Sunday Round Up

The best charts and info I've found this week

If you have enjoyed Mind The Tape, please consider sharing your favorite posts, including this one, using the button below. It helps grow the community and helps me put out more of the content that you enjoy.

Today’s issue is a round-up of the best charts and information I found this weekend. When I cite a source for a chart, I highly recommend you check them out. Without further ado…

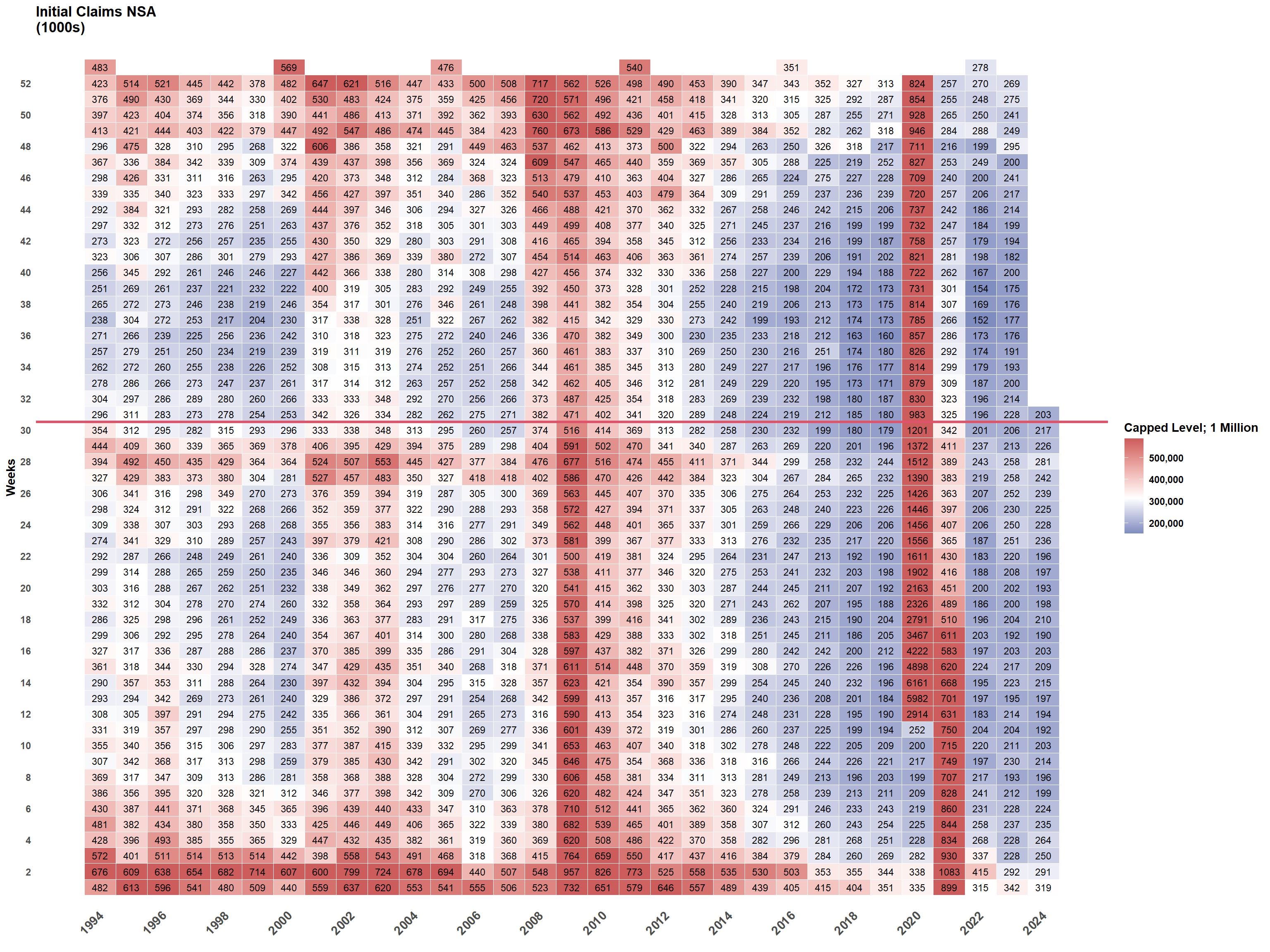

Here’s a chart from George Robertson of The Monetary Frontier. It shows the weekly initial jobless claims for each of the last 30 years. Red on the chart indicates high claims, while blue indicates low claims. The chart makes it very clear that we are in an anomalously strong job market, measured by unemployment claims, and have been on either side of the pandemic.

