The Fed Almost Always Loses Inflation Battles

But this time is different™️

Last week was an unusual one with a surprising amount of volatility for a week where the VIX closes in the 12 handle.

I don’t think there was a lot of signal in the PA, with it having to do more with end-of-month strangeness than any fundamentals of this market. In fact, the fundamental data we got was fairly bullish, with GDP coming in a touch under expectations and PCE coming in exactly in line.

Not going to focus too much on what happened last week, but instead, I want to talk about the landscape of the Fed’s battle against inflation.

Inflation Battles

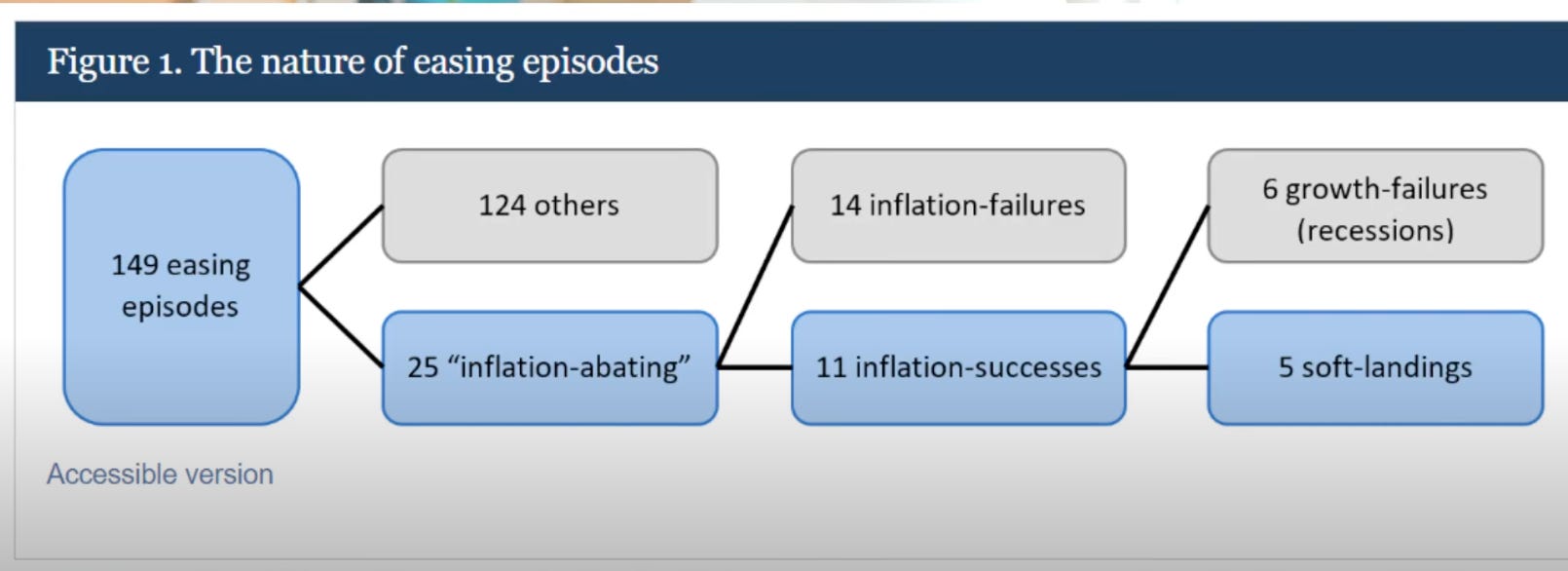

I grabbed this flow chart from Joseph Wang’s youtube video, because I found it quite interesting. The chart breaks down all Fed “easing episodes” and shows the results by category.

First, it excludes 124 easing episodes that did not involve inflation abating. Then, it shows that in a little over half of scenarios the fed easing resulted in “inflation-failures” or rebound inflation. Amongst the successful inflation scenarios (inflation did not recur), about half the time we end up in a recession.

It’s easy to see why, a year ago, everyone was quite pessimistic about the outcomes of the tightening cycle, and where we would be at during the subsequent easing. Only about 20% of similar tightening cycles have ended with a “soft landing” style easing.

