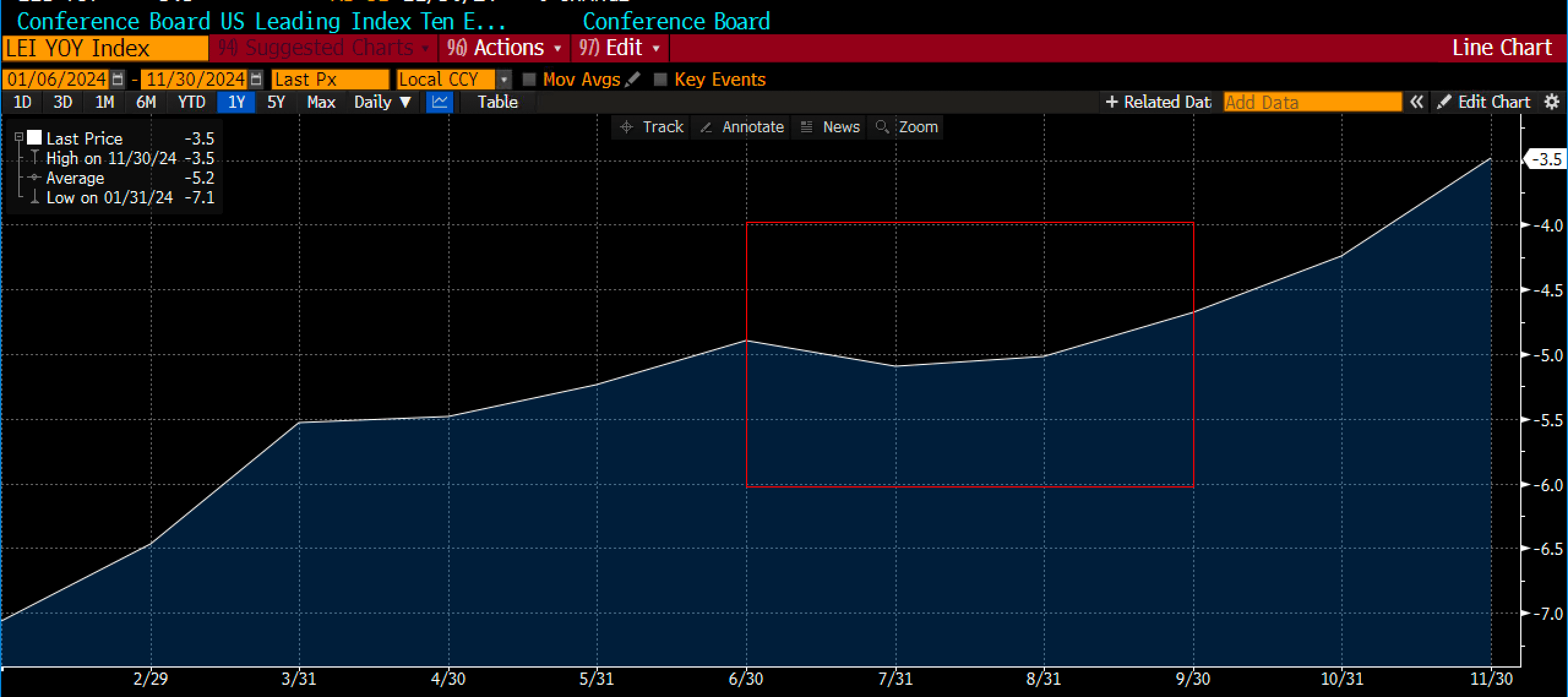

Looking back at Q3 2024, which we could categorize as a “growth scare,” we find that the indices had multiple substantial drawdowns.

In the Nasdaq 100 we saw a 16.5% and 8.5% drawdown in the July-September period.

This chart of the economic surprise leading index shows the “growth scare,” which I’ve marked in red.

The difference this time is that economic data has become much more robust.

However, with that robustness has come a resurgence in CPI.

This interplay between CPI and growth is at the heart of the Fed’s current dilemma. The Fed cut in September because it became worried about the growth scare, and it paused in December because it is worried about inflation.

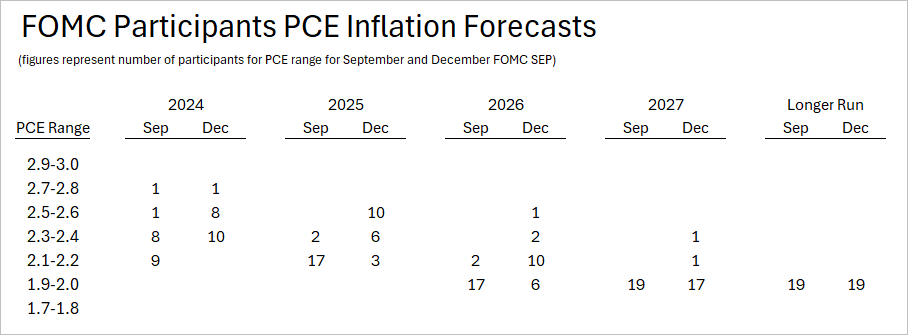

I already discussed this in my piece "Anatomy of a Market Crash," but I’ll review it again quickly. The biggest shock to markets in the December meeting came from the above chart of FOMC inflation forecasts.

