A Correction For Ants?

Another leg higher...

Author’s Note: I will continue releasing free content where I can provide value to everyone. Posts will include premium content for paid subscribers at the end of emails or as separate write-ups. Free content will focus on macro views, whereas the paid content will focus more on the tactical trades I’m making.

Serious traders or investors should join Premium to get the best, most timely information.

Hello everyone.

Equities pushed to fresh highs before a modest pullback. Despite softer labor signals and stretched multiples, positioning remains light—last week’s de‑grossing leaves room for a “surprise” leg higher into Q4. A firmer dollar is a swing factor: it tightens conditions, but with underexposed “smart money” and potential Fed easing ahead, the path of least resistance may still be up.

Below: the positioning, the policy setup, and what would change my mind.

My last post about taking down risk led into a few months of chops, but since then equity markets have continued higher.

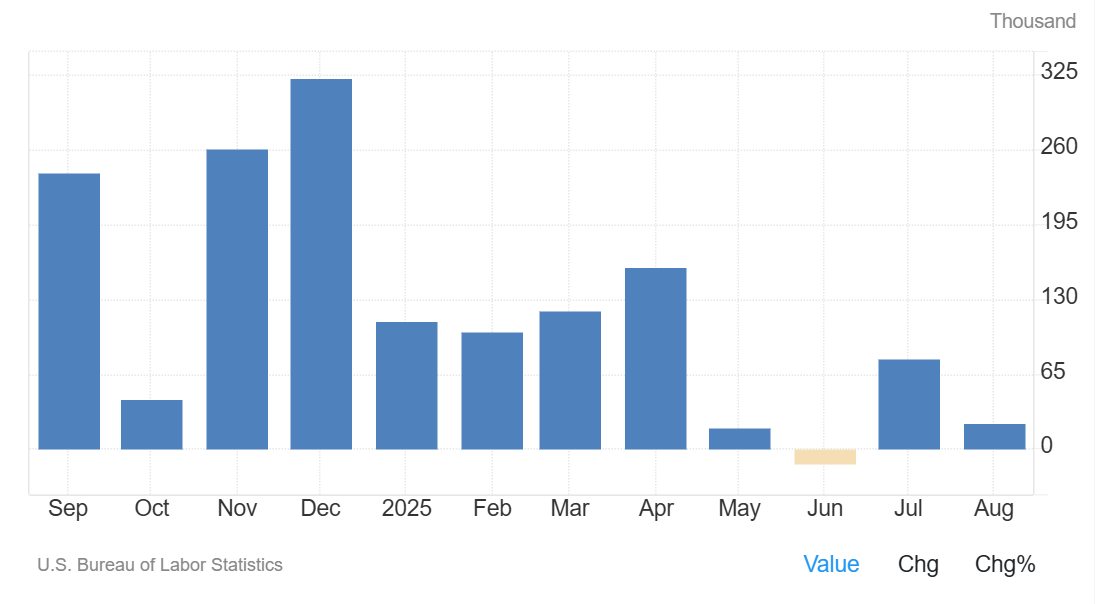

I’ve found the market a bit hard to read the last month or so. On the one hand the jobs data has clearly deteriorated to near-recessionary levels.

While P/E ratios have been breaking out to historical highs.

