Dawn of the Second Week

The second "full" trading week of 2025 dawns

Author’s Note: I will continue releasing free content where I can provide value to everyone. Posts will include premium content for paid subscribers at the end of emails or as separate write-ups. Free content will focus on macro views, whereas the paid content will focus more on the tactical trades I’m making.

Serious traders or investors should join Premium to get the best, most timely information.

Well, 2025 has been exciting so far. The indexes pumped up big in the first few days of the year and then gave back those gains and more.

This puts the indices below or approaching 5% drawdowns from their highs in mid-December.

Mag7 is off the highs, too, but, except for Tesla, they haven’t felt a disproportionate amount of the pain so far.

In fact, if you go back to December 1st, they are all still up since, or at least close to it.

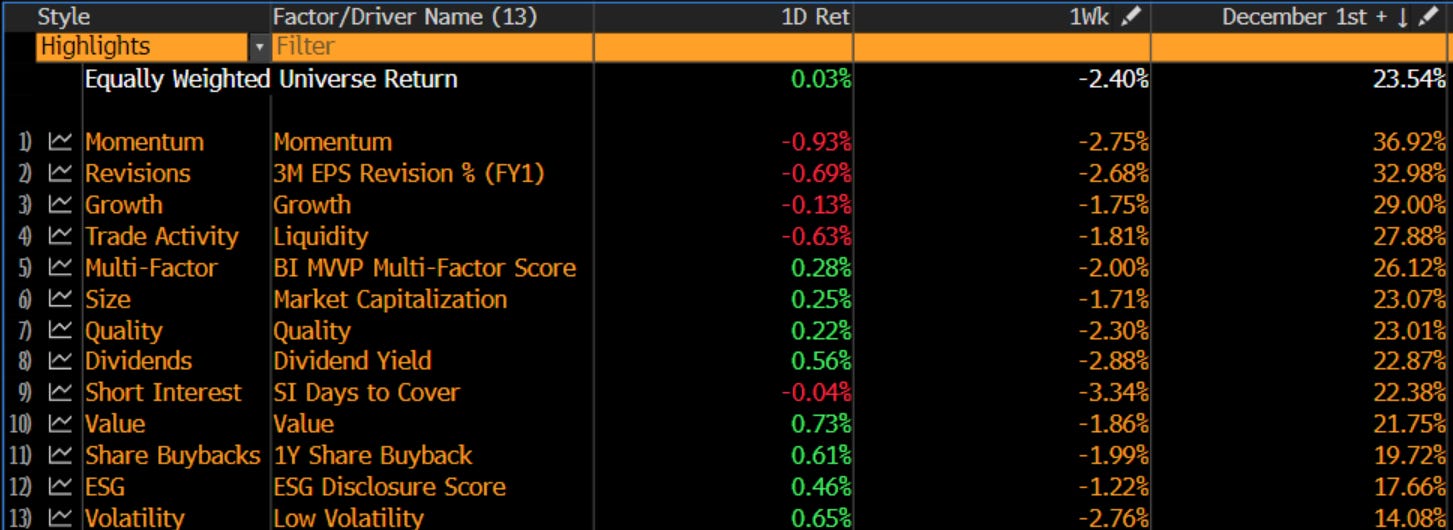

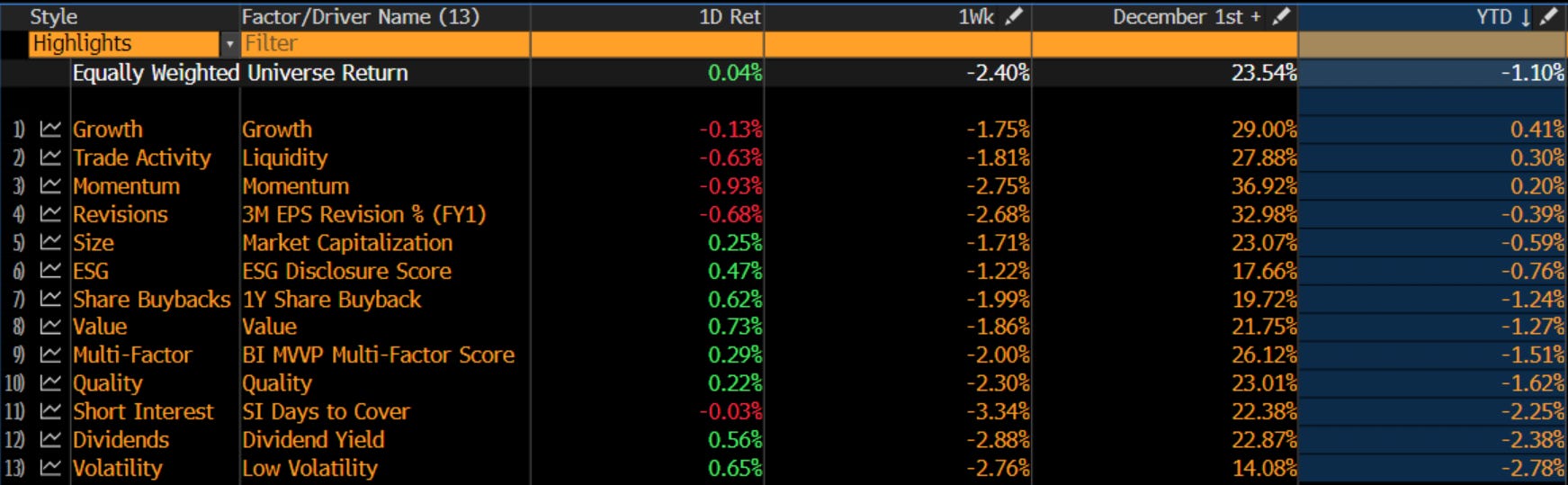

One thing we’ve been checking in on a lot lately is which factors have out-performed and which have underperformed. Below are the factor highlights. I’ve sorted them by performance since December 1st and then YTD.

I’ve written before that to really believe that we have shaken out the animal spirits and that the worst of any correction is over, I would want to see momentum lag or reverse. These charts make it clear that it hasn’t. Momentum was the top performer in December and is still close to the top in 2025.

I want the quant funds to manually turn off their momentum-following bots to signal a capitulation event. We are nowhere near that yet.

That said, this doesn’t mean we can’t bounce, and it doesn’t mean such a capitulation is imminent! There is much more going on than just these momentum funds distorting the market, particularly in bonds.

Taper Tantrum Redux

Treasury yields have been marching ever-higher in Q4 and into Q1 2025, even as the Fed began a short-lived cutting cycle last year.

Anyone who tells you they know exactly why bonds are selling off like this (yields spiking means bonds are selling off) is lying. It’s a mixture of factors, and it’s not totally clear how much each matters. The factors, in no particular order, are:

A strong economy has caused the bond markets to price out Fed intervention in 2025, allowing them to keep rates higher.

Hotter-than-expected inflation has also contributed to the markets pricing in fewer Fed cuts. Essentially, with a strong economy, the Fed can afford to stay restrictive to try to stamp out the last vestiges of inflation.

