It's So Over, We're So Back

The tale of two economies...

It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair…

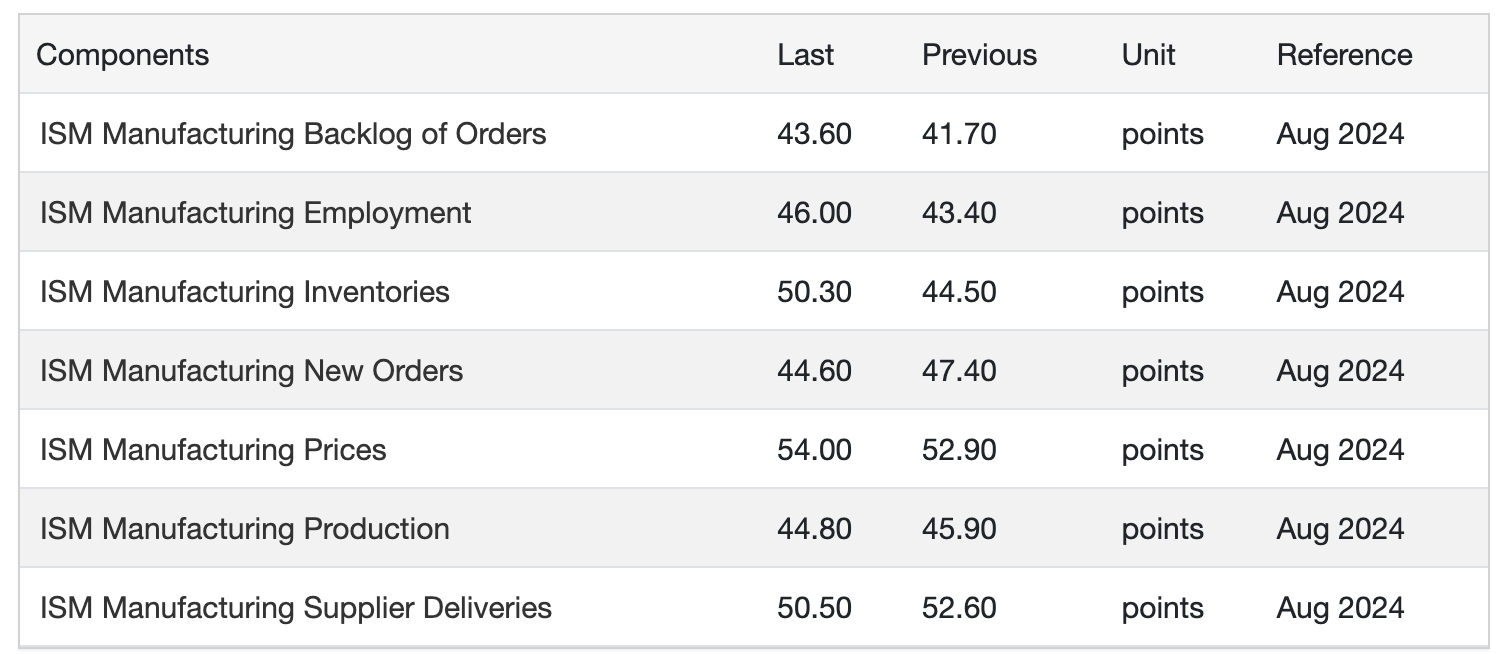

We got manufacturing data today, and it was ugly, ugly, ugly.

This marks two ugly months in manufacturing in a row. You might remember that the July ISM Manufacturing survey spark a similar large sell-off the Thursday before August 5th.

Well, it looks like we are in for something similar this month.

I’m a bit surprised to see this magnitude of a sell-off on the data. You’ll note that some of the key numbers in here are better than the July numbers, notably Employment.

Prices up and new orders down is the stuff of stagflation, the market’s worst nightmare.

