Are You Having Fun Yet?

The Fun will continue until morale improves...

Author’s Note: I will continue releasing free content where I can provide value to everyone. Posts will include premium content for paid subscribers at the end of emails or as separate write-ups. Free content will focus on macro views, whereas the paid content will focus more on the tactical trades I’m making.

Serious traders or investors should join Premium to get the best, most timely information.

I’m on vacation this weekend so going to keep this one a little short, but I do have some ideas/thoughts I want to convey. I hope they’re helpful.

Well, we bought the “dip” too early, and now all your favorite Finfluencers are convinced it’s the end of the world and the start of the next great bear market.

I link those articles to illustrate my point, but they are also worth checking out. Both Kevin and Shrub are some of my favorite reads.

Markets sold off in a zig-zag pattern this week with the Nasdaq 100 just below its 200 DMA after a failed breakdown Friday.

The SPX followed a very similar pattern but, in contrast, it managed to hold onto its 200 DMA.

For the first time in a very long time, everyone is seriously watching these 200 DMA levels for a clue as to whether “it’s so over” or “we are so back,” which should tell you all you need to know about the state of market participants’ sanity.

Nevertheless, the 200 DMA is a key level for a lot of money and there is a real risk of a cascade if we lose it in the SPX. The fact that we held it after a look below, and fail is a good sign. That might read like a bit of a tautology: the fact that we didn’t go lower is bullish, but there’s more to it than that. We didn’t get the liquidity cascade people were concerned about, and in not getting that, we showed buyers (who were concerned about that cascade) that it’s safe to buy here.

The Macro Picture

Somehow we find ourselves in the middle of a growth scare narrative that, combined with tariff uncertainty, is really rocking US markets and their claim on global superiority in a way I haven’t seen in a very long time.

I believe that this narrative is wholly unwarranted by the data, so I’m going to quickly try to explain why with a series of charts.

