The Momentum Unwind

Are we entering a growth scare, a correction, or up only from here?

Author’s Note: I will continue releasing free content where I can provide value to everyone. Posts will include premium content for paid subscribers at the end of emails or as separate write-ups. Free content will focus on macro views, whereas the paid content will focus more on the tactical trades I’m making.

Serious traders or investors should join Premium to get the best, most timely information.

I wanted to write a quick note about the momentum unwind and its’ potential consequences for markets.

If you’re not familiar with momentum or other factors like growth, value, etc., check out my previous piece, where I explained them.

“Momentum” is pretty intuitive—when we talk about momentum stocks (or momo) we are talking about stocks that have outperformed over some recent-ish period, maybe the last 3-6 months or so.

Momentum has been the best performing “category” or “attribute” for equities for quite a while now. Because it has performed well to long stocks that have been doing consistently well, that trade has caught the notice of trend followers and there are now algos managing many $Bs that look at momentum to choose names to buy.

We can’t know exactly how much money chases these “momo” trends but we know it’s substantial just because of how big the moves are in some of these names.

TSLA 0.00%↑ was a big momentum name in Q4 last year, and in early December it went on such a bull run that it actually distorted the market in a bunch of ways, quite literally sucking all of the liquidity out of indexes such that anyone long non-momo stocks got hammered.

PLTR 0.00%↑ has been another big momentum name, going on a massive tear after its’ last earnings call.

HIMS 0.00%↑ has been another big momentum name.

If you look closely at these charts they all have one thing in common: In the last 3 months they’ve all experienced big blow-off tops.

MoMo NoMore (please forgive this horrible pun)

Last week was February OpEx. In general OpEx has been a bearish week for equities, and the sell-off from the ATHs wasn’t hugely unexpected. Generally however the sell-offs don’t continue, but we saw follow through today.

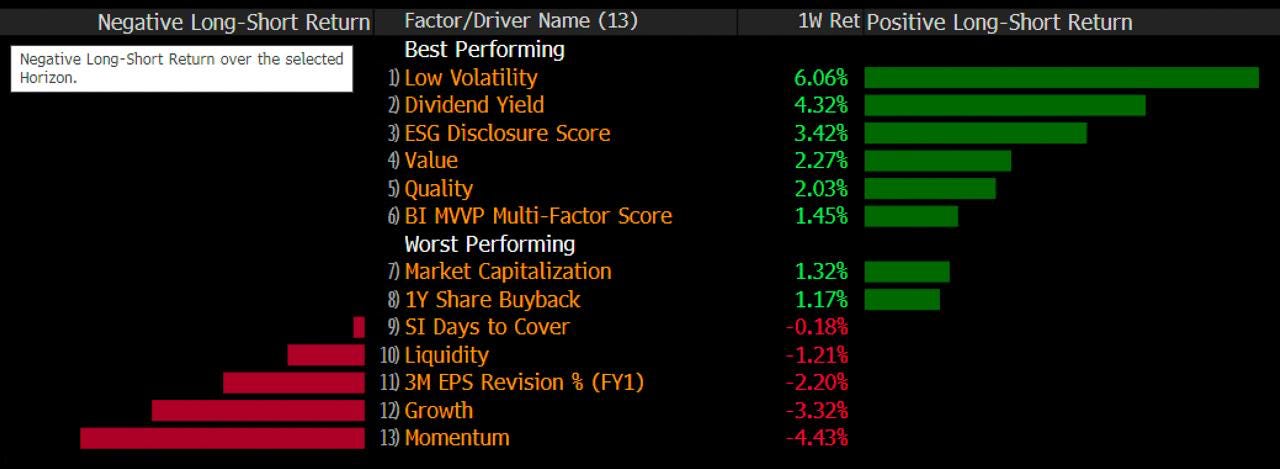

The chart above shows how various factors have performed week to date. Momentum, Growth, and 3 M EPS Revision were all slaughtered in favor of low volatility, dividend yield, quality, etc.

This is notable for two reasons:

Firstly, it’s notable because this is a complete reversal of what has been working recently and for the last few years.

Secondly, it’s notable because it might imply what investors are expecting. IE, maybe investors are preparing to rotate more heavily into these “defensive” stocks because of some macro concerns.

