Did you buy the dip, Anon?

A look at what the markets did and where they might be going.

It’s been a whirlwind August, with lots of opportunities to get hurt. I hope you’ve been following my posts, especially Threading The Needle, as I’m proud to say we’ve navigated the chaos well. If you missed it, I more or less predicted the clean sweep of economic data and geopolitical events we had last week that have positioned us for the “Goldilocks of all Goldilocks” outcomes.

It closes with, “I think the ingredients are right for a violent and sustained rally.”

The question now: “Is the rally a thing of the past, or are we in for more fun?”

Let’s look at some of the important signals available in markets to see if we can make good, educated guesses about that.

Yen Carry Trade

A lot has been written about the size of the Yen Carry Trade and how much of it was unwound in the last two weeks. JPM claims that 75% of the trade has been unwound, an almost impossible figure.

No one knows the full extent of the unwind, but the truth is that it doesn’t matter, and the proof is right there for everyone to see.

All year, the big indices have traded in a close lockstep with USDJPY. Since August 5th, that correlation has disappeared. Until it returns, we don’t need to worry about further unwinding of the Yen Carry Trade.

VIX and Volatility

The VIX has had one of history's fastest unwindings of a spike.

The reason for that is because there’s been no contagion, not even a hint of one. Contagion has been something I’ve been watching closely. A good place to look for contagion is in credit spreads. I’m going to steal a chart from MktContext for that. (Side Note: His latest post is excellent and has a large free section; go check it out.)

Credit spreads did not spike at all during this crisis. With VIX falling rapidly and credit spreads unchanged, there’s very little reason to expect big blow-ups to come.

That said, I think the VIX may have fallen too far, too fast. I’ll touch on that more at the end of this article.

Goldilocks Economy

I mentioned earlier that I predicted we would “thread the needle” of economic data right into the Goldilocks zone last week. That happened as I predicted, so let’s take a look at what the data actually said.

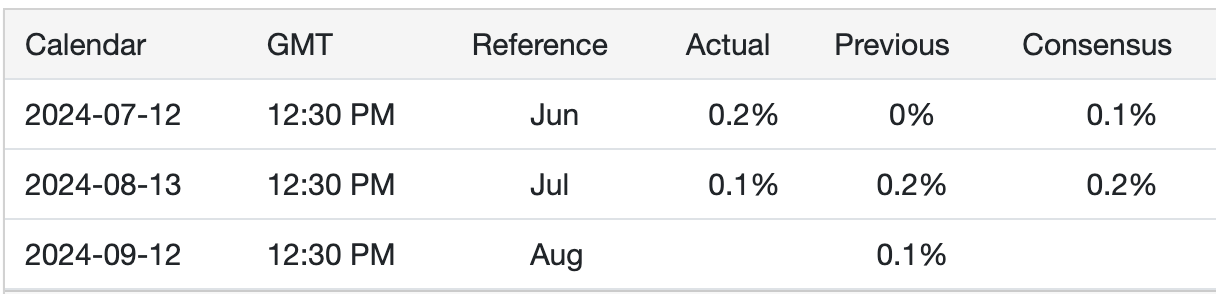

PPI came in quite cool, lower than expectations and lower than June’s numbers.

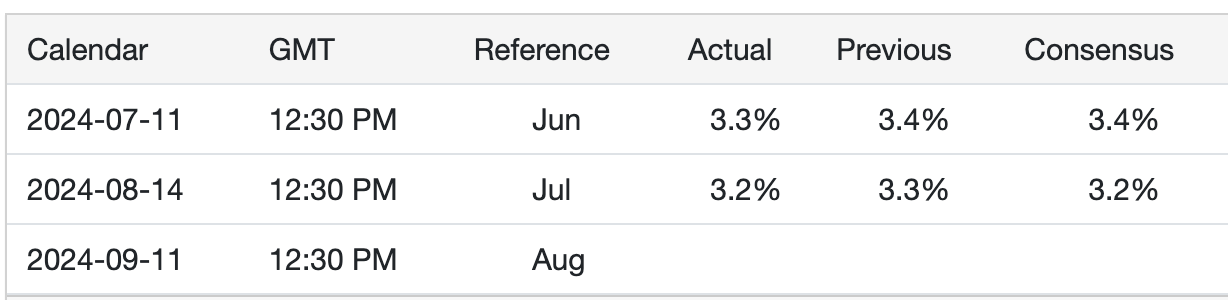

Core CPI came in ever so slightly below expectation and below June’s numbers.

