Non-Farm Pre-View

Quick look at the day's events and a preview of NFP tomorrow

Author’s Note: I plan to continue releasing free content where I can provide value to everyone. Posts will include premium content for paid subscribers at the end of emails or as separate write-ups.

Quick update today: What to expect tomorrow from Non-Farm Payrolls, a few of today’s key events, and some trade ideas from the chat.

ISM Services Today

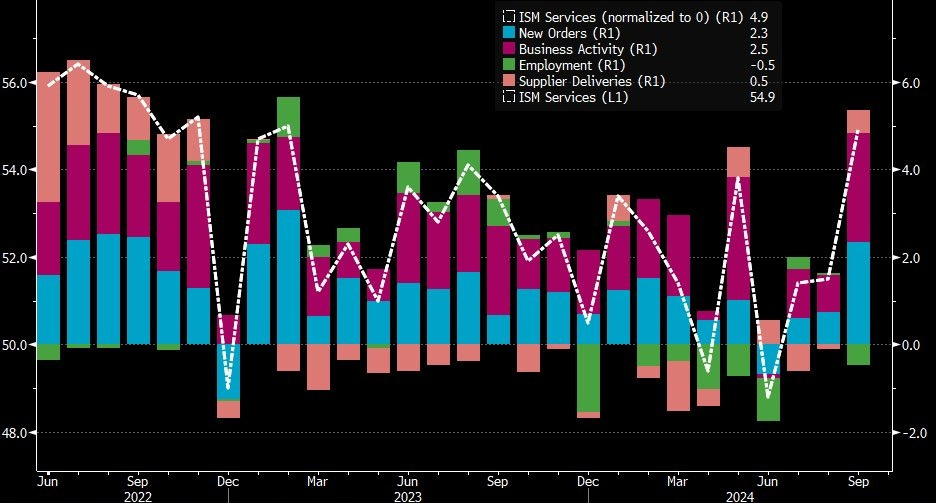

ISM Services came in white hot today, boding well for tomorrow’s NFP results and the state of the economy as a whole.

Confusingly, though, the employment component specifically came in colder than expected. The employment component is noisy and not nearly as important as the headline number, but with all eyes on Non-Farm Payrolls tomorrow I thought it was notable.

Weighted to their importance within the economy, this month’s ISM Manufacturing and ISM Services was the highest of the year.

Goldilocks personified.

Non-Farm Payrolls

Non-Farm Payrolls tomorrow are the main event of the week, with SPY straddles pricing in about a 1% move either way.

JPMorgan did a good job of breaking down the range of outcomes tomorrow.

I think they are mid-curving it a bit saying 200,000 jobs is worse than 180,000, but I doubt we’ll encounter either number.

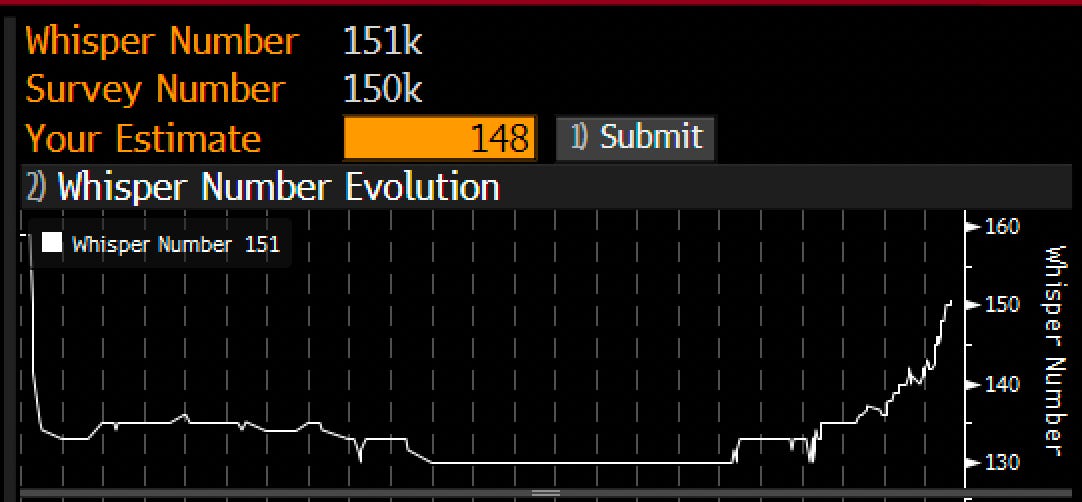

Bloomberg has a cool tool that shows the evolution of traders' best guesses for the print in the days before. At the close today, it crossed over 150k, higher than the economists’ estimates.

That tells us that traders are expecting a pretty good print. Normally we want to fade expectations, but equities haven’t run up at all into the release.

The recent economic data has been robust and paints a picture of a resilient economy that bottomed over the summer.

My general sense is that there is a lot of pessimism about Iran/Israel and the economy.

I think we can catch a bid on a solid NFP, but I’m concerned about selling into the close on Middle East fears. We will have to play it by ear tomorrow.

Port Strike and Biden Putting His Foot In His Mouth

I never wrote about the port strike because I never expected it to be a big event. And, it wasn’t, ending this afternoon.

That removes one tail risk to rebounding inflation.