Here’s a quote from my previous article.

Whereas previously, nearly all members expected inflation to return to near-target (2%) next year, now only 3 (!!!) do. Now, the vast majority don’t expect us to return to target or near-target until 2026, and even then, a handful think it won’t happen until 2027 or later!

This means the Fed, the markets, and the economy are back on the tightrope. While growth fears have subsided, we now have inflation fears to contend with again. While the Fed hasn’t said they’re worried about inflation, the chart above makes it clear that they are.

1990s Parallels

The biggest reason the Fed’s inflation expectations are spooking markets is best communicated with this chart below, borrowed from Citrini.

In the late 1990s, the Fed paused, and stocks and bonds both started ripping. Then, the Fed started cutting. Stocks kept ripping, but bonds started falling. Then, the Fed started hiking, and stocks came crashing down violently.

The market is worried about a similar sequence playing out today, and the Fed’s projections clued them in as to what the Fed is concerned about.

The events of the last few years have closely followed this analogy. In 2022, the Fed started hiking, and stocks and bonds both sold off. The Fed then paused its hikes, and stocks and bonds rallied. The Fed began cutting late this year, and stocks rallied to new highs while bonds sold off steeply. Now, the Fed has signaled it is ready to pause, and the rest remains to be seen.

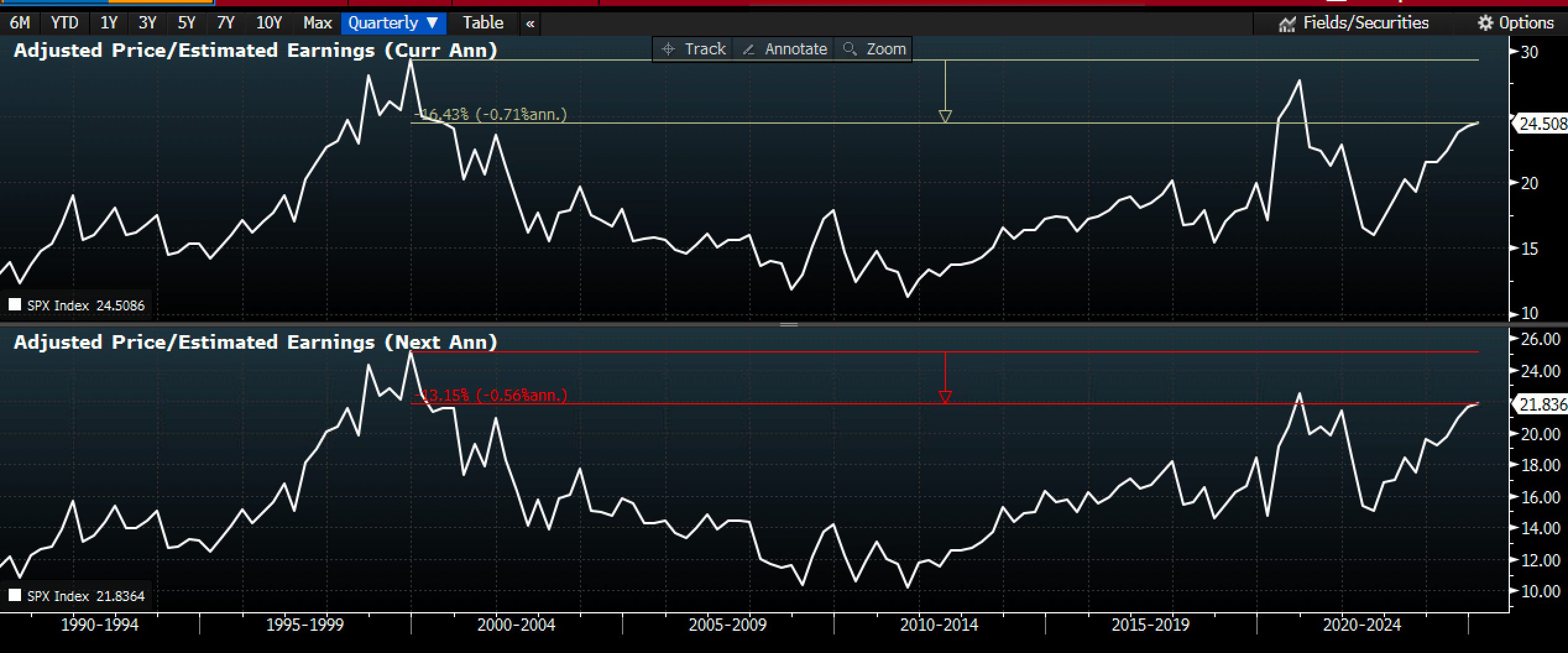

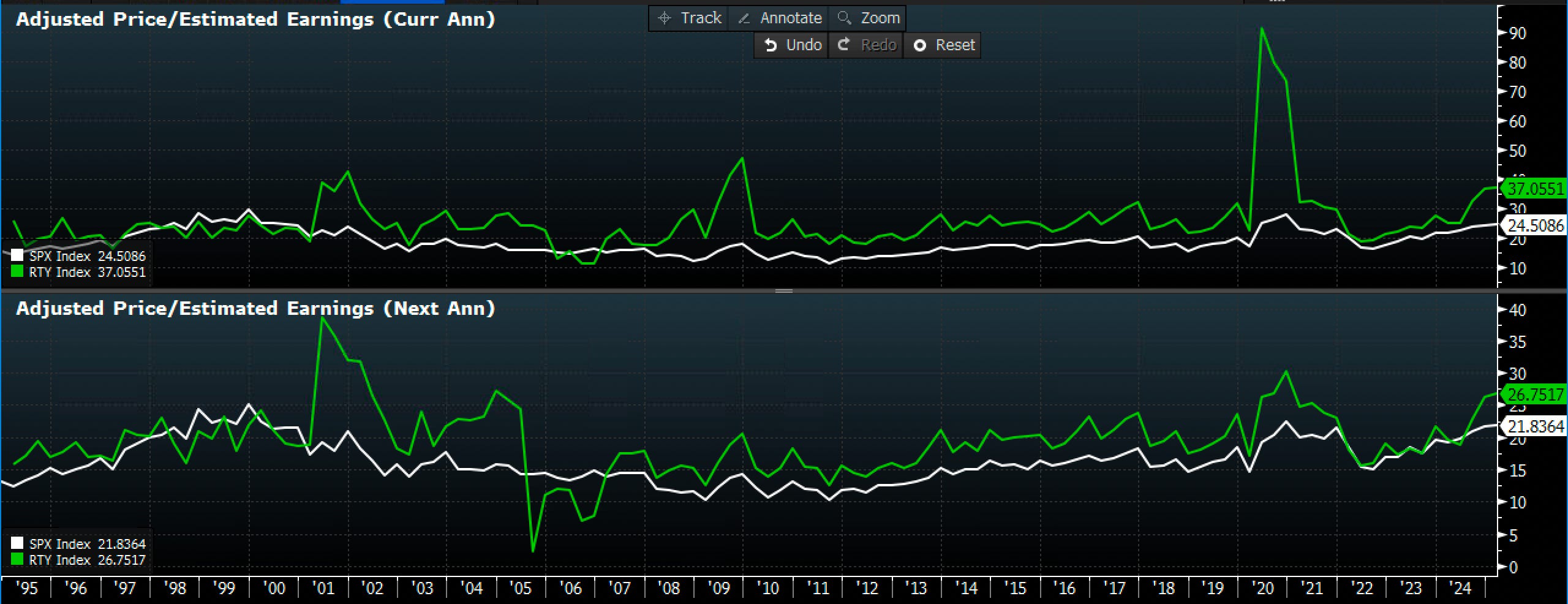

Let’s take a quick detour into looking at P/E ratios.

P/E Ratios

We are still off the highs of the dot-com bubble, but we are getting close.

While P/E ratios themselves are useless for timing the markets, they indicate where we are at in relative value.

And US stocks are expensive.

This makes stock valuations that much more sensitive to earnings expectations, which are themselves sensitive to the economy's growth.

