A Case For The Blood Being Over

Buy, Baby, Buy (?)

First of all, I’m sorry for triggering any PTSD by having to think about Sarah Palin again. I’m sure we are all happy to have that particular quirk of American history well behind us.

I’ve been thinking a lot all weekend, particularly today, about whether or not we are truly heading for a recession. Friday, the market and I were convinced of it. Now, on Grey Monday (as I’ve seen it called), it paradoxically looks much less likely.

To understand what’s going on, let’s start with the data we got last week and why it sent the market screaming for the exits.

Thursday and Friday Scaries

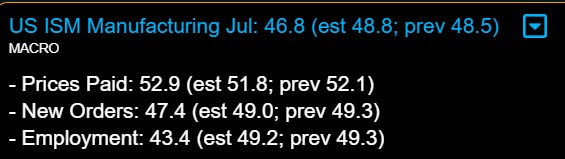

Last week, our first piece of bad data came from the ISM Manufacturing survey.

These numbers came in quite bad, and Employment was especially scary. The ISM indexes work on a scale where anything above 50 represents growth and anything below 50 represents contraction. Right away, this terrible employment number (way worse than previous) scared the market into recession fears.

For reasons you can all intuit, the economy really IS the job market. So, employment falling off a cliff would mean a certain recession.

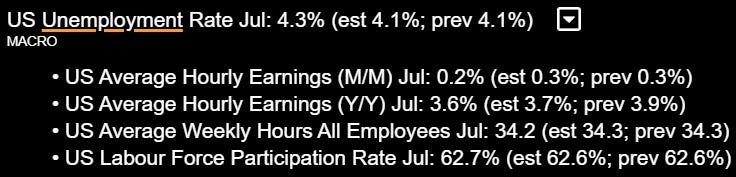

Then, on Friday, we got even worse numbers in the form of the unemployment rate.

That represented a big jump in the unemployment rate, reinforcing the idea that we must be imminently headed for a recession.

To make matters worse, it triggered what is known as the Sahm Rule, which says that a recession has begun when the three-month moving average of the national unemployment rate rises by at least 0.5 percentage points relative to its low during the previous 12 months.

Open the floodgates, sell, baby, sell.

Monday Confusion

Over the weekend, futures opened red and then sold off MASSIVELY on Japan fears. Somewhat quietly, the ISM Services index came out at 7 a.m. They were likely part of what caused the rally, although it’s unclear.

For one thing, this morning’s ISM services index came in above expectations. Of particular importance is the Employment number here.

Hotter than previous and MUCH hotter than manufacturing.

So, what gives with this conflicting data? Are we heading for a recession or not? Let’s take a look.

The Sahm Rule

On the surface, the Sahm rule triggering is very damning. It has a near-perfect track record, as you can see below:

The only time it missed was in 1959, but don’t worry—a recession started five months later anyway.

So that’s it, right? Sell, baby, sell is the dominant narrative, and now we all go to Hades?

Well, I’m not sure if that will remain the narrative, but I’m not so sure it’s the truth.

Digging Deeper

First of all, there’s some reasonable chance that the July unemployment data picked up on some distortions. I’ve read in a few places that the weakness may be partially attributable to Hurricane Beryl and auto plant disruptions.

Fed member Daly echoed that today:

So, it’s probably true to one degree or another. In fact, given that we just dinged the .50% rise in the unemployment rate that triggered the Sahm rule, perhaps it shouldn’t have triggered after all…