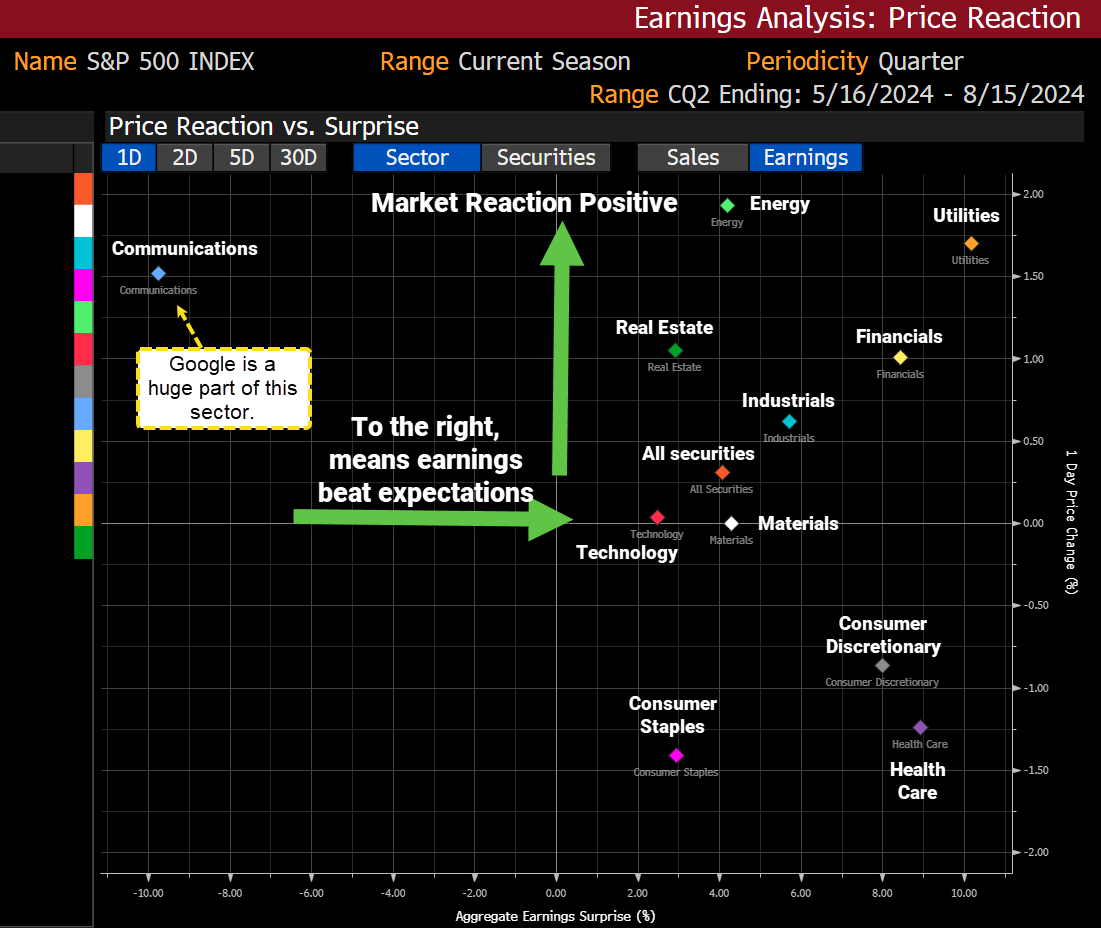

Earnings have continued to surprise to the upside more than the downside. As this chart from Kevin Muir shows, those surprises have not always been bullish for the price. Notably, the weakest reactions to earnings have come in Consumer Staples, Consumer Discretionary, and Health Care. The first two are most interesting, as the consumer's health is a big concern for the economy.