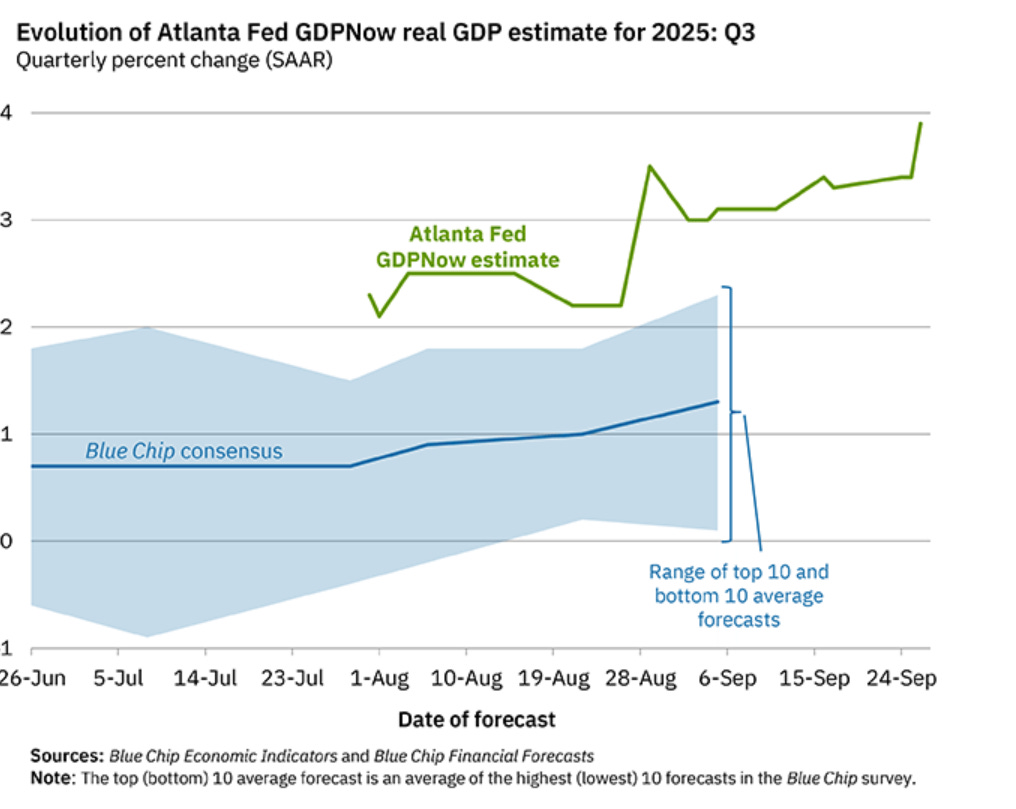

But GDP growth projections have also remained extremely high.

So there hasn’t been much in the way of slam-dunks in US equities as far as I can tell.