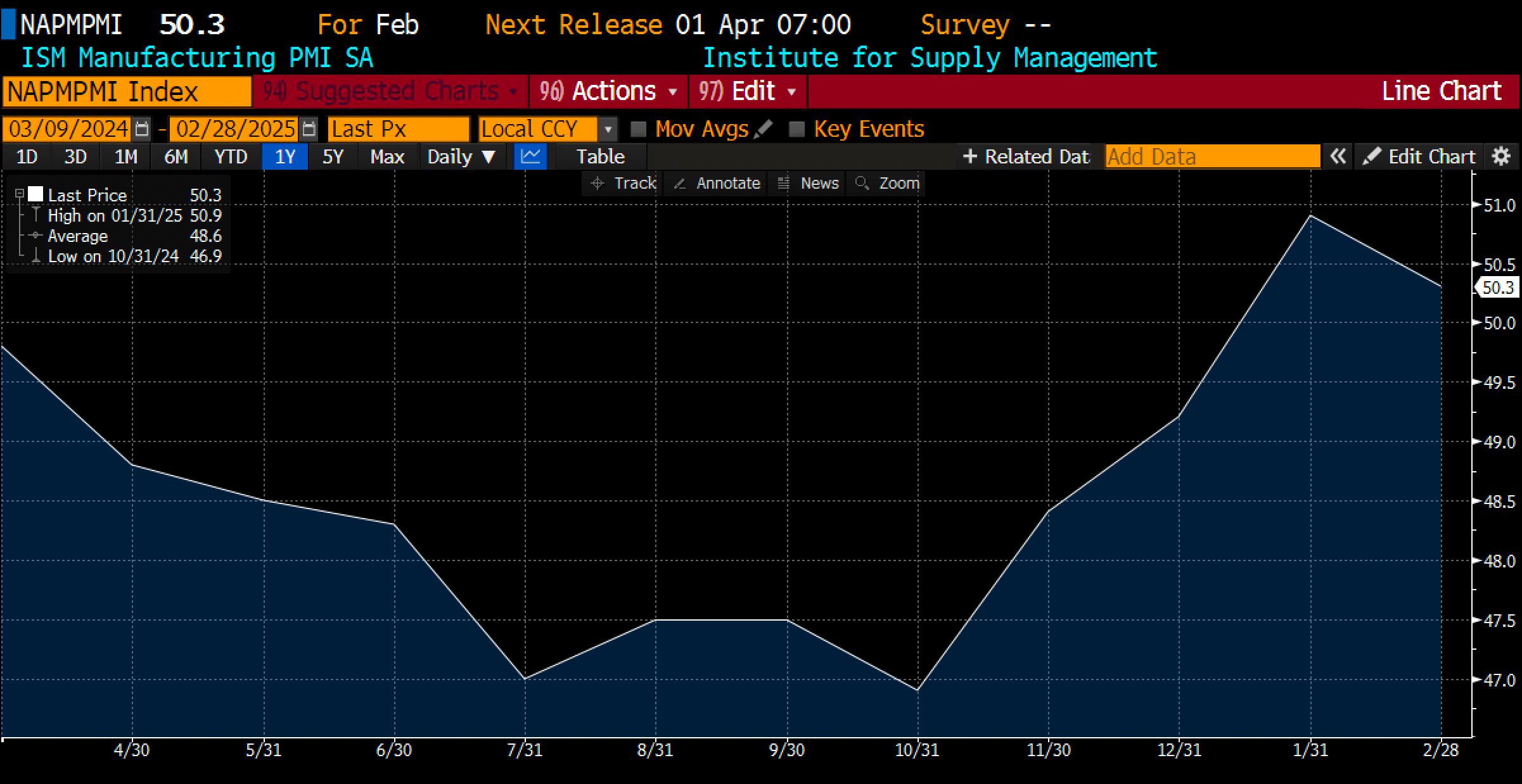

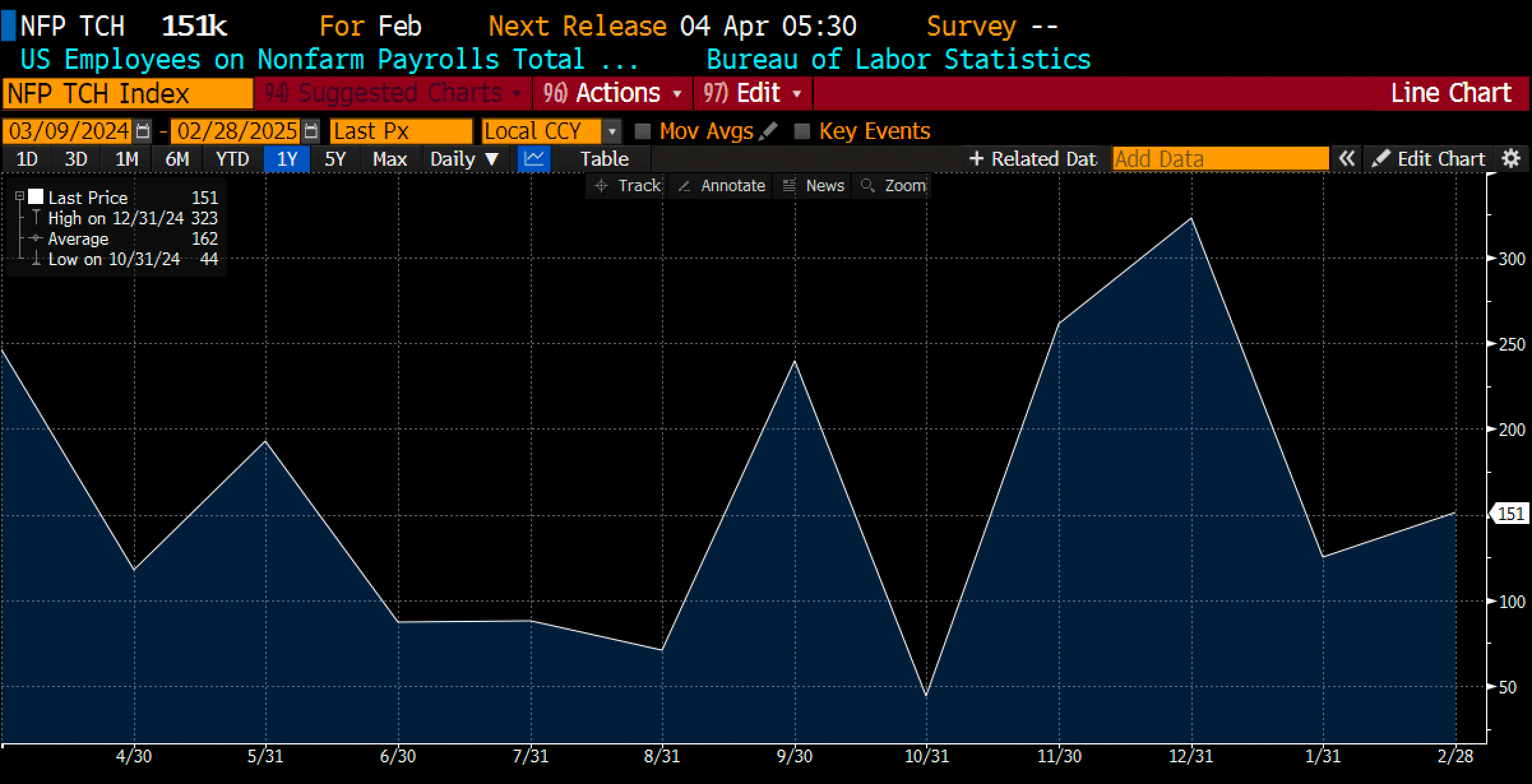

These first three charts should be pretty self-explanatory. They are big, headline economic numbers that don’t show any slowdown.