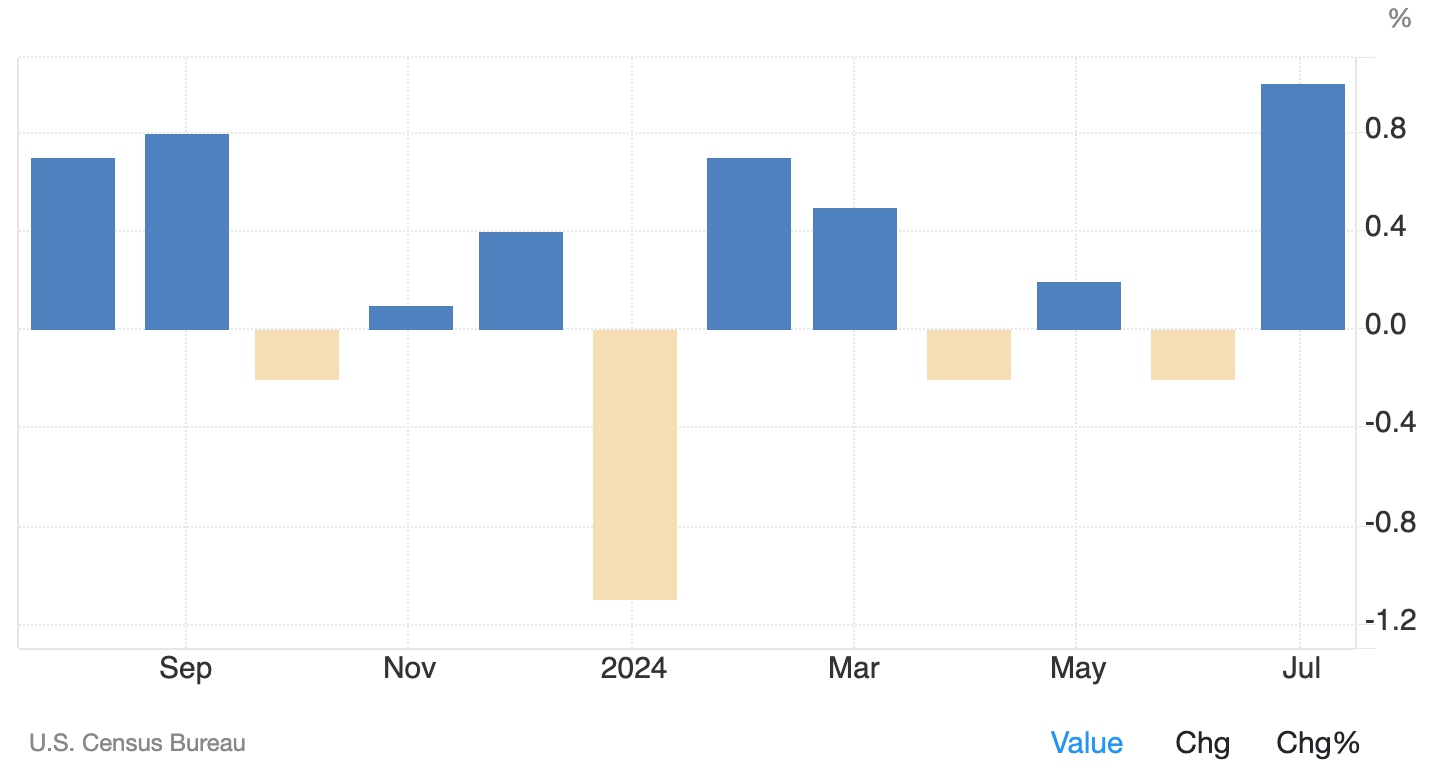

Retail sales came in quite strong, the best number in 12 months’ time.