Today, we are looking much more likely to be in the “soft landing” outcome as we see inflation come down, and growth stay strong.

That 20% “soft landing” outcome is looming much larger than ever.

How Markets Are Pricing This

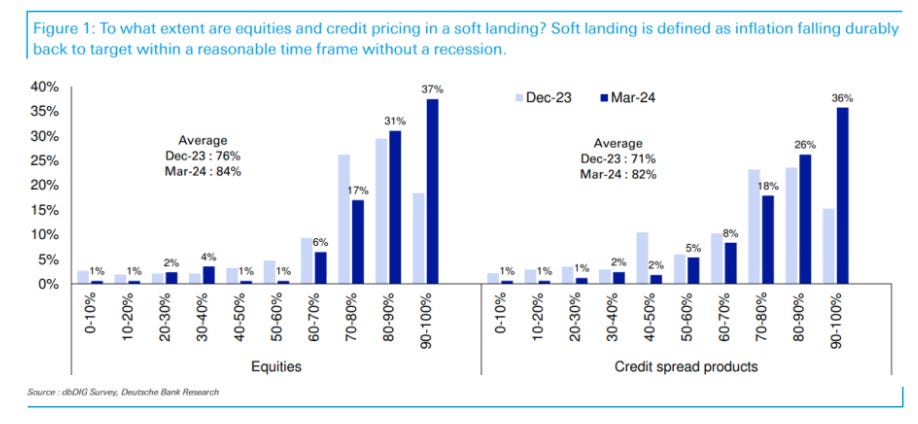

I found this old chart from Deutsche Bank from March showing how they were estimating markets to be pricing in a “soft landing.” Depending on the exact day you choose to look at, equity markets are a little bit above where they were at the time.

Yields, meanwhile, are up a bit with the 2 year yield up around 4-7%.

2Y yields are a decent proxy for inflation expectations (there are some better proxies out there but they’re harder to look up).

But, put simply, equity markets are pricing in about the same level of “fed success” today as they were in March while the bond markets price in a little less.

Thinking It Through

Knowing that the market is pricing in such a high percentage chance of a soft landing is interesting, but it shouldn’t surprise anyone who has been paying attention. The broader question is, how do we make money with this?

I’m going to use this as an opportunity to illustrate why being bearish is kind of dumb as a general practice.

Lot’s of math to follow, so if you’re not big on “showing your work” just skip to the end.

For round numbers, let’s assume the market is pricing in an 80% chance of a soft landing and a 20% chance of an inflation-failure (which is significantly worse for equities than a recession).

Let’s also pretend that, in our wisdom, we know for a certainty that the true odds are closer to 60/40. We have identified that an inflation-failure is twice as likely as the market thinks!

When there is an inflation-failure, let’s assume the market drops 15% the remainder of 2024 and regains about 6% through 2025.

When there is not an inflation failure let’s assume the markets go up a healthy 10% each year.

No More Math From Here

If you math out the probabilities here, assuming the bullish strategy means “holding through it all” and the bearish strategy means “Waiting for a 15% dip, and buying the bottom if it comes, but otherwise holding short” you see that the bearish strategy… loses money on average?

The reason for that is because when you’re bearish you still frequently find yourself wrong and losing money waiting for a dip that doesn’t come.

That’s a really important thing to understand, and this is coming from someone who started their trading career as basically a short-only guy.

Now, you can get some much better bets down than just outright shorting the stocks, and certainly you can make some money on the short side (we will someday in this Substack, i’m sure). But that core concept is really, really important.

You should be default-bullish unless you have a really good reason.

Especially because there is something called reflexivity in markets.

Outperforming the Index

So how do we outperform the indexes if all we do is stay unlevered long?

Well, we don’t, which is why that’s not all you should do. It should, however, be your default.

And, in fact, in a world of deteriorating fiscal policy I’d argue that you need to be long something high beta most of the time to increase your wealth at all.

Thank you for this clear concise piece. We really need to reiterate common sense from time to time to remind ourselves. The math section was pretty funny XD