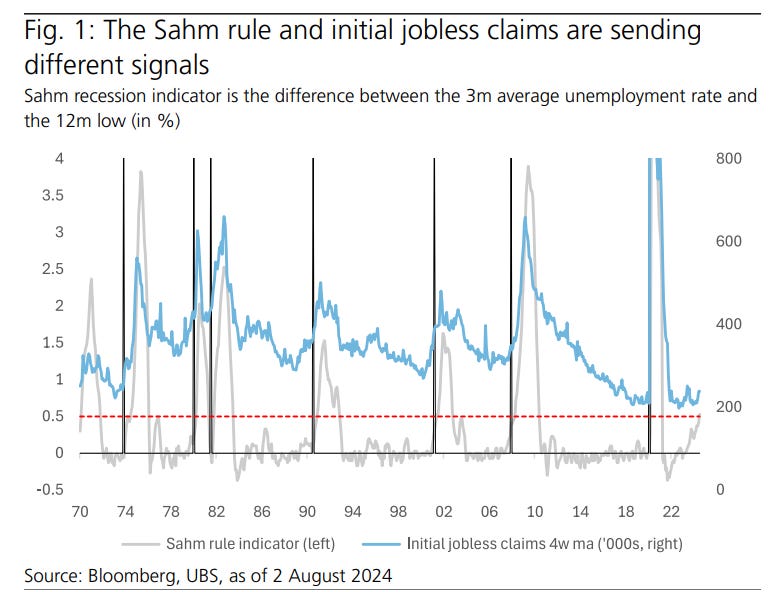

Uncertainty about the unemployment number aside, we can’t ignore the fact that it tells a radically different story than initial jobless claims.

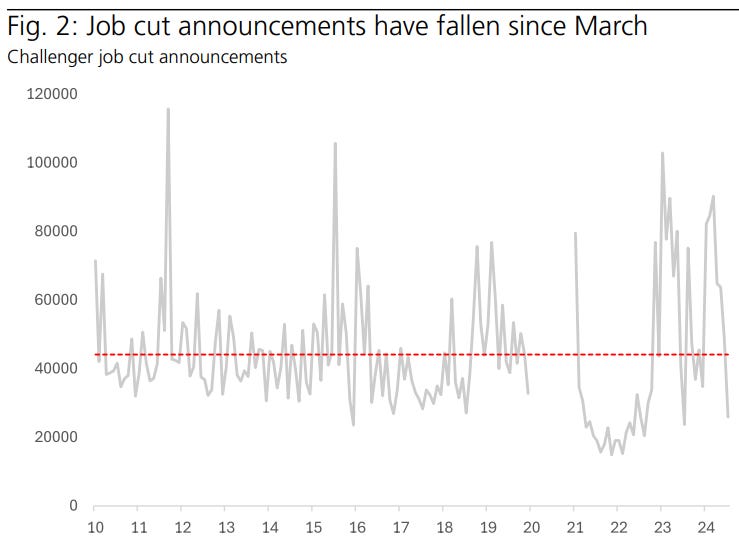

Furthermore, job cut announcements have actually fallen since March.

The implication is that not many people are actually losing their jobs because jobless claims aren’t rising to match the unemployment rate, and companies aren’t cutting jobs.

I’ve seen an explanation for this discrepancy: the massive surge in immigration this year. It's plausible, at least.

So, how bad are the employment numbers? Mixed, at least, and possibly encouraging. They are certainly far from screaming “recession.”

These insights have been enough to return my base case to “soft landing,” although I think it’s important to stay vigilant.

How The Market Will React

First, it’s impossible to guess how the market will react. Is the market capable of digesting the subtleties of the job reports?

