Groundhog Day

Haven't we seen this movie before?

Author’s Note: I plan to continue releasing free content where I can provide value to everyone. Posts will include premium content for paid subscribers at the end of emails or as separate write-ups.

The week ahead is a key one for economic and geopolitical events. We have escalation in the Middle East, ISM surveys and Nonfarm Payrolls all coming in hot.

Literally, if you’re in Beirut.

You're not alone if you feel like you’re in the movie Groundhog Day reading that introduction. Somehow, the first week of every month has been “unironically the most important week in macro” for about 4 months now.

“It's so over; we’re so back,” Meta continues.

Let’s dive in.

Assassination is in the Air

On Friday, we saw Israel assassinate Hezbollah’s leader Hassan Nasrallah. News of the strike started hitting the wires in the last few hours of the trading day, likely contributing to market jitters that saw the Q’s and SPX close near their lows.

So far, Iran has said little and seems reticent to escalate. This is in keeping with their response to previous escalations that have come from Israel.

The military calculus is simple for Iran: Outright war with Israel is a losing proposition. Especially after their previous and entirely unsuccessful strike on Israeli territory. Their oil production infrastructure is vulnerable, and there is no reason to believe Israel would not immediately destroy it in a direct conflict. At the same time, it’s entirely unclear whether Iran is capable of inflicting meaningful damage on Israel soil.

But the regional calculus is equally simple: Iran cannot allow themselves to be weakened into irrelevance while their proxies are taken apart piece by piece.

Obviously, there’s an uneasy tension between those two outlooks. It remains to be seen how Khamenei will reconcile the two in a way that best cements his political power at home and abroad.

I don’t see how Iran can meaningfully respond, and I suspect they are desperately looking for an off-ramp. Will Netanyahu allow a de-escalation that is likely against his own self-interest?

Chalk view: Nothing ever happens. We will see a few weeks of increased tensions, with sporadic Iran/Israel headlines spooking markets until they fade back into the background. Maybe oil will catch a bid, or maybe it will continue to be down only while the Saudis stroke their beards and execute their inscrutable plans within plans.

We are in a challenging situation as traders where both the US and Iran have been “the boy who cried wolf” one too many times, warning of Iran’s imminent intent to escalate. It will be hard to know what headlines to credit, but I’ll be keeping an eye out and will inform you if I see something that concerns me.

Make sure you’re in the chat to get that in real-time.

The Most Important Week In Macroeconomics

Monday will open with the Chicago PMI, which is not that important in and of itself but is likely to be read by markets as a barometer for the major ISM releases on Tuesday and Thursday. We also have Powell's speech on Monday, where he is likely to add some color to their recent decision to cut 50bps.

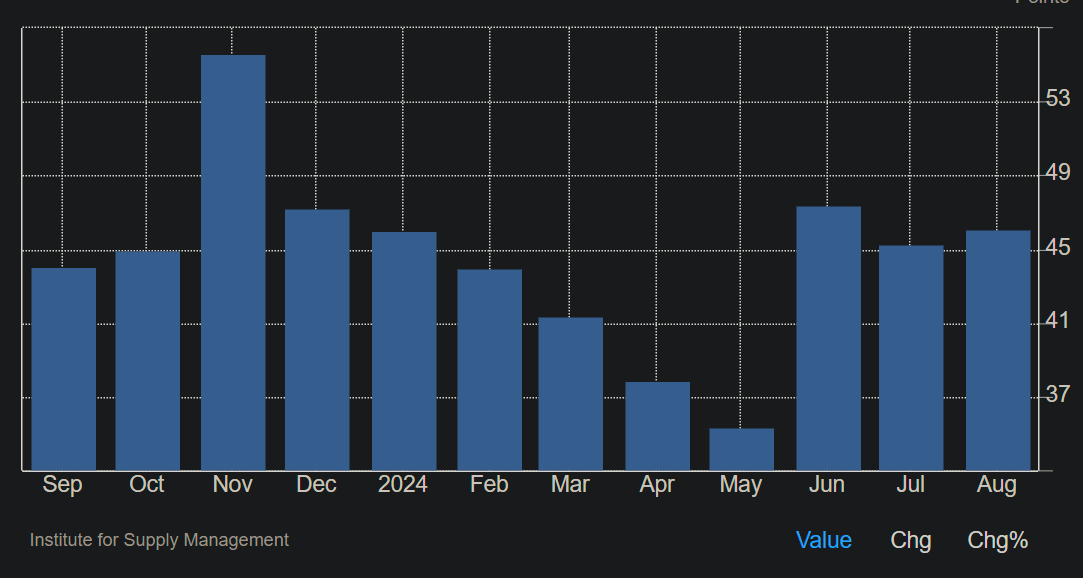

Tuesday we get the S&P Manufacturing PMI, followed by ISM Manufacturing. ISM Manufacturing is the main event here and has been in the dumps for at least 18 months but is expected to rise from its low in July (47.2) to 47.6.