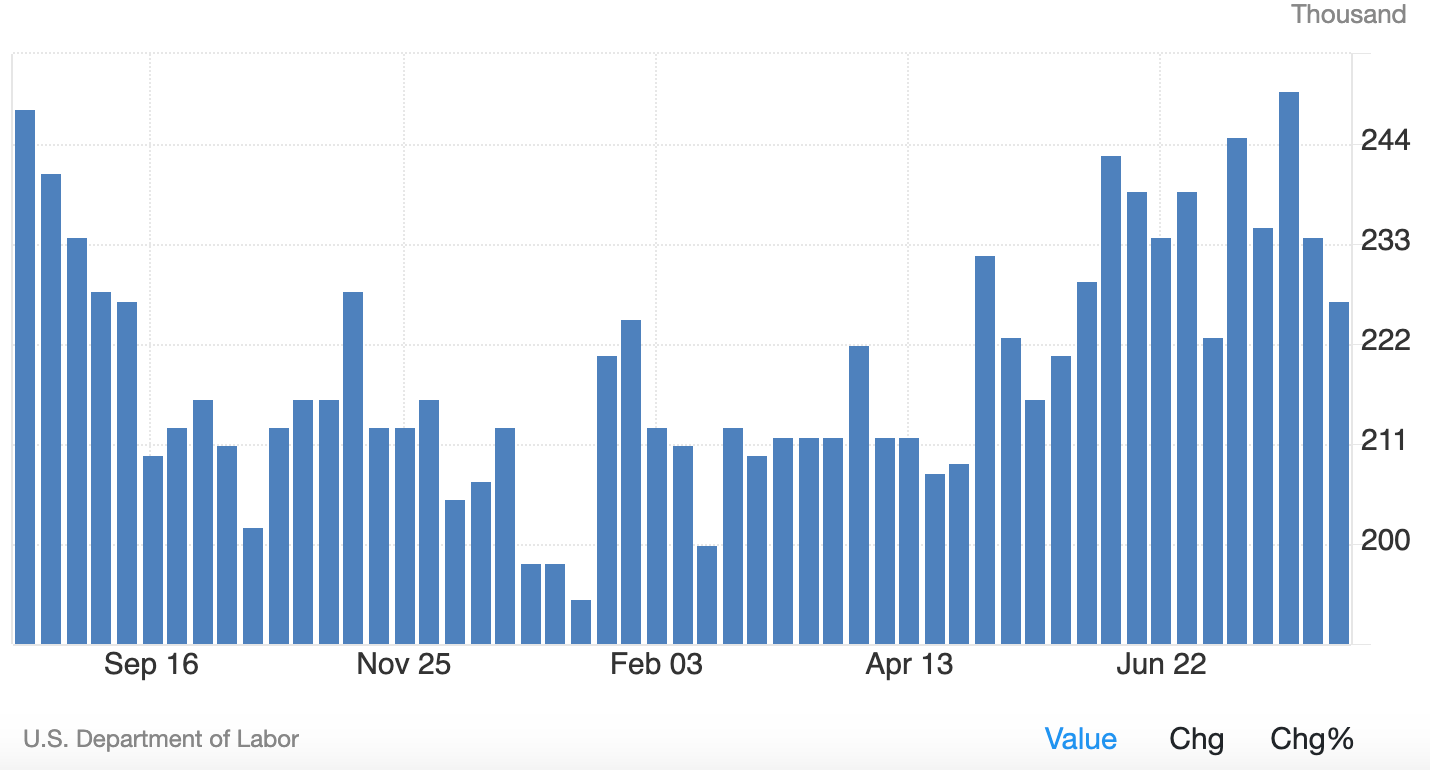

Jobless claims came in low, lower than expected, and also painted this pretty picture of a labor market that has slowed but isn’t slowing at an increasing rate.

Absolutely perfect data. Inflation is low, retail sales (a huge component of the economy and a bellwether for the consumer) are high, and there is a resilient job market.

Goldilocks if I ever saw it.

The Fed

Two weeks ago we had pundits calling for emergency rate cuts. Last week, the pundits and the markets called for a 50 bps September cut.

This week, Powell is speaking at Jackson Hole, and the market is pricing in a 75% chance of a 25 bps cut and a 25% chance of 50 bps.

I think the market is going to be disappointed. There is nothing out there to support a 50 bps cut. I would love to see it, as would the market, but I see no reason Powell would entertain that this week.

Therefore, I think Powell’s Jackson Hole approach will likely be hawkish. He will try to talk the market back from 50 bps.

Granted, the market may not care. Traders have been incredibly optimistic about rate cuts all year and have continually priced them out without too much turbulence.

The exception was in April when the March CPI data put together a 3-month hot streak, and we saw the S&P sell off about 5%.