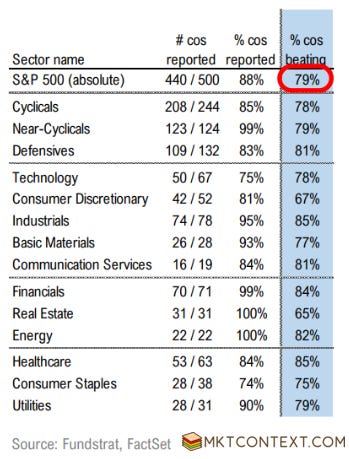

This related chart (from MktContext) shows the percentage of S&P 500 companies who have beat revenue by industry so far this earnings season. You can see that consumer discretionary is one of the worst-performing industries, with consumer staples just ahead. It's a little contradictory to Kevin’s chart, but directionally, they paint a similar picture.

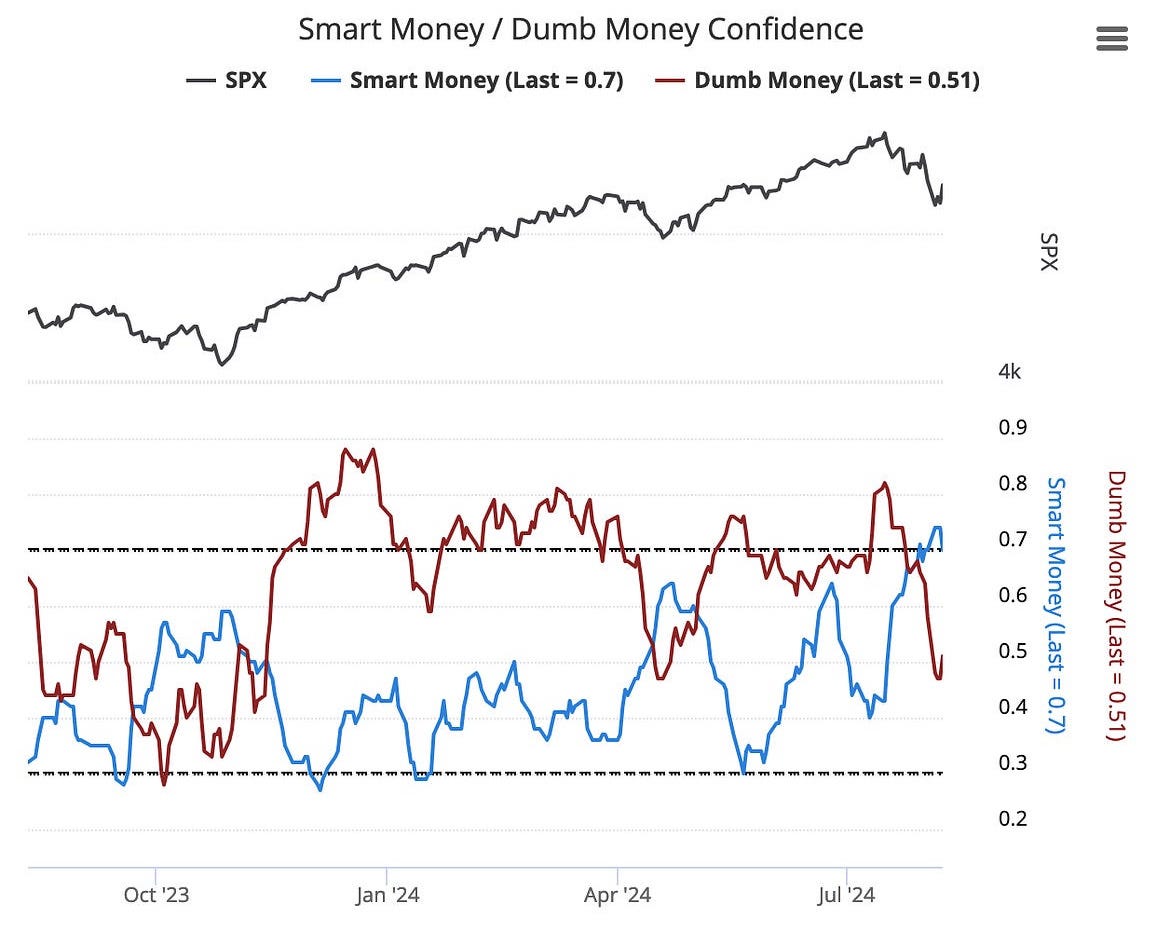

Thanks to SmartReversals for this one. This chart shows the current net exposure for asset managers considered “smart money” and asset managers/retail who could be considered “dumb money.” The chart speaks for itself but suggests it’s mostly the dumb money running for the hills over the last month.

There is no information on how “smart” vs. “dumb” is decided, so take it with a grain of salt. And we’ve learned before that sometimes the “smart” money is the dumbest money of all.

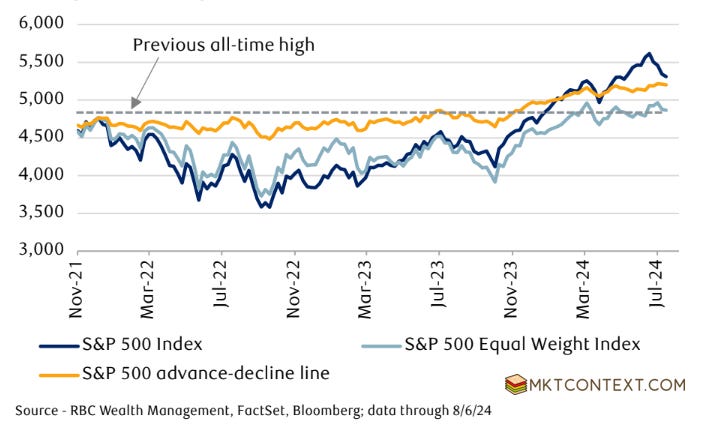

Thanks again to MktContext for this one. A lot of proverbial ink has been spilled all year about the ever-decreasing “breadth” of the bull run as the Mag 7 has pulled ahead while other names have lagged. That trend has been and is reversing. This could be a healthy sign that the correction is behind us and the market is ready to start climbing again.

Stealing this one from Le Shrub, who apparently stole it from BofA Global Research. This chart shows the weekly cumulative equity flows after various financial shocks. There are a few ways to read this chart. On the one hand, the fact that we saw net inflows after the events on August 5th puts us outside the realm of the worst events on this list. But I think the broader point is just as important: it takes time for these events to shake their way through the system and fully resolve.