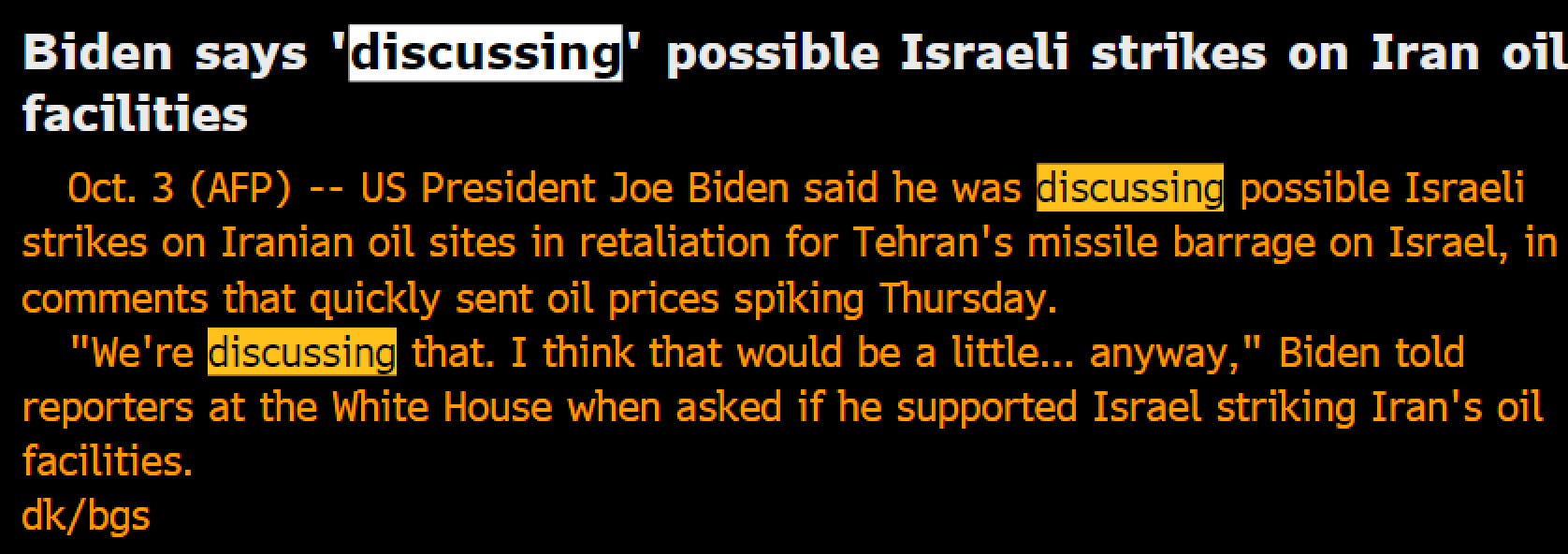

Meanwhile, Biden put his foot in his mouth today and hinted that Israel was in talks about hitting Iranian oil sites.

ISM Services had sparked a brief rally before that fun comment, but the rally quickly faded.

It is still implausible that Israel conducts a large-scale strike again Iranian oil infrastructure, but the market didn’t like hearing it was being discussed.

Some reasonable people see it differently, including Paulo Macro.

I don’t agree with this perception for the simple reason that I don’t think regime change helps Israel at all. Khomeini has been surprisingly willing to retaliate in ways that haven’t killed Israelis. Would the replacement leader behave the same?

Unlikely.

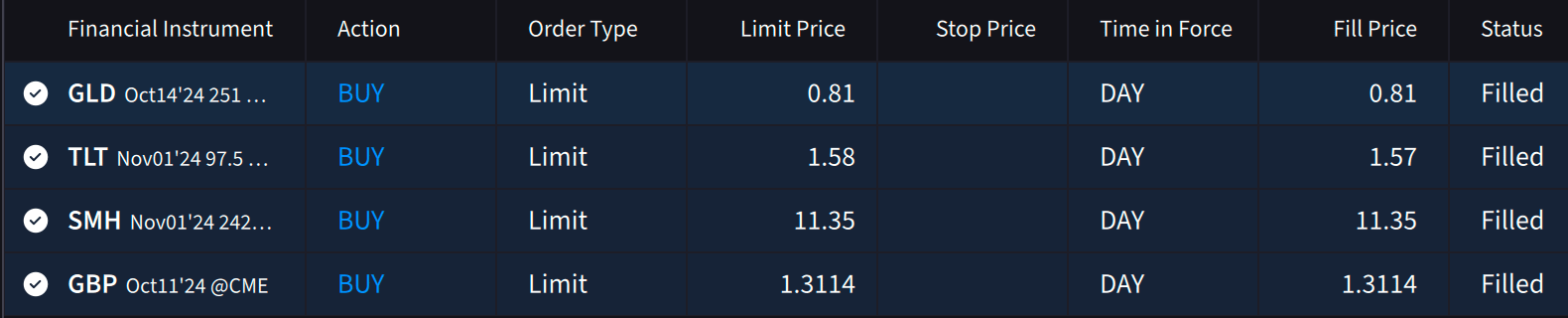

Trade Ideas From The Chat

Longed GLD with somewhat high convexity calls as a good GeoPol hedge that doesn’t involved chasing everyone headlong into oil.

We bought TLT puts because long bonds haven’t been able to catch a bid on war fears, which says to me that no one wants them.

We shorted GBP overnight on central bank comments from them about incoming easing.

And finally, we bought SMH calls. I am a big believer in the AI trade, and it has been lagging for a while. In my view, the Fed cutting into Goldilocks is the scenario in semiconductors, and AI stocks need to come back alive with a vengeance.

If you like the newsletter, please consider sharing it with someone who would enjoy it. It helps a lot. Good luck out there.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here. The information is presented for educational reasons only.