Going Forward

“Hedge when you can, not when you have to.” I’ve brought that quote up a few times this year, and we have mostly done well by not hedging.

However, given how fast we have run up, how low the VIX has gotten, and how important Powell’s speech is this Friday, the market is pricing perfection this week.

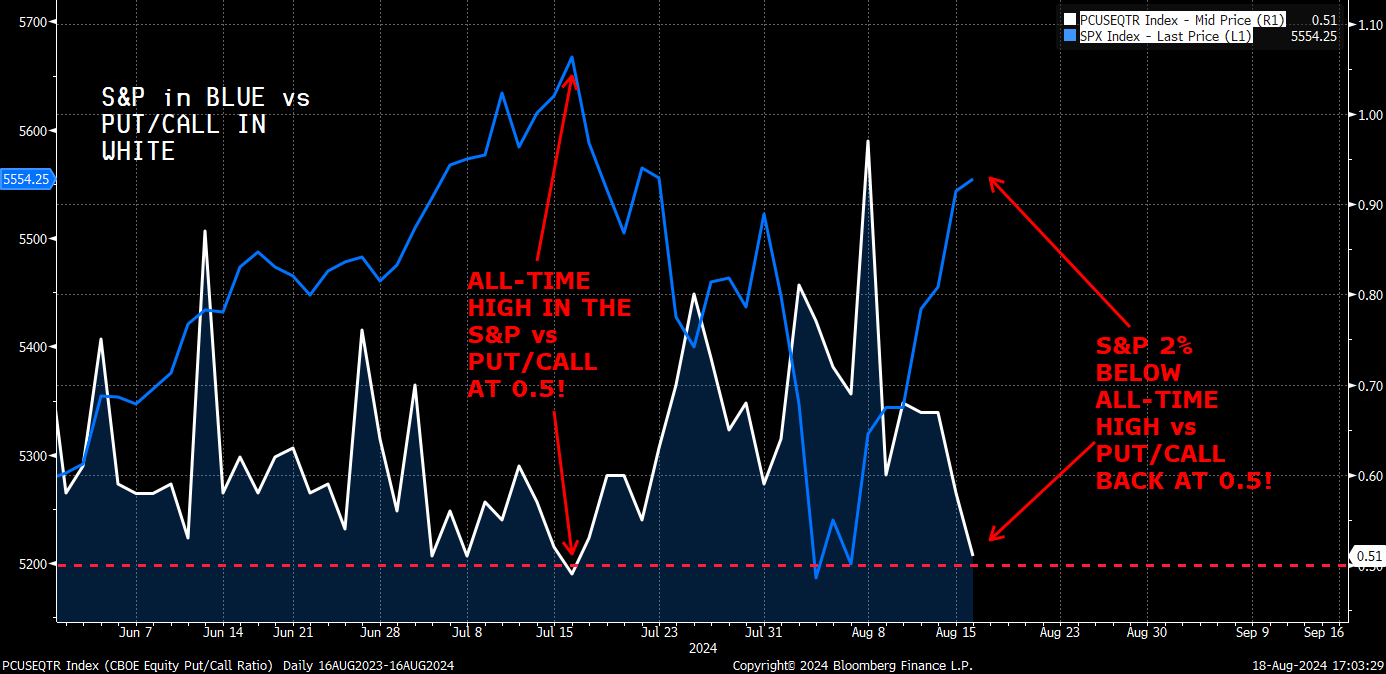

Let’s take a look at Put/Call spreads.

Thanks to Le Shrub for this chart.

We are back down to a ~.5 Put/Call ratio, the same as we hit at SPY all-time highs.

Taking everything in totality, I think puts are too cheap this week. The chalk outcome is certainly a low-volatility green week, but sometimes it pays to bet on the underdog.

I am still quite bullish, but I will look to buy some small put protection this week to cover Powell’s speech.

Join me in the chat to get my real-time moves on things like that.