Another chart from Shrub showing that seasonality is still working against us. August and September are historically red months. Obviously, that’s not decisive enough information to make a trade on, but it’s another reason to exercise caution.

What’s Ahead

Futures

As I write, futures are up small but mostly flat. USDJPY shows the Yen weakening slightly. Notably, the 1:1 correlation between risk and Yen seems to have subsided tonight.

The Data

This week has some interesting economic data in store for us. It’s going to be another sleepless week for us west-coasters.

PPI, CPI, and Retail Sales are the ones to watch. We are looking for Goldilocks numbers this week, IE in-line across the board. The death knell would be a hot CPI print accompanied by weak Retail Sales, as that would spell an inflationary recession, which the Fed is powerless to stop.

The World

China remains a bit of a black box and could become either a global headwind or a tailwind, depending on how things play out. Their economy, especially consumer spending, has slowed substantially this year. If China continues to slow and Beijing continues to be stingy with stimulus, that could drag down world economies. On the other hand, China could be expected to be a source of growing global liquidity in the near future.

You can read some of the latest news about China here.

The potential Israel-Iran conflict seems to have left the market’s consciousness. But on Sunday, some pundits suggested we should expect things to heat up there this week. I remain skeptical of that view, but it’s another thing to watch.

Good luck out there this week.

If you enjoyed this post, the most helpful thing you can do is share it with someone who would also enjoy it. I would really appreciate it.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here.