Hurtling Towards... Something

Can These Indicators Predict a Recession?

Quick Note: I recently enabled paid subscriptions. I have not yet ultimately decided how to break down free vs. paid content. My main goal is to grow a community here where we can learn and discuss together. The plan is always to have primarily free content where I can provide value to everyone. Eventually, I will experiment with adding paid sections to the end of posts, etc.

If you want to support me with a paid subscription, I would appreciate it and will make sure I provide value. If you don’t or can’t, just know that I still appreciate you and will make sure you’re getting the valuable insights you signed up for too.

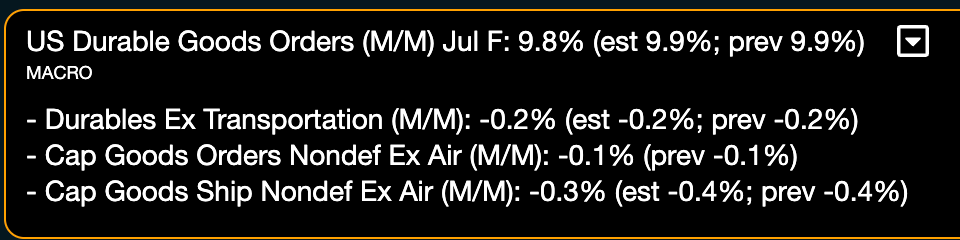

The theme of the week has been “new economic data.” Yesterday we got ISM Manufacturing. Today, we got JOLTs and Durable Goods orders.

You can see the trends in that data. The economy is slowing, something that has been obvious for a long time. There is no way to curb inflation without slowing the economy.

As I keep saying, the only question is, “How bad will the slowing get?”

Will we get a recession?

To answer that question I decided to dig into the weeds on some of this data, check out the historical analogues, and try to determine what data is still relevant in the changed landscape of 2024.