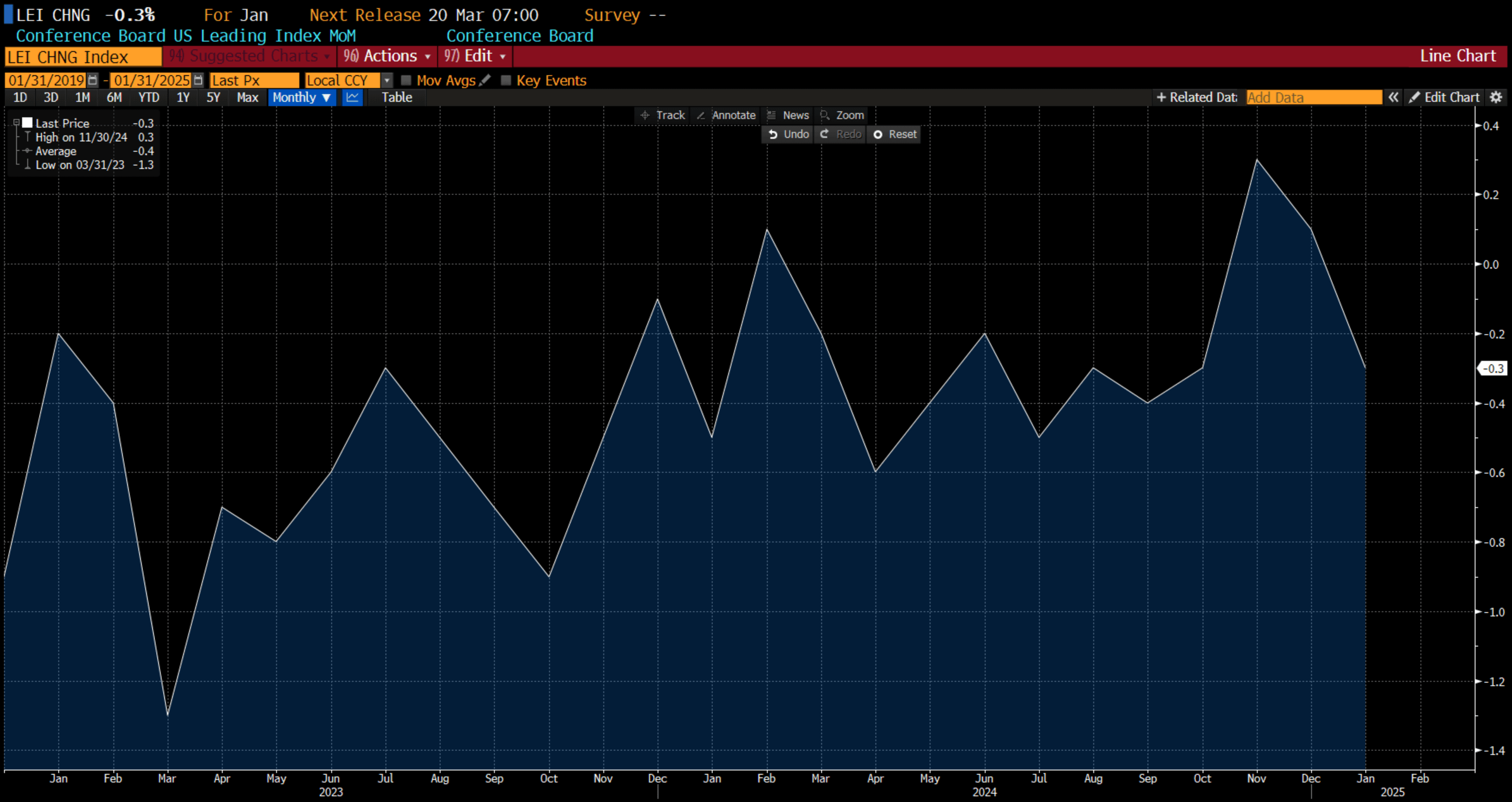

The timing is notable. Not only was it OpEx last week, but we got a variety of not-so-great macro data. That bad macro data comes on the heels of a sequence of bad macro data that has driven the Conference Board Leading Indicator Index (a collection of leading economic indicators) down to pre-Trump levels.

This chart shows the momentum factor’s performance over the last few years. I’ve shaded the significant momentum drawdowns in red. The most recent one, the one we are currently in the midst of, is in white.

It’s interesting to note the steepness of the sell-off. While the depth of selling has not been especially dramatic, the speed of selling has been dramatic.

Bull Markets Don’t Die of Old Age (They’re Murdered By The Fed)

When you put all of this together one of a few things could be happening:

This is a regular ol’ degrossing. Healthy, bullish selling, in other words. Some of the momo names got overheated, and now they are corrected, and it’ll be business as usual soon. One of the best traders I know thinks this way (shoutout Lord Fed).