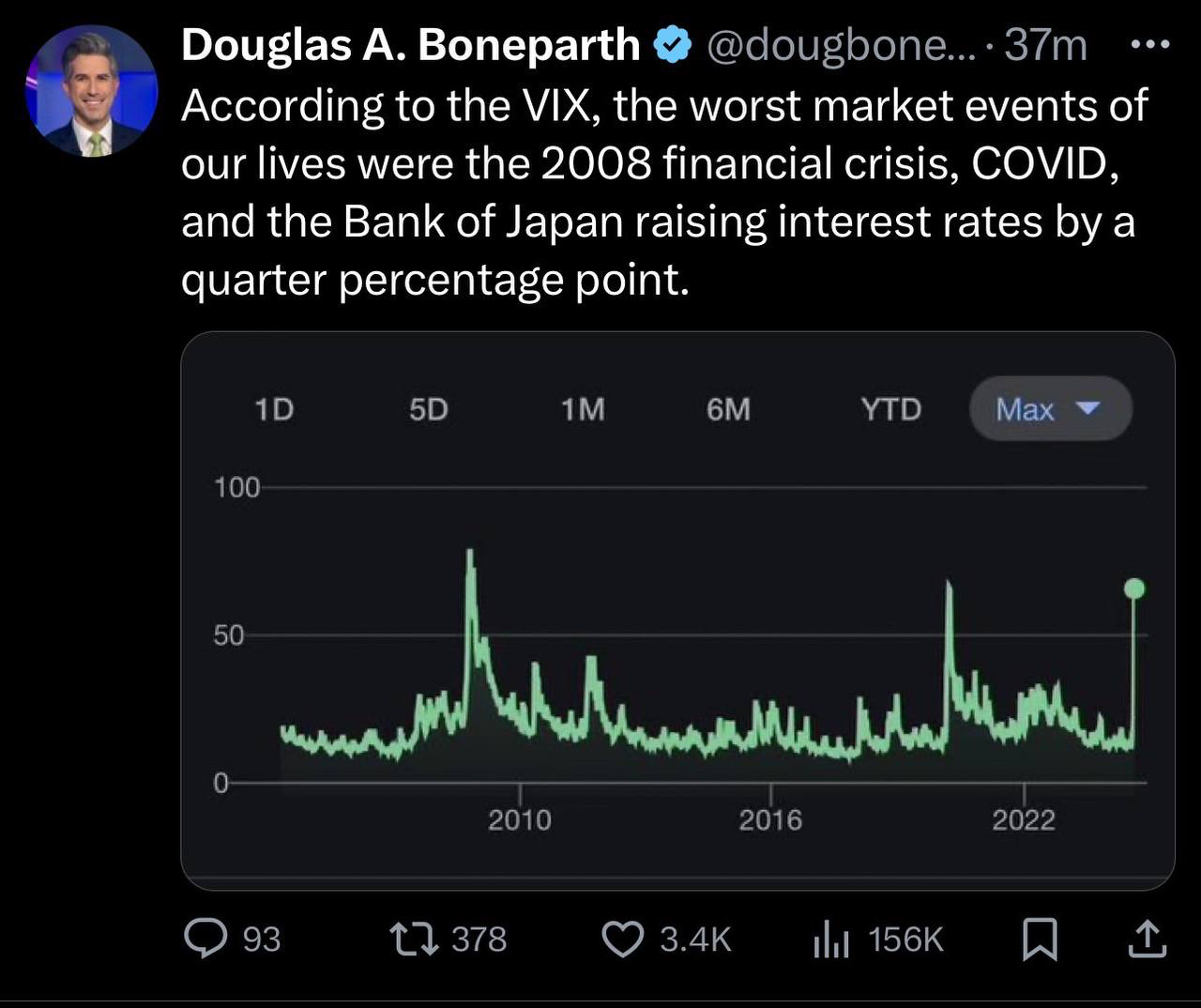

I don’t know. But what I do know is that we had one of the biggest VIX blowouts we’ve ever seen, on par with the 2020 crash and the 2008 financial crisis, fueled by poor jobs data and a crash in the Nikkei.

To steal a tweet from my previous post:

Does that seem proportional to the reality of the situation? I don’t think so. The only thing that could be bad enough to deserve it is if the Japan implosion is going to really blow our socks off in a way we don’t understand yet…

Which is possible. In fact, there are a lot of things that could blow our socks off, which is why I’m generally encouraging you all in each post to lower your risk tolerance for the foreseeable future.

But is the Yen/Japan going to be the thing that does us in?

Troubles in the Yen

As I write this, Nikkei futures are limit up—up more than 7% after falling 12% today. It feels like it might well end up being… a nothing burger?

Famous last words? Maybe. But when you’re staring at all this information compiled in one place, what’s the rational takeaway?

On this one in particular, please remember that I’m not a financial professional and this isn’t financial advice. I’m quite literally a moron who is just doing his best. Please make your own educated decisions, DO NOT outsource your critical thinking to me.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here.