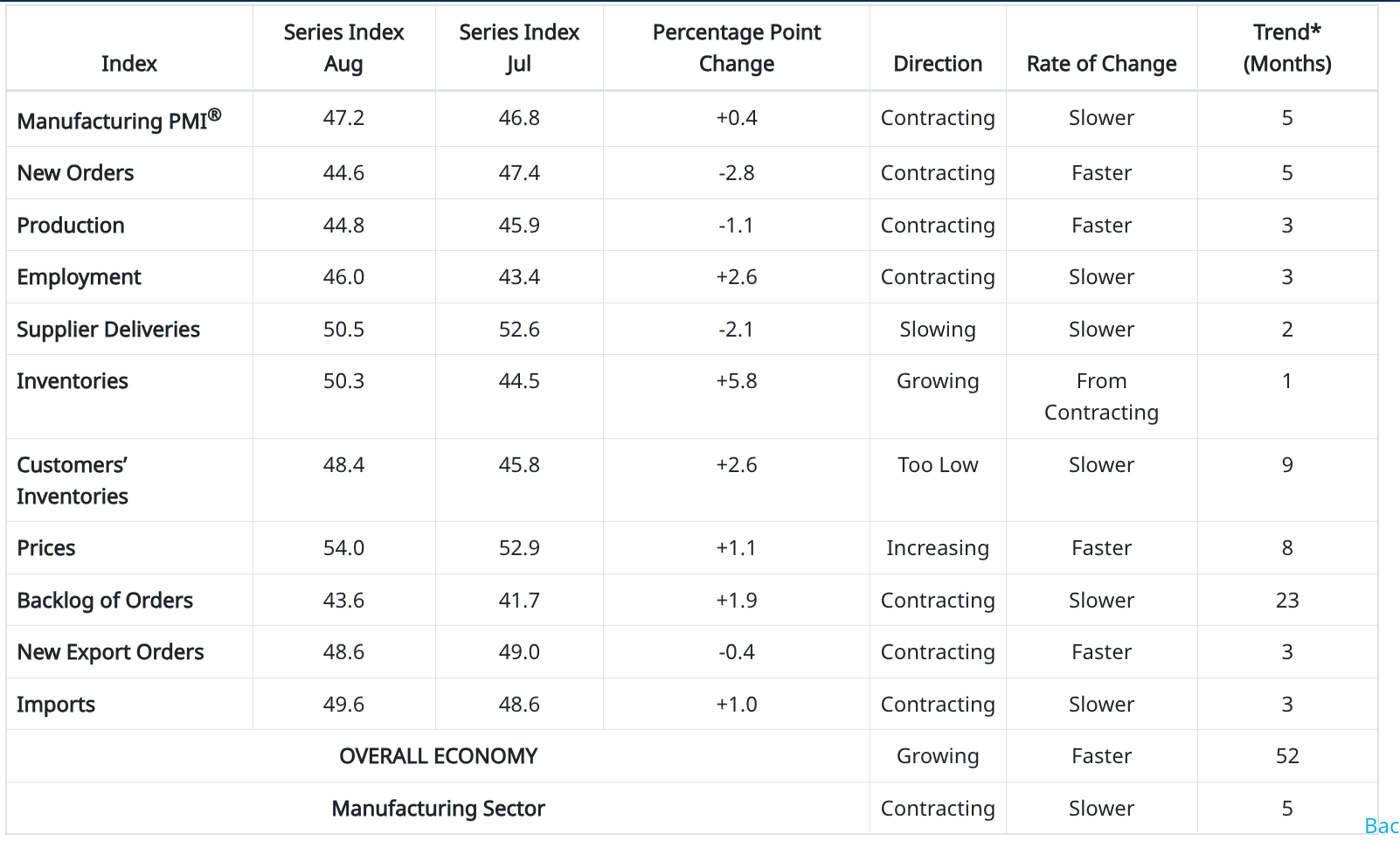

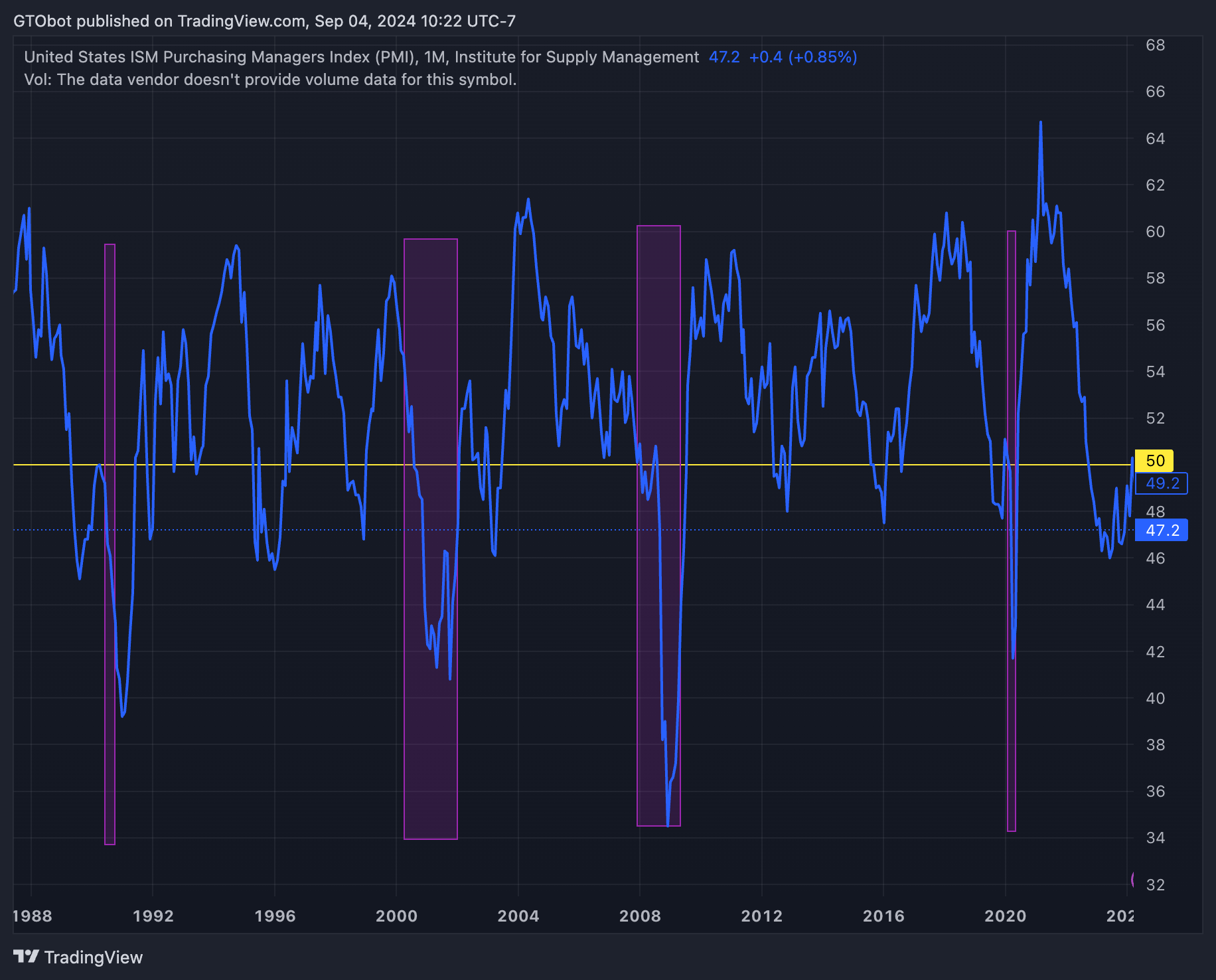

ISM Surveys

The ISM (Institute for Supply Management) surveys are monthly reports that aim to gauge the economic health of the manufacturing and services sectors in the United States. They are widely followed because they, in theory, provide real-time insight into the health of various sectors of the economy.

A reading over 50 is generally considered expansionary, and a reading below 50 is considered contractionary.

That’s great, and it can tell us when we are in a recession, but how useful is it as a leading indicator?

There are a few immediate problems. One, it generates a lot of false positives that make it tough to read. In 1989, 1995, 2003, 2012, and 2015, you’d have been pretty justified in worrying about a recession. But one never manifested.

And if you try to look at absolute change post-covid, you’d have been forecasting a recession for… 3 years.

The ISM surveys, especially those for manufacturing, are utterly distorted by Covid. And furthermore, manufacturing only represents about 10% of GDP these days.

ISM Services

Maybe the situation is better for non-manufacturing surveys?

Actually, yes, it is. Non-manufacturing ISM does a much better job of pegging recessions. There has only been one false positive. ISM Services has very high specificity and sensitivity, to use terms from disease testing. That means it’s powerful for identifying recessions and the lack of recession.

The problem is, it’s not a leading indicator.

Zooming in on each of the recessions in this chart, let’s look at when ISM Services deteriorates.

The data did not deteriorate much before QQQ (purple line) gave up the highs, and the ISM numbers did not appear to decline before a recession started.