However, I believe that’s changed…

A Correction For Ants

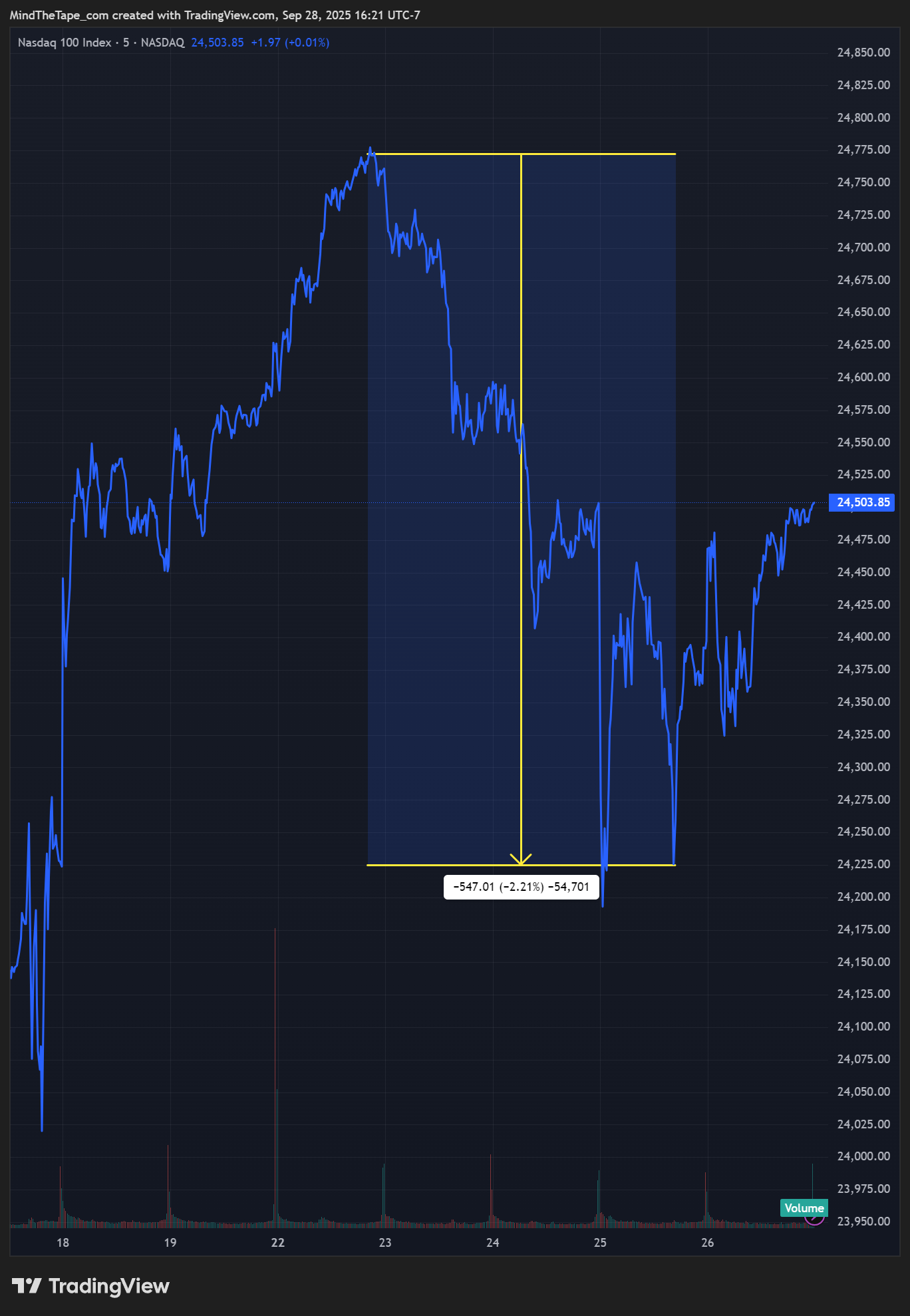

NDX and SPX both made new highs last week before selling off.

The actual size of the sell off was quite small. Like all of the post-TACO (Trump Always Chickens Out) dips have been.

