Has the Recession Already Started?

Steel-manning the case for a recession being upon us

Steel-manning is the practice of presenting an argument in its strongest and most compelling terms to argue against it. It’s the opposite of the process of “straw-manning,” where you mischaracterize an opposing argument to make it easy to tear down.

I don’t see a recession in the data. But for this article, I’ll do my best to find it.

Forecasting a Recession

Forecasting a recession is difficult. There are always conflicting data points and pundits who want to tell everyone the party will continue to push those positive data points.

Meanwhile, the people who call for recessions early are typically those who incorrectly call them for years before they arise. That’s where the old joke about someone “correctly calling 9 of the last 5 recessions” comes from.

But lowdowns are self-reinforcing. I think it’s time to start steel-manning the case for a recession so we are prepared.

Research from UCSC

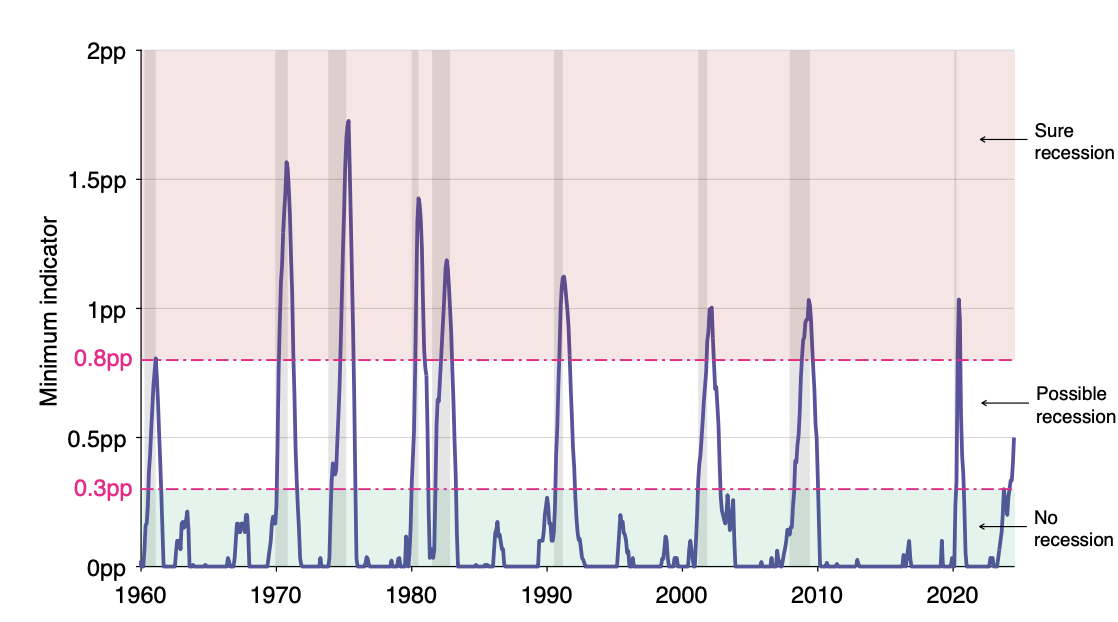

A paper released this month by a researcher at UC Santa Cruz proposes an alternative to the Sahm rule for predicting recessions. This proposed indicator suggests a 40% chance we are already in a recession and implies that the recession may have started in March 2024.

The paper is relatively unsophisticated, and the 40% number is completely bogus. However, their proposed indicator has an even longer perfect record of predicting recessions than the Sahm rule.

Why is that 40% number completely bogus? They identified that “.3pp” on their indicator represents the lower bound for a possible recession and that “.8pp” and above represents a 100% chance of recession. The indicator is at .5pp, so they said .5pp is 40% of the way to .8pp, which means a 40% chance of recession.

That’s bogus math, but figuring out the proper chance we are in a recession from this indicator is complicated because there has never been a period where the indicator hit .3pp, and a recession didn’t trigger.

This is a pretty discouraging chart. Don’t read too much into it, though. The authors drew the red line at .8pp specifically because that was the lowest number they could find that captured every recession.

Still… I don’t see any instances of the number cracking .3pp and falling back to the “no recession” zone either.

The Daily Feather

Danielle DiMartino Booth writes a publication on Substack called The Daily Feather. She has been loudly saying we are in a recession for months now. I have followed Danielle for the last few years, and she brings a data-heavy approach to market analysis that I respect. Still, if you had listened to her claims that we are in a recession, you would have missed out on significant gains in equities.