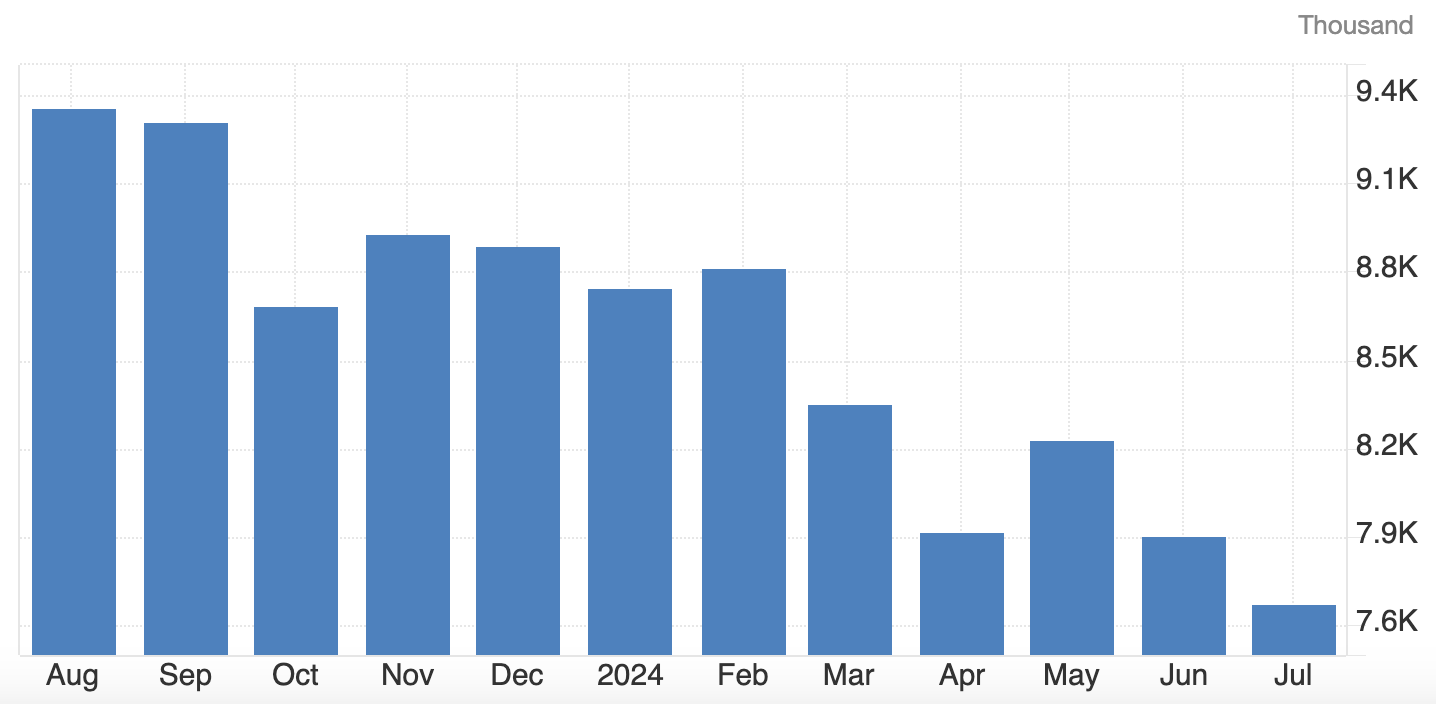

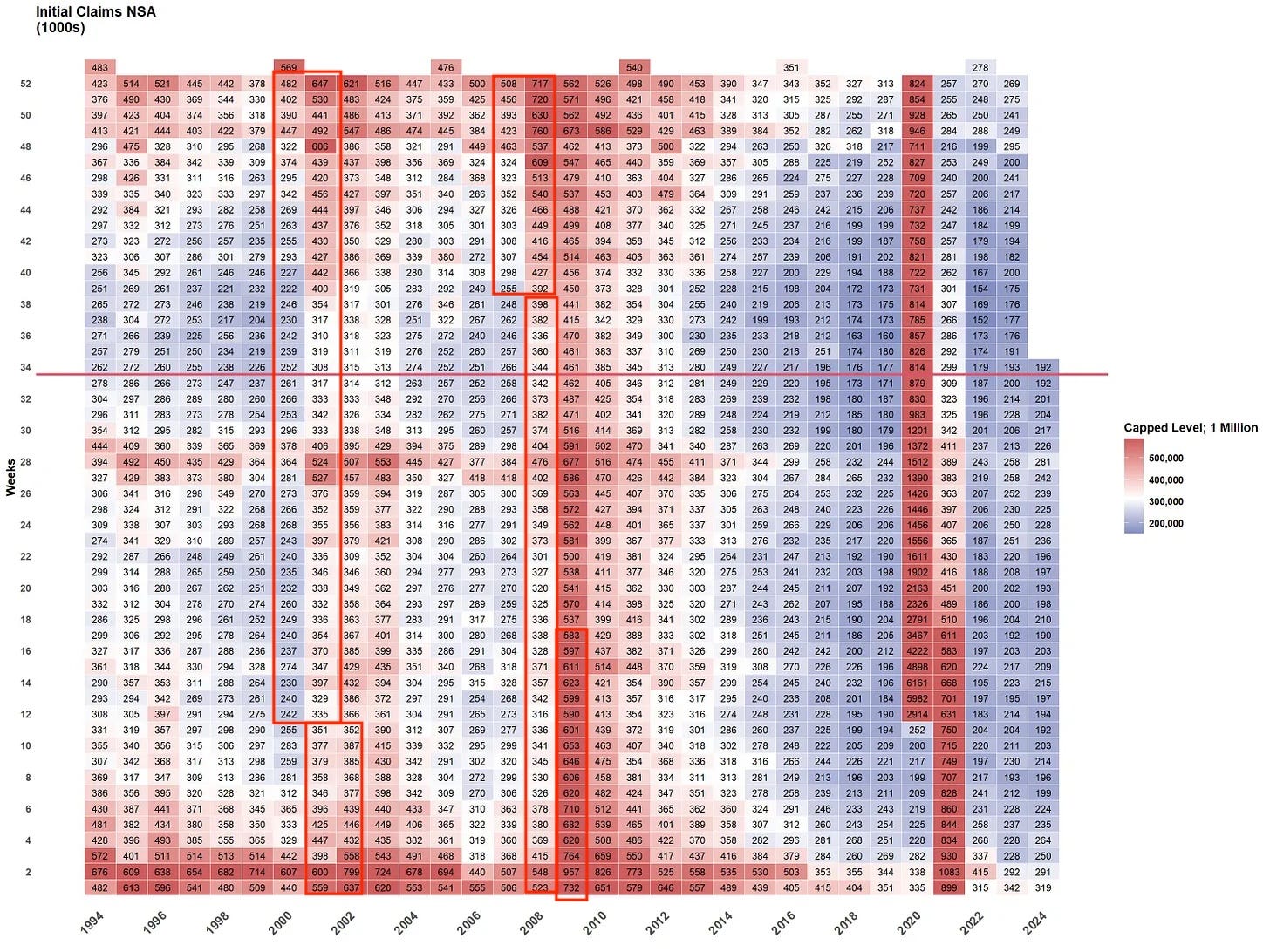

Labor Data

I’ve shared this chat from George Robertson a number of times here. It shows the Initial Jobless Claims by week. Let’s take a deeper look at it.

I’ve added some red boxes around the recessions in 2000/1 and 2007/8.

The periods immediately preceding these were indistinguishable from any other.

I think the overall message that we have a historically strong job market is still meaningful. But we clearly can’t rely on initial jobless claims to predictively warn us of a recession.