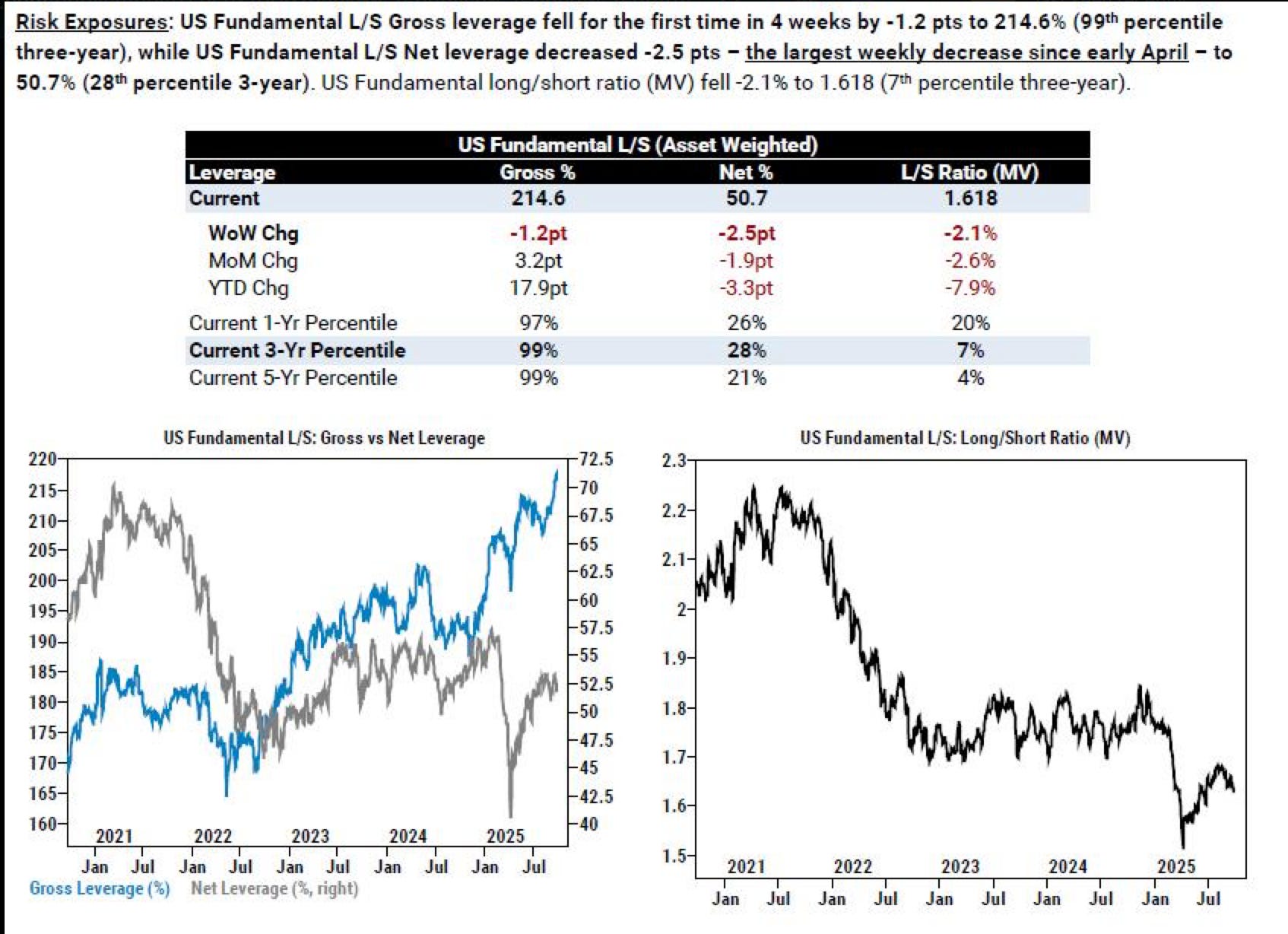

The market structure of this rally has left smart money relatively under-exposed the whole way up. That has kept the dips shallow. Notably, last week saw a significant de-grossing on equities down to quite low levels.

Also, the DXY seems to have bottomed, and might be looking for another leg higher.

These two factors, particularly the gross/net exposure numbers, lead me to think we are going to get a “surprising” move up from here, possibly all the way through Q4.

One thing I am watching is month/quarter-end in the first few trading days of next week. There are a lot of pension funds who will be looking to rebalance out of equities. I believe some of that has already happened, and I don’t expect too much turbulence, but the possibility is there.

The Mother of All Asset Bubbles

The Fed appears ready to re-begin their easing cycle while US indices are at their ATHs.

Since 1995 there have been three instances where the Fed has cut with the NDX ~at all time highs.

One in particular, 1998, stands out for culminating in the Dot-Com Bubble.

The Dot-Com Bubble itself was characterized by low or no revenue internet companies reaching insane valuations. This happened because:

1. There was a promising new technology for investors to get excited about.

2. Interest rates were lower than the neutral rate creating artificially loose financial conditions.

Is the stage set for something similar?

Monetary Illusions

There is a growing “soft” crisis of confidence in the US dollar. The average consumer is painfully aware of how vulnerable their purchasing power is, to the point where even your local uber driver knows (consciously or intuitively) that they’re expanding the money supply at a scary rate (6.5%/year over the last 20 years).

This is a large part of why Gold has been on such a tear for the last few years.

I don’t have any fancy data or articles for this point, but I think this contributes to setting the stage for an epic asset bubble. People are primed to believe stocks only go up, and they are looking for something to do with their ever-devalued paper.