I decided to poke through her newsletter, looking for the most compelling charts that scream recession.

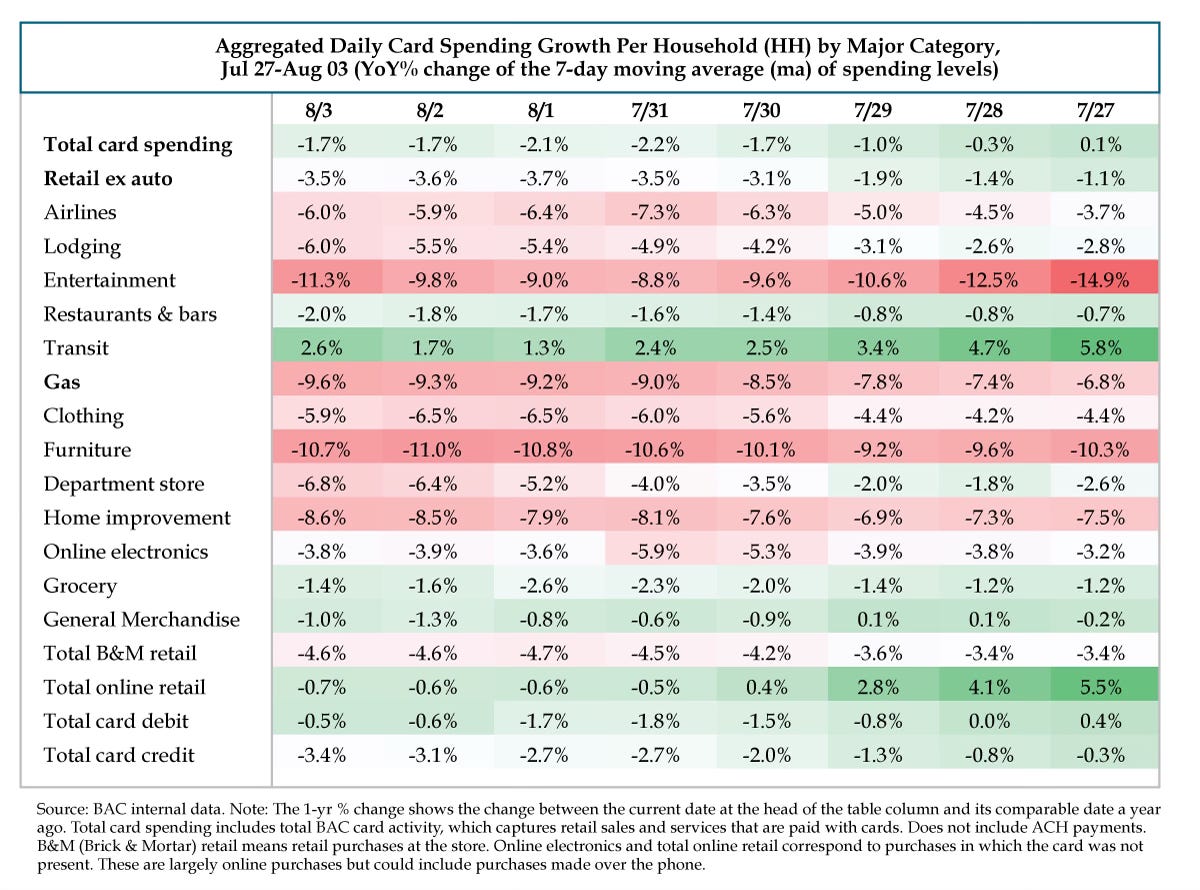

This one shows card spending by day, compared to the same period last year. In theory, it shows us two things.

It shows that total card spending worsened seasonally, just from 7/27 to 8/03.

It also shows that card spending is significantly lower at the same time this year compared to last year.

