Don't Get Chopped Up

Going into Fed Meeting week with our heads held high...

Author’s Note: I plan to continue releasing free content where I can provide value to everyone. Posts will include premium content for paid subscribers at the end of emails or as separate write-ups.

I have written in the past about the proprietary trading signals I’m developing, those will always be paid content. These signals are truly proprietary in that I am aggregating and scoring data that isn’t quantified elsewhere.

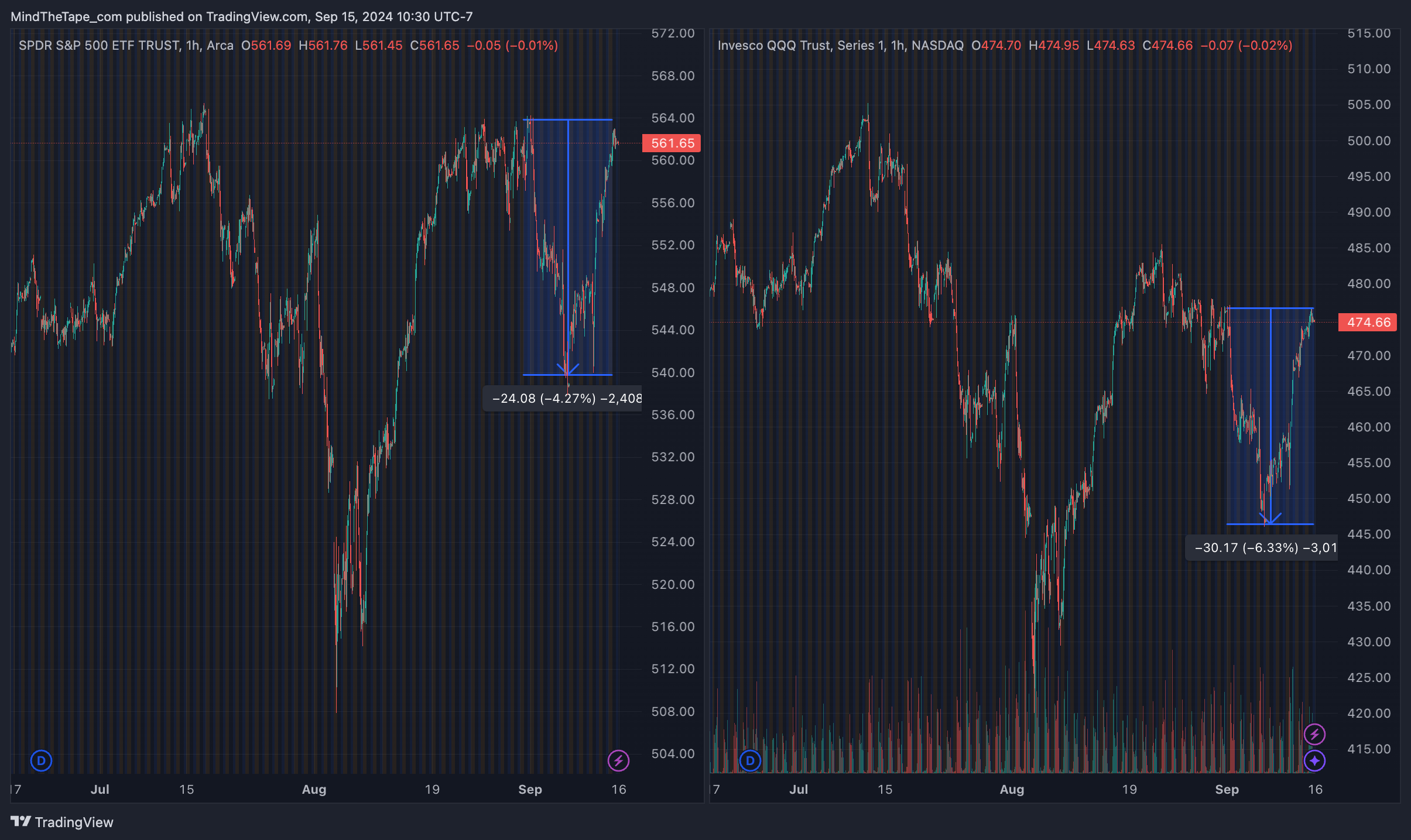

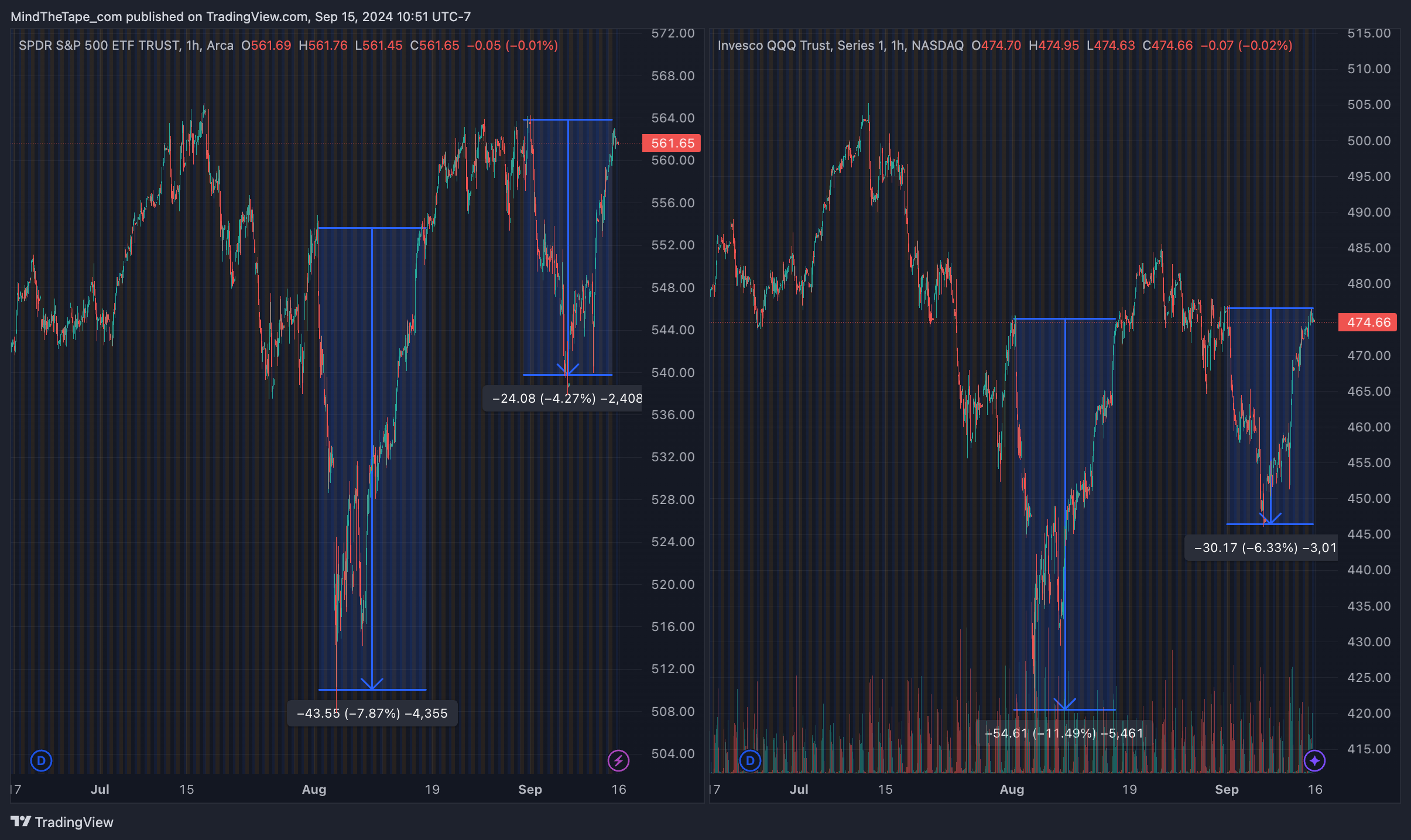

We’re coming off a very volatile start to September, with stocks rushing back last week to where they began the month.