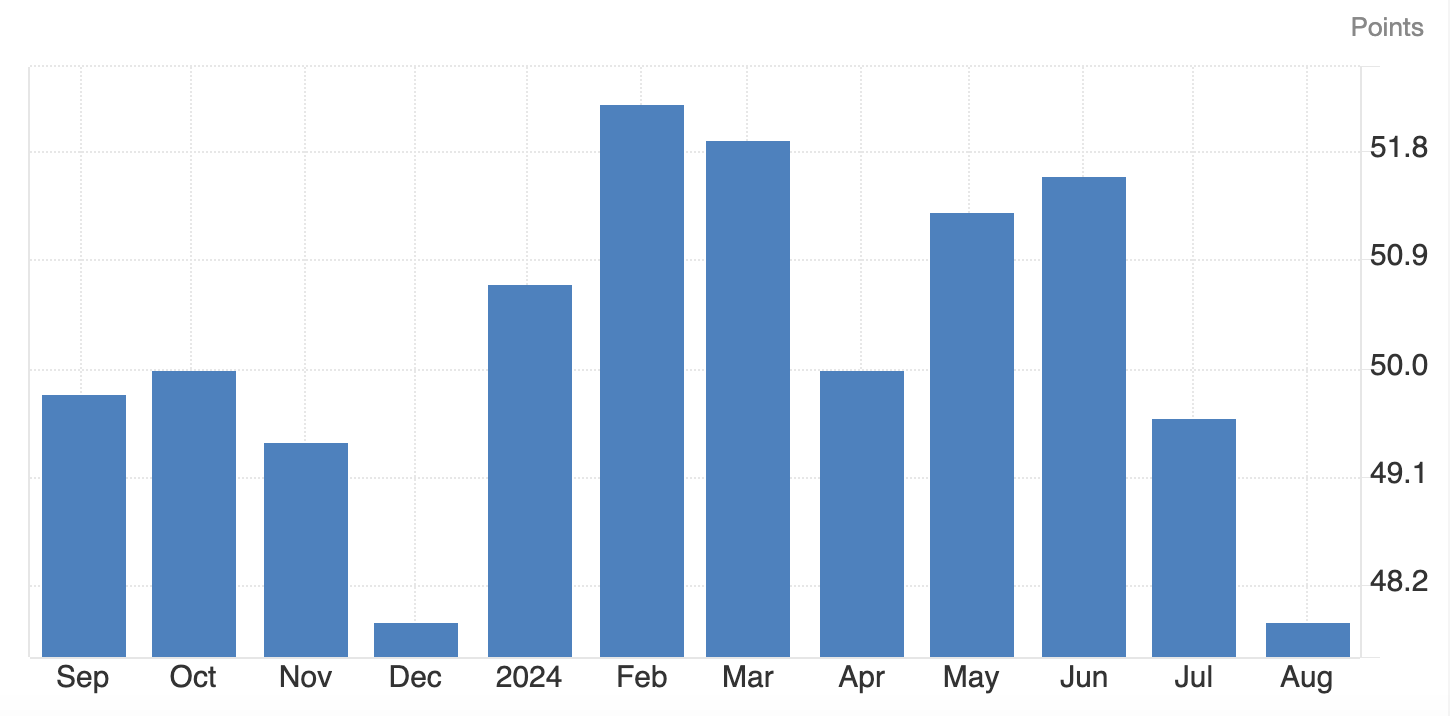

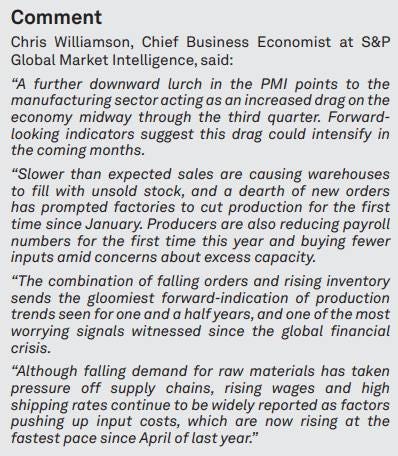

The S&P Global US Manufacturing PMI came in very cold. I’ve never paid much attention to that metric, but this month, it seems to be significant.

Worse even than the number itself was the commentary from S&P Global Market Intelligence that accompanied it.