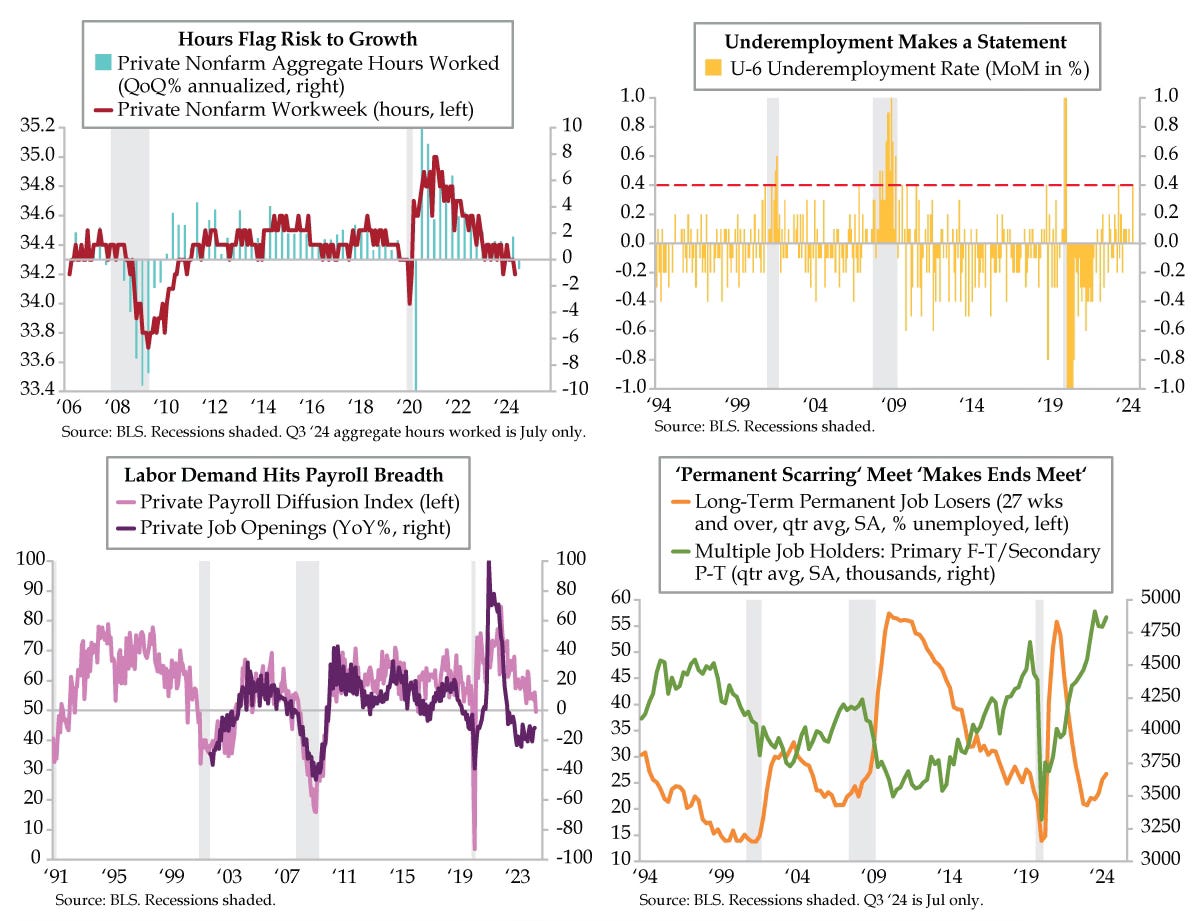

Here’s a 4-pack of charts for us to digest.

Going clockwise from the top left and finishing with the bottom left:

Nonfarm payrolls may not be sending up too much of a warning sign, but workweeks are being shortened. Employers often take this step before they begin letting people go—cutting shifts.

This one is indecisive. We got one big tick up, but more important to a recession is how heavily the spikes cluster.

This one relates to chart one, in which we saw that people are having their hours cut. That’s led to an increase in the number of people taking second jobs. Here we also see permanent job losers tick up, which doesn’t often happen outside of recessions and can accelerate rapidly.

I’ll leave readers to interpret this one, as I’m not entirely clear on what the “private payroll diffusion index” refers to.

Again, in all these charts, the last few months of data have begun to look troubling. We are clearly entering a slowdown at best and a recession at worst.

The Unicorn and The Black Swan

At this point in the search, we can see that things are slowing down—more so than is typically associated with a slowdown.

They are also slowing down less than is typically associated with a recession.

The problem with that analysis is that when we are entering a recession, these negative indicators tend to worsen quite quickly.

So, whether we are heading into a recession or not, it’s more important than ever to stay careful and nimble. If we are simply slowing down and will emerge on the other side into another bull run, then we should have some chop between now and then and plenty of time to reallocate.

As I’ve written, I expect the market to twist and turn on every piece of economic data for a while. If we can string together some good news, it might be time to get back in the water.

If we can’t, it will be time to get out of your pool membership.

Stay careful, and I’ll be here to help make sense of the data as it comes in this week.

Good luck out there.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here.