Combine that with loosening financial conditions and Fed cuts… it’s hard to stay out of the pool for long when it comes to investing.

What I’m Watching

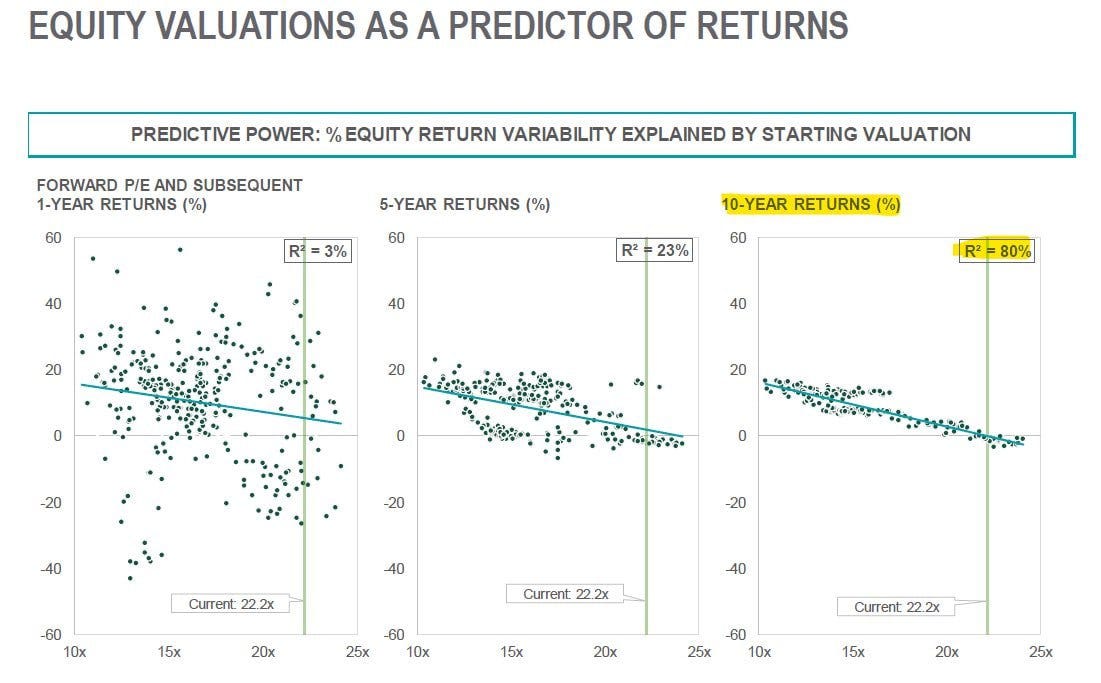

There are obviously concerns around valuation. Valuations don’t predict crashes but they do have an influence on forward returns.

In order for US equities to continue their march higher these main factors must persist:

Positioning has to remain constructive. Once it gets stretched the “marginal buyer” has already bought and we are likely to stagnate.

Inflation has to stay “relatively” subdued to permit Fed easing.

The economy can’t weaken fully into recessionary territory.

The fiscal spigot has to stay on.

Point #4 is particularly interesting in the context of next week’s “government shutdown” negotiations. Trump has threatened to fire thousands of Federal workers if a deal isn’t reached.

There is some chance that this shutdown debate crystalizes around some measure of fiscal responsibility. While I find it unlikely that anything meaningful will come out of it, that’s something to watch for this week.

Obviously this Friday we also have Non-Farm Payrolls. Pay particular attention to that data print and any August revisions. We are in the danger zone around jobs, so while I think the market is prepared to be forgiving any especially cold data could raise alarm.

I’m going to try something different this week. If this post gets 10 likes I’ll give away an annual sub.

Good luck out there.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here. The information is presented for educational reasons only. Investment positions listed in the newsletter may be exited or adjusted without notice.

Good read, thanks!