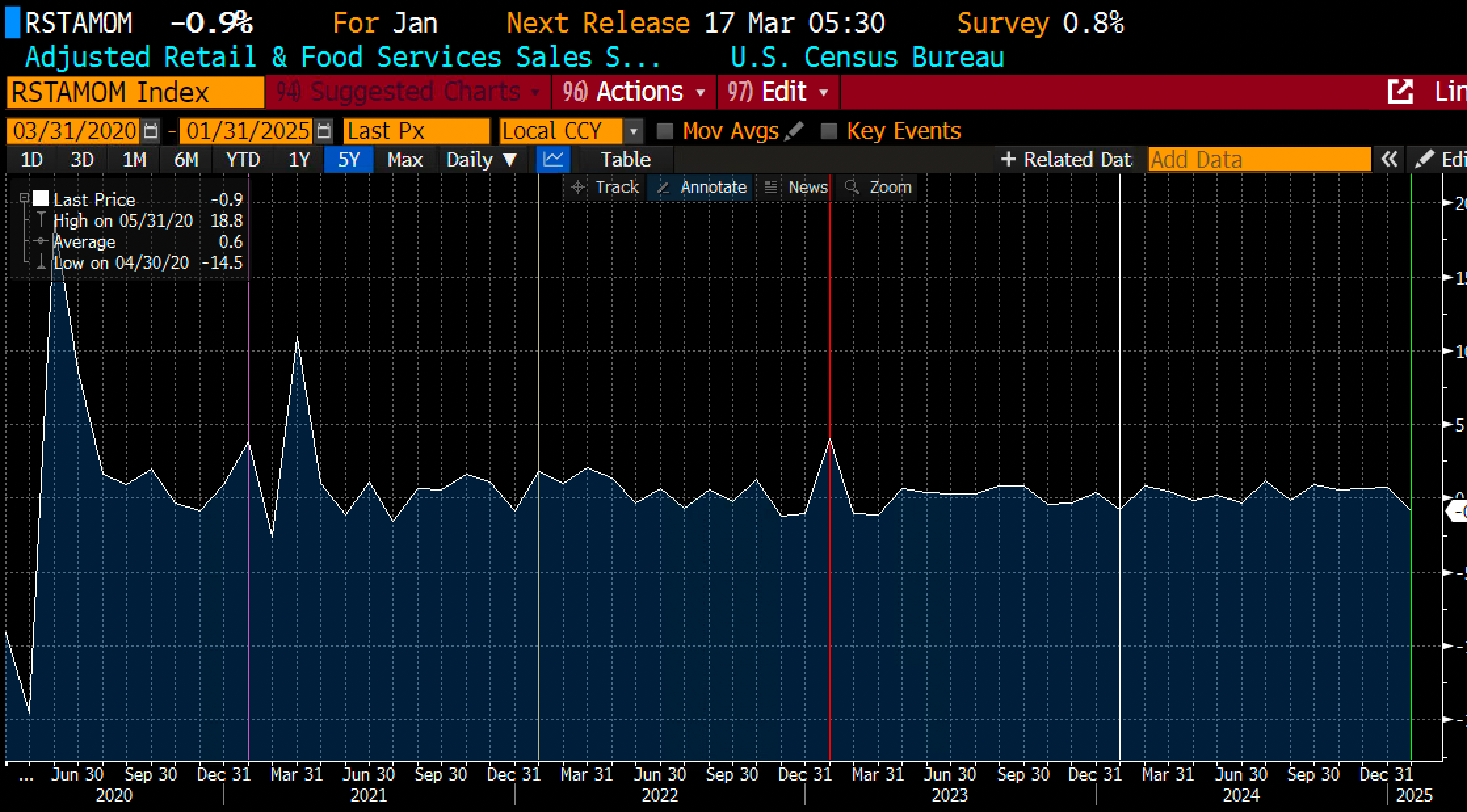

This next chart is a little more nuanced. It’s the chart of retail sales (ex-autos) over the last 5 years, with Januaries highlighted. I did this just to show that January is an extra noisy month, and to show that the print was fairly in line even if it wasn’t great. This print is also easily explained by “bad weather.”

We are not seeing deterioration in the economy in any major way yet. Calling for a recession here is no better than calling for a recession at any random time, as far as I can tell, unless you believe Trump intends to start an incredibly destructive trade war with the world. I don’t.

Even if you are convinced we are seeing a recession, you have to acknowledge that we are in an incredibly early phase of it (IE it’s not happening yet), in which case two very stimulative things have happened that might head it off:

Both the oil price heading to the lows (left axis) and the 10y yield heading to the lows (right axis) are stimulative for the economy. With regard to yields, they are stimulative to the very sectors that have been seeing the most alarming data (housing, autos).

The conference board’s leading indicator index is no worse than most of last year.

This all leads me to a single conclusion…

The growth scare is not real.

Does it have to be real?

So given that the growth scare is not real, and is instead fully vibes based, where does that leave us? Is this a train to step in front of?

Not necessarily.

The Trump administration has been carefully repeating for all the world to hear some variation of “there is no Trump put” (Bessent, on Friday) and “we aren’t even looking at the stock market” (Trump himself).

Market prices are based on flows, and flows are based on vibes. Enough negative vibes surrounding the markets could be enough to fly in the face of any economic hard data and send the market lower. The very act of sending the market lower would be enough to then turn the hard data downward, and create a self-fulfilling price cycle.

It is very clear that a main priority for Bessent is taking the 10y yield lower.

Stephen Miran, Trump’s head of the council of economic advisors, wrote a paper in November of last year that lays out a plan for doing just that which involves tariffs.

It’s a must read, and can be found here.

To summarize:

We implement tariffs.

We threaten to withdraw from our world police role.

We use the tariffs and withdrawal threats as negotiating leverage to get other countries to buy long dated debt from us at low rates.

In this way, we solve the US’ debt problem.

Getting 10y yields lower is part of this equation.

All of this to say there is something happening in the background here that is real and worth watching. I don’t personally fully know what it is yet or how it will manifest in markets.

The AI Boom

All of this is made even more confusing for equity prices because it is happening against the backdrop of an inflection in the AI progress cycle.

The Chinese have released a fully autonomous agent that appears capable of doing a variety of “white collar worker” tasks. That might sound bearish at first blush (China, etc) but I view it as incredibly bullish.

Demo: https://x.com/mckaywrigley/status/1898756745545252866

The major AI companies in the US' are working on this tech and I don’t expect them to be behind China here. Nothing about the Manus method seems especially proprietary.

That means we might well be months away from the “white collar worker in a box” that I’ve been predicting.

In a world where that exists, is being sold by companies like Amazon/Microsoft, and the US 10y yield is below 4%, are these companies not incredibly valuable?

I think they undoubtedly are, it’s just a question of how much pain the market forces on us before we get there.

Good luck out there.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here. The information is presented for educational reasons only. Investment positions listed in the newsletter may be exited or adjusted without notice.