May Flowers...

Might be late to arrive

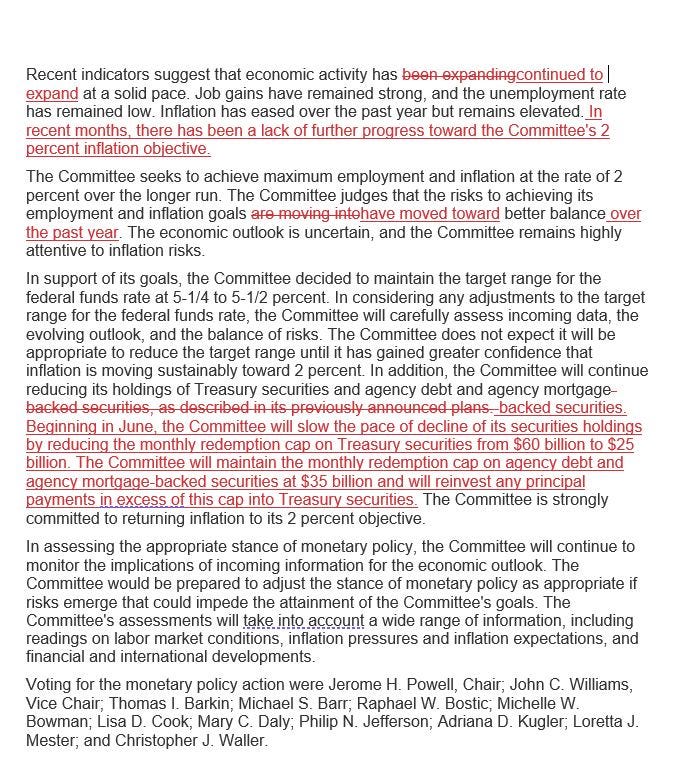

Fed interest rate decision came out today, and it was exactly what was expected. Some key language in the press release was changed to indicate that the Fed is seeing less immediate progress on inflation that they have in recent months.

The Fed is also beginning to wind down QT, earlier than expected.

Powell continued on to give the usual 1 hour Q&A that pumped markets… only for them to dump in the last 30 minutes of the trading day to close below the open.

That pump and retrace or dump and retrace pattern has been a staple of FOMC days, but I was surprised to see it play out so violently today. Powell was as dovish as anyone could reasonably have expected or hoped.

"Evidence shows that policy is restrictive and is weighing on demand... I think it's clear that policy is restrictive... we believe over time it will be sufficiently restrictive."

"I'd say it's unlikely that our next policy move will be a hike."

He more or less came out and confirmed that the market’s repricing was realistic and in line with what the Fed is projecting. He announced the tapering of QT.

But the market didn’t buy? Why is that?

When you think the market should be bullish but it isn’t, that’s a cause for concern. It could mean a few things:

Positioning was so bullish leading into the event that a bullish outcome wasn’t enough for further pump (clearly not the case here)

You are misinterpreting something

You are missing something that the market is “thinking” about

You are early

So, basically, we are wrong or we are early. Neither one is a particularly attractive thing to be. I’m going to lay out a few more reasons why I think we are just a bit early below.

Inflation and Oil

A lot has been made of the “war” in the Middle East, the risk of sustained high oil prices, etc. I have been arguing that oil prices are not high and will come down. Today was a nice validation of that. Lowering oil prices should alleviate market’s fears of resurging inflation.

Granted, Core CPI, the Fed’s preferred measure, is not sensitive to oil prices. But it is sensitive to housing, transportation, and services. Services costs are sensitive to wages which are sensitive to consumer goods which are sensitive to oil. Transportation is sensitive to oil. Stripping out energy costs only gets you so far. A decrease in Oil prices lowers Core CPI.

The Saudis Are… The Champions of Regional Peace?

Big headlines today that everyone’s favorite butchers are close to reaching a comprehensive defense pact with the US.

In exchange, they would recognize Israel, and a bunch of other things that no one is saying aloud. Israel would be expected to reciprocate by ending the Gaza war and joining the US-led coalition to modernize the region. More peace, more money, in other words.

This will continue to drive oil down if it succeeds (it was, I’m sure, the cause of much of the drop in oil prices we’ve seen already). It will also help ease fears of regional conflict in the Middle East. This is big news that is quite bullish equity prices.

Markets may not realize it, but an aligned Saudi and Israel united with the backing of the United States would be a massive stabilizing force in the region. It would also probably make all parties involved quite a bit richer.

Yen Intervention, and A Weakening Dollar Will Buoy Equities

Michael Howellwrote a piece a few days ago about how the strong dollar has been holding up equities by bringing in lots of foreign investment. I commented on his piece to get some clarification, but I tend to believe it’s the opposite.

I did some quick research and found that Microsoft MSFT 0.00%↑ , Apple AAPL 0.00%↑ , and Google GOOG 0.00%↑ all do roughly 50% or more of their revenue outside the US. Such revenue is priced in non-dollar currencies, and when those currencies fall against the dollar it directly hurts Big Tech’s USD earnings here at home.

In general, a weaker dollar should be stimulative to equities. If you look throughout history you’ll see examples of this. The great bull run of the 1980s was kicked off after the dollar round tripped big gains and made new lows. The crash in 2001 correlated with the local top in DXY.

Given the US’ fiscal situation it’s only a matter of time before the dollar weakens. Deficits like the ones we are running are not conducive to a strong currency. I think the dollar is slowly starting to break out of its uptrend.

The BOJ has intervened twice this week to support the Yen. The BOJ/Yen situation deserves it’s own deep-dive, but I won’t get into it here.

That’s not to say I think the dollar will collapse, but I think a 3-5% correction is overdue. And when it comes, which may be soon, it will be a tailwind for equities.

Adding It Up

When I sit down and look at all the news of today in totality, I am bullish. I have been, and I continue to be.

I viewed today as a buying opportunity going into Powell’s FAQ (and I said so in the chat). After Powell’s FAQ, I continue to feel the same way.

Nevertheless, as a trader and an investor we have to honor the price action. And the price action has been complete shit.

I maintain some cautious optimism from here. It makes sense for the path to be rocky, but I think we are in the midst of sticking the landing, and US Equities will continue to outperform.

That’s all for now.

Please also always remember... none of this is financial advice. I’m not a professional. I quite literally don’t know what I’m doing.