A round trip of ~4.5% in the S&P500 and ~6.5% in the Nasdaq is nothing to sneeze at, especially when it takes place in two weeks.

Regular readers will know that we have traded these volatile markets well.

On September 3rd, as the sell-off began, we discussed the “it’s so over, we’re so back” chop we were in and urged people not to overreact.

Then, just before the rally began on September 8th, we flagged that those were not good levels to sell at, and we would be playing for a bounce.

We proceeded to get the big rally last week, having not let any of the chop shake us out of our positions.

Meanwhile, we also added some short-term long exposure last week, something that members of the chat got in real-time. Those short-term calls we fired returned ~6x and ~10x.

We give thanks, as Le Shrub says. Make sure you’re in the chat if you want those real-time call outs.

A Choppy Market is a Bloody Market

In these choppy markets where things are not trending in a clear direction, the most important thing to do is not to let them chop you up. Let’s look again at the price action of the last few months.

If you had fallen asleep at the end of July and woken up to check your brokerage account this weekend, you wouldn’t even know you’d missed anything. But when I see charts like that, I know they are littered with the proverbial bodies of the guys who sold on August 5th, rebought in late August, and then sold again in disgust last week.

Instead of a net-zero 30 days, they could be down 15% or more!

Flows Incoming?

I wanted to highlight a quote from MktContext that I found very interesting.

Given the strong bond outperformance relative to equities this month, pension funds and sovereign wealth funds will need to buy $125B of equities to rebalance portfolios. That’s a huge amount of price-insensitive flow. In addition, institutions moved >$100B into cash this past five weeks, which will eventually need to get redeployed into stocks.

He didn’t show his work, and I can’t vouch for the numbers, but the sentiment makes sense.

Vix Spikes and VAR Shocks

There is an odd dynamic in markets that we have discussed before but that I want to flag again.

When volatility goes up, the VIX spikes, which can trigger a VAR Shock. VAR stands for “value at risk,” and it measures how much a given position can lose over a period of time.

I’ve flagged some VIX spikes associated with the recent sell-offs. In these cases, selling begets more selling, as large institutions are forced to de-gross their position sizes.

You end up with a strange dynamic where these institutions are forced to sell on the way down and rebalance back into the assets if and when the VIX drops back to acceptable levels.

This dovetails into what MktContext said above. There is undoubtedly cash on the sidelines waiting to buy back in.

Powell’s Pivot

Beneath the hood, the economy is worse than people think. CPI last week was not good news.

Most of the data used to support the “no recession” thesis are lagging indicators, which means they have no predictive value.

In this newsletter, we’ve been very clear that the Fed needs to cut 50bps to slow the deterioration of the labor market before we reach a tipping point.

Well, late last week, the Fed started laying the groundwork for a 50bps cut with a whisper campaign in various publications like the Wall Street Journal and Financial Times.

SOFR Futures immediately repriced to 50/50 25/50bps.

We view this as a positive sign that the Fed is appropriately assessing the risks to the economy. Even if they only cut 25bps, which we consider a mistake, the jawboning about a potentially larger cut is promising.

Tomorrow will likely bring another round of articles hinting at the direction the Fed plans to move in.

Let’s see.

Parting Thoughts

We are in a difficult-to-read market regime. You might call it “It’s so over, we’re so back.”

Markets will likely continue to overreact to data points, causing periods of violent chop. That said, my gut is that we get a 50bps cut this week that the market reads as bullish.

If we do, and markets rally, we will have to remember that they are rallying against a backdrop of deteriorating data. That means we can’t let ourselves get greedy.

Continuing to buy well-timed hedges while staying materially long remains our best option. Like the Fed, we will stay data dependent.

I recently did paid deep dives into the CPI data last week and revealed my proprietary Fed Sentiment Indicator. If you want to take a look at those, make sure to upgrade. You can find them in the articles below.

As always, stay frosty, and good luck out there!

Reading Recessions With Proprietary Data

Mind The Tape is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Was There a Secret in Today's CPI?

To get insights and information when they are most valuable to you, subscribe below.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here. The information is presented for educational purposes only.