The US Government has a credibility problem regarding fiscal responsibility. The bond market is waking up to the fact that the United States has little hope of ever repaying its debts without significantly devaluing its currencies. Therefore, the bond market demands higher premiums to continue lending to it.

Of all three of these concerns, the last one is the most mysterious and troubling.

As FedGuy12 says, the funny thing about the bond market is that it is self-correcting. Higher rates should slow the economy, lower inflation, and eventually encourage the Fed to ease and add liquidity.

That is, unless the credibility concern becomes mainstream. In that case, we are likely to see a prolonged temper tantrum in bonds that drags down equities until lenders are assured that the US Government is “good for it” regarding paying its debt.

In any case, high bond yields tend to correlate with equity underperformance. So, as long as bonds continue to sell off, we are unlikely to see equities reverse course significantly.

Macro Events

With so much focus on bonds and the economy, again, it’s looking like a case of the It’s So Over, We’re So Back (ISOWSB) market I’ve been writing about. In an ISOWSB market, every new econ print is the most critical print ever, and this week’s prints are no exception.

PPI tomorrow and CPI Wednesday have the power to affect inflation expectations, which could directly impact the bond sell-off.

I think we are getting close to pricing in max-fear in bonds, at least in the short term. It’s not that bonds can’t go higher; I just think the speed and steadiness at which we’ve priced them to this level implies a lot of negativity around them. What would it take to surprise bonds to the downside at this point?

I don’t know, and hopefully, I won’t have to find out.

My Trades

I’ve been fairly well-hedged for the last six weeks, but my portfolio has ground down despite this.

Not fun.

I’ve been preaching caution since early December after taking maximum advantage of the November election rally. We’ve traded well.

This morning, I longed ES and crypto for a trade and closed some of the hedges.

I am very hesitant going forward and am staying cautious. I don’t expect to find fat pitches for a while, but I will post them here when I do.

Good luck out there.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here. The information is presented for educational reasons only. Investment positions listed in the newsletter may be exited or adjusted without notice.