Missing the estimate to the downside is bad, and to the upside, is good. Anything between 47.2 and 47.6 should be roughly considered “fine” as it continues to show directional improvement. Anything below 47.2 will be a serious “it’s so over” moment.

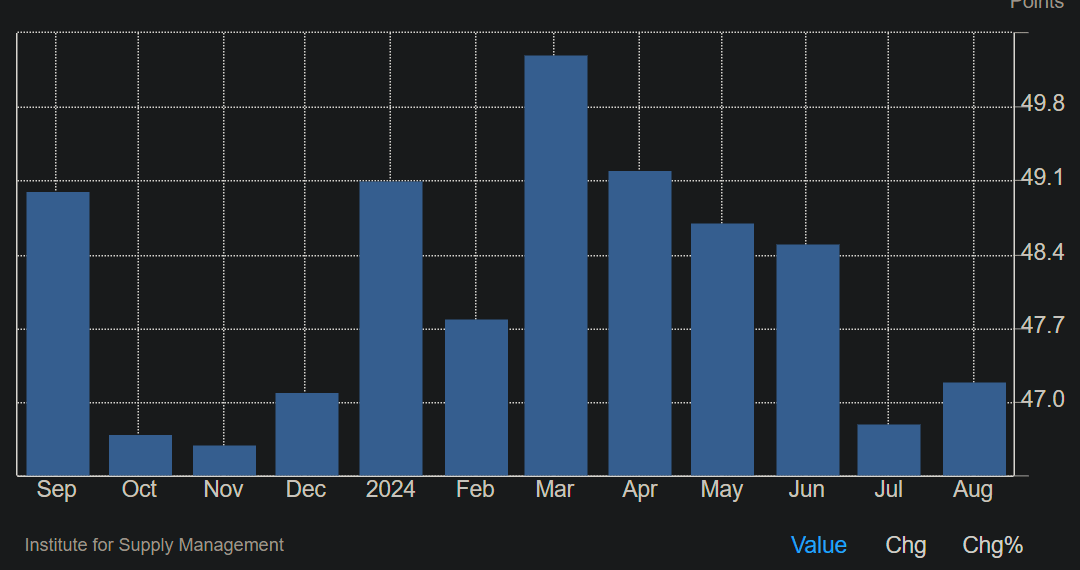

Thursday, we get S&P services as an appetizer to ISM Services, the true main event of the survey indexes. It’s expected at 51.6, a very slight improvement over August’s 51.5. ISM Services has held up much better than the manufacturing data, and the market will view any deterioration in it as a horrible sign.

ISM Services has an employment component that will be closely hawked as well.

Friday is the jobs data release, unironically the Most Important Number Ever™, with all eyes on Nonfarm Payrolls and the Unemployment Rate. Nonfarm Payrolls are expected to have grown by 146k, up from 142k in August. The unemployment rate is expected to have held steady at 4.2%.

Deteriorating data in either part of the jobs release will be horrific for risk assets.

Quick Election Check-In

Trump has fallen behind in the race post-debate, and I can’t help but wonder if that is part of what has been weighing down markets.

I wrote before about how Trump is clearly better for markets and the economy than Harris. Check it out, and if you still disagree, feel free to let me know in the comments.

Polymarket has the race pegged at almost 50/50, with Kamala leading slightly. Most other places have Kamala leading much more decisively, but Polymarket is the most liquid, so that’s what I use.

The View From Here

This week’s data is awkward for traders and investors. The Fed’s 50bps cut hasn’t had enough time to work its way through the system, but so far, the data looks to have bottomed somewhere around May - June.

This week of data releases will likely set the tone for risk assets until November when another round of data and the election results arrive.

Heading into Monday I am cautiously optimistic. We picked up some October 31st, SPY 560 puts for downside protection, and I closed out some of my leveraged longs from the week.

These are prudent risk management moves. As the saying goes: hedge when you can, not when you have to.

But my personal view is quite bullish. I will be looking for nuggets of Goldilocks data this week to signal risk-on and looking to bet on a rally.

The Fed easing into a Goldilocks scenario while China stimulates is one of the most bullish situations I can imagine for equities.

Still, let’s stay unbiased and let the data and market guide our positioning.

Stay frosty, and good luck out there.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here. The information is presented for educational reasons only.