ISM Services

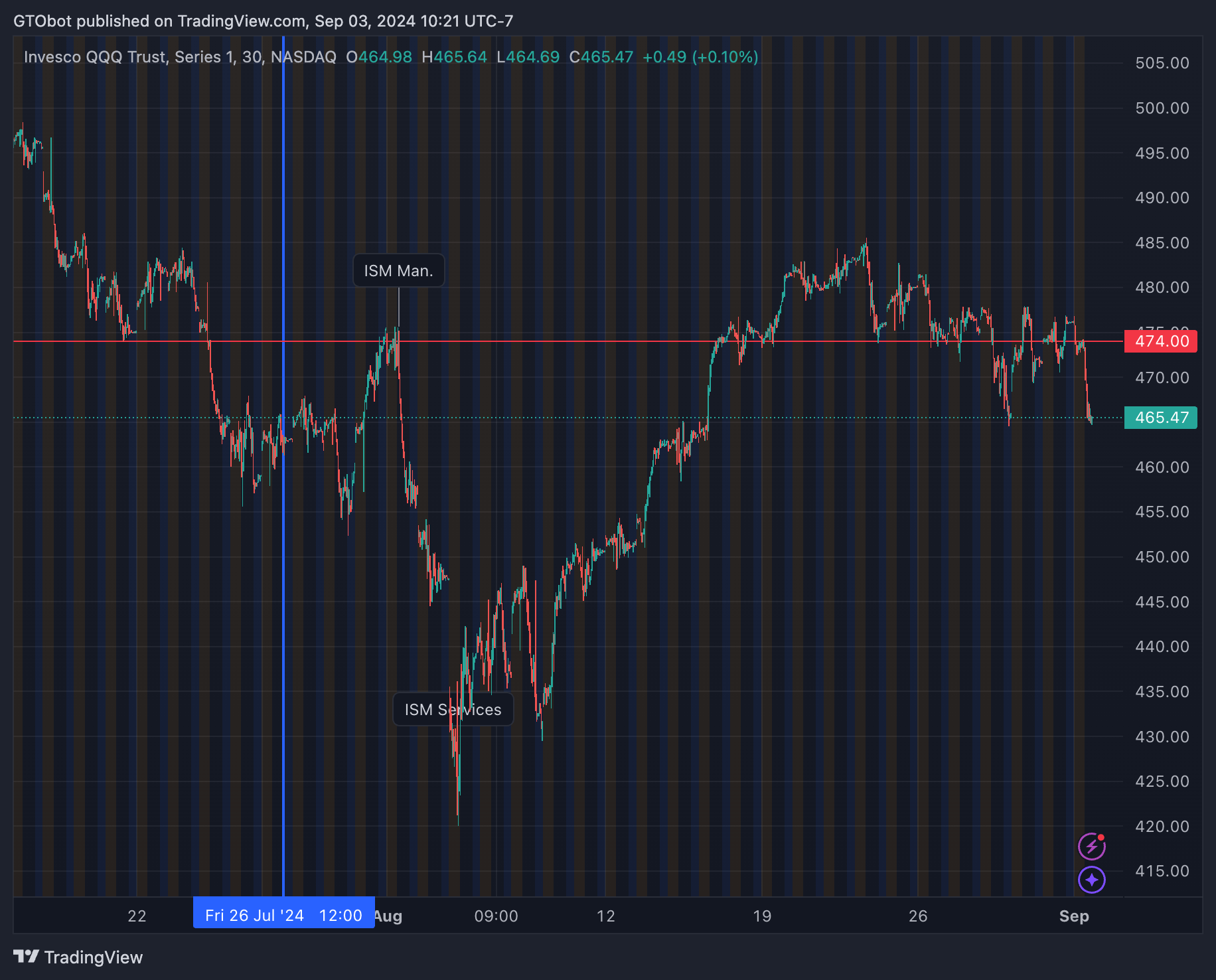

Last month, ISM services came in a few days after ISM manufacturing and saved the day.

Combined with the unwind in the carry trade getting “resolved,” they sparked an 11%+ rally in NQ.

This month ISM Services is scheduled for Thursday morning. Will we get the same bounce?

Only 44 hours to go…

We’re So Back, It’s So Over

There’s no way of knowing how services will come in. But I think the strong trend emerging here is a “We’re so back, it’s so over” economy where it’s impossible to draw conclusions about the economy as a whole.

Just last Friday, Personal Income came in hotter than expected, Chicago PMI was stronger than expected and trending upward, and on Thursday, GDP was revised upward to 3%.

Take a look at these charts comparing Dollar General stock to Walmart.

They serve very similar consumers, but they’re having a completely different experience of the economy right now.

We’re So Back? It’s So Over?

A New Type of Recession

Lyn Alden’s most recent premium report covered this “dual economy” situation.

One of the themes I’ve had for a while is that recessions look different in economies experiencing fiscal dominance compared to what we’re normally used to. This is similar to how recessions tend to show up differently in emerging markets than in developed markets. Developed market recessions tend to be more about bad credit cycles and high unemployment rates, while emerging market recessions tend to be more about stagnation and currency crises.

The excellent PauloMacro has discussed the same phenomenon, turning it into a refrain:

Inflationary recessions create monetary illusions.

The truth is we are in uncharted territory in the United States. The middle and lower class aren’t in a great spot. Their buying power has been quietly eroded, and their ability to make important purchases like a home has never been lower.

Meanwhile, there is a lot of extra money around, and if you are lucky enough to own assets, you will likely be in the most robust financial state of your life.

Surprises Ahead

Currency debasement is the only certainty in a period of fiscal dominance. Over a long enough timeline, we should expect continued asset inflation coupled with increasing inequality.

Over the next few months, the market will have trouble digesting new economic news as it tells a conflicting story.

That’s because we truly are seeing a bifurcation of the economy, one in which asset owners will benefit, and asset renters will suffer.

Equities may not be the immediate winners amidst this economic uncertainty, but I remain structurally bullish.

Hopefully, you all took it to heart when I said I don’t see any “fat pitches” now and de-risked some. I wish I’d taken my advice to heart a bit more!

As always, stay frosty and get lucky.

And don’t forget to subscribe!

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here.

I also took some chips of the table end / mid August. Global liquidity doesnt look good for september, and the it's over / we are back conflicting information will certainly continue this month. As the market priced in too many cuts, I think september could be as worse as some people thought. October might be decent to start front running a Trump victory with some BTC buys imo