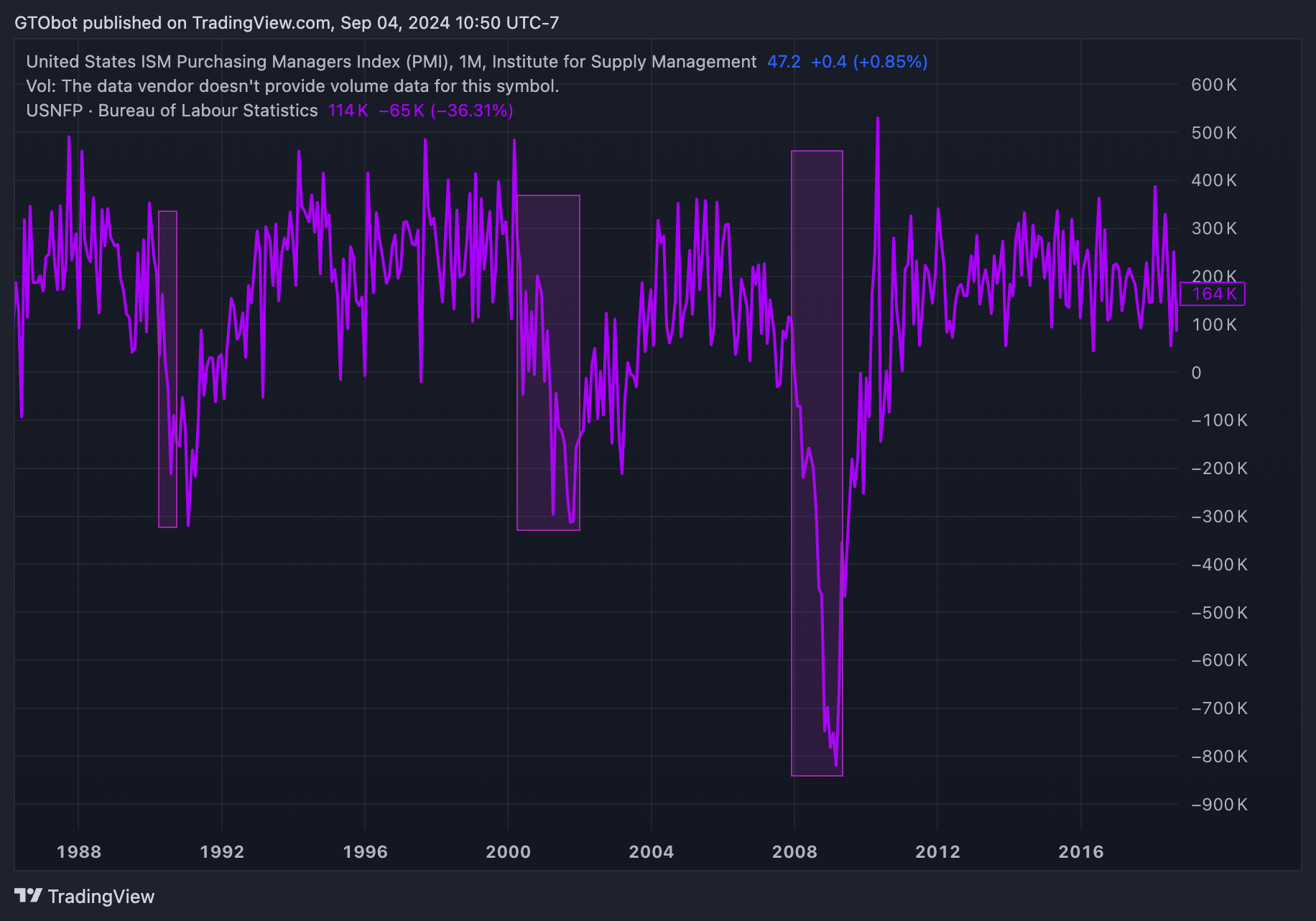

Non-farm Payrolls

I’ve cut out the Covid-recession from this chart because it distorts the axis and, obviously, wasn’t going to be predicted by the labor market.

This is the best one yet, but it’s still not perfect. Outside of the occasional random tick and the periods in or after a recession, Non-farm payrolls never go negative without a recession.

Predictively, it’s still a little tough.

Like most of these indicators, things tend to look ok until, suddenly, they don’t.

Taking the post-Covid boom years out of the equation, payrolls look pretty normal. They are expected to come in at 163k for August, putting us at the pre-covid average.

Fundamentally, though, the market is seeking reassurance from this print. The absolute number isn’t important, what’s important is the number relative to expectations.

The truth is, there’s no predicting a recession. Any given one of these indicators deteriorating or improving moves the odds around a bit, but not much.

Hence, the dominant regime remains, “It’s so over, we’re so back.” In other words, uncertainty.