In other words, while P/E values may not matter much today, they make stock prices especially vulnerable to a deterioration in the economy, which would likely cause both the P/E ratio and the earnings on which it is based to collapse.

A Crash In Need of a Catalyst

There’s a famous expression in markets that goes roughly like this:

That which cannot sustain, will not.

People have gotten complacent about the idea of owning US equities. They have returned ~20% a year for as long as people can remember.

But US stocks are reaching very expensive levels. As I mentioned earlier, with any hint of a slowdown in US economic excellence or corporate earnings they could be in big trouble.

That which cannot sustain, will not.

I was more worried about a crash as we rounded the horn on the end of 2024. It’s early in January and there may still be a big correction looming, but I’m leaning more towards expecting chop.

The problem with predicting a big crash is that there is always a catalyst needed. I thought the “blow off top” behavior in the markets in December combined with year-end weirdness might offer a catalyst.

I’m not sure what the catalyst might be in January. It could be a weak Non Farm Payrolls. It could be something none of us are thinking about.

Or it could just not come. Until it shows it’s hand there’s no way to know.

Year of the Stock Picker

Looking ahead into 2025 one thing is clear to me: 2025 is going to be the year of the stock picker.

We have had a long period of passive-investing where people have become accustomed to sticking their money in the index and watching it grow exponentially.

I think in 2025 there will be a lot of edge to be had in picking specific stocks. That’s not my forte, but we’ll be diving in head first.

In the immediate term I’m keeping my hedges (which took a beating Friday) and staying cautiously long. Boring, I know, but what else is a man to do in a market like this?

Good luck out there.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here. The information is presented for educational reasons only. Investment positions listed in the newsletter may be exited or adjusted without notice.