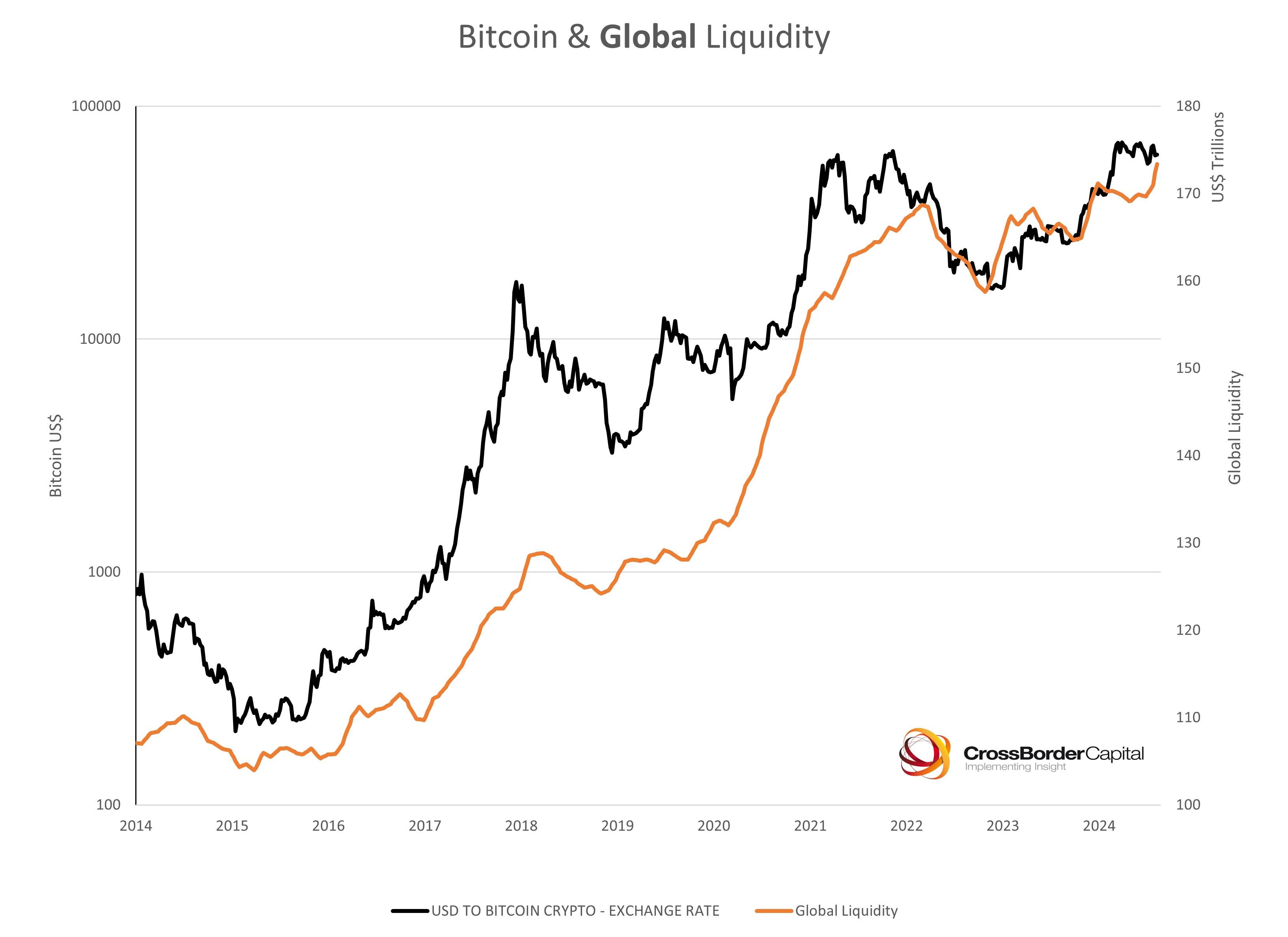

A Quick Note on Cryptocurrencies

While I am a “true believer” in the vision of cryptocurrencies (in some sense), as a trader, I view them as a high-beta bet on global liquidity. You can see why in the chart below.

In periods when liquidity is ticking up, Bitcoin tends to outperform. We look to be entering another one of those periods, which also comes on the heels of a big correction in crypto prices.

Also, anecdotally, my “true believer” friends have never been more disillusioned with crypto than they are right now—not since the lows in 2022, anyway.

All of this combines to make me structurally quite optimistic about a large upward move in crypto prices later this year. I can’t perfectly time the markets, especially not one as volatile as Bitcoin, but that’s my current outlook.

As always, stay careful out there and, more importantly, be lucky.

If you enjoyed this post, consider subscribing for free. Subscribers get all my market insights in real-time, directly to their inboxes.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here.