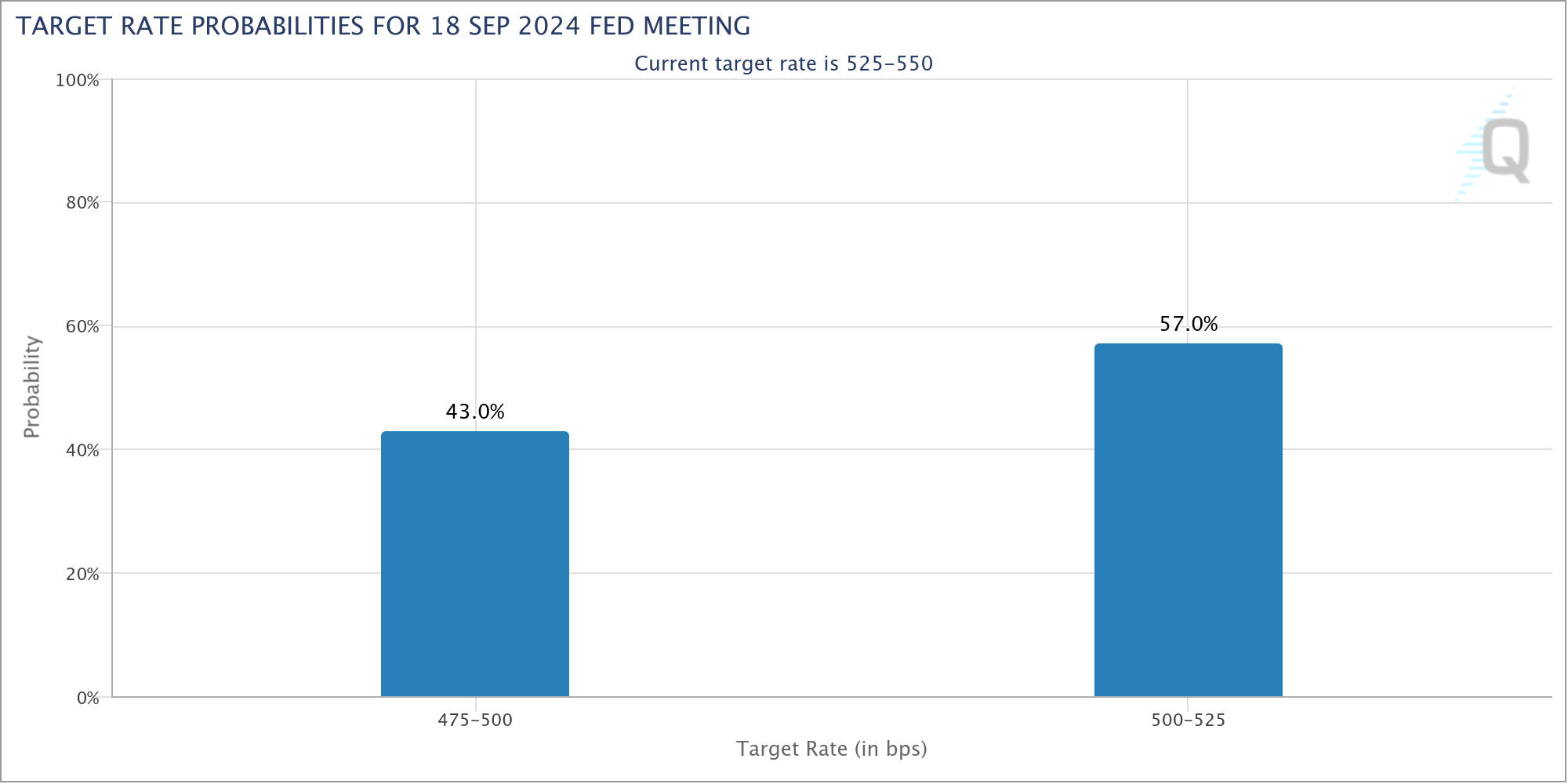

CME Fed Watch

We dramatically increased the odds of a 50bps hike today with weak JOLTs data. I am coming around to the idea that the Fed may hike 50bps.

With every weak data print, their Friday payroll data threshold lowers for being considered “weak enough” to cut 50bps.

Parting Thoughts

If you’re a tactical trader, this is your dream setup. For the rest of us, we have to do our best to stay nimble.

If we learned anything from yesterday, there is a mountain of selling waiting for bad data.

Nevertheless, it pays “to be fearful when others are greedy and to be greedy when others are fearful.”

We missed our chance to be fearful about two weeks ago. I don’t want to miss our chance to be greedy.

As always, be careful out there, and good luck.

And even more importantly, subscribe for more!

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here.

Glad to see more sharing of George's data, he certainly is an undervalued source of alpha!