This is the start of a broader rotation driven by macro factors.

Number one is easy to understand, and it’s the most likely. But let’s take a look at number two for a minute.

With value and defensives outperforming last week after soft economic data it makes sense to assume that the market is pricing some amount of economic slowdown.

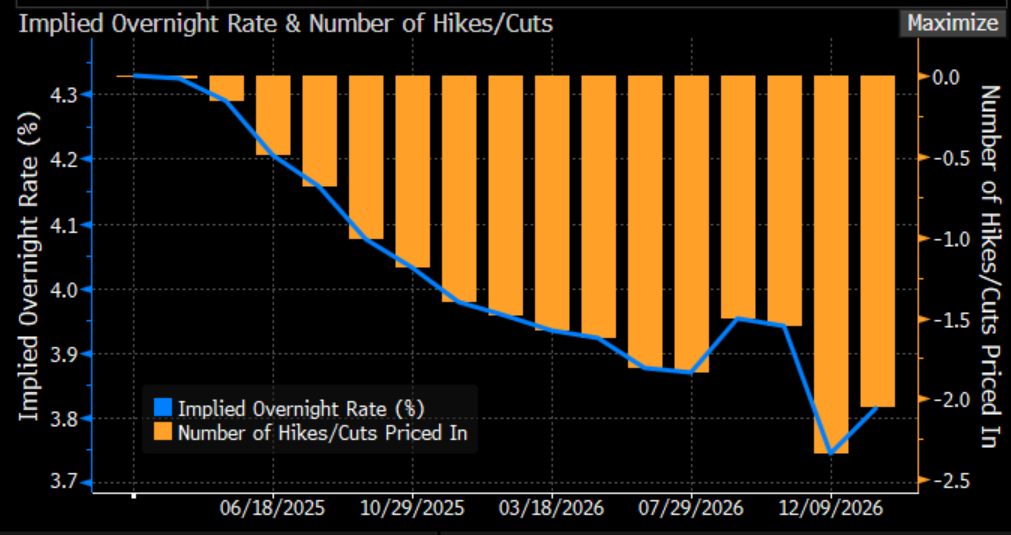

At the same time as the market was digesting that possibility we hit peak Fed-hawkishness fears.

In other words, last week, markets were grappling with the idea that we might see less than 1.5 rate cuts this year while economic data is deteriorating…

They were concerned that the bull market was doomed to be murdered by the Fed.

Evolving Expectations

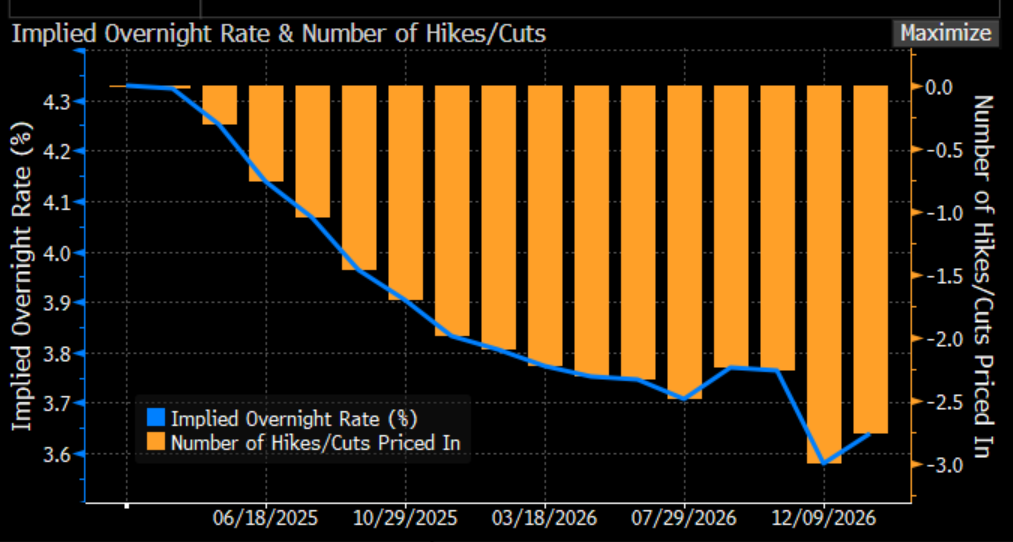

The good news is that hawkish rate sentiment has reversed some. Markets have priced in an extra ~20bps of cuts this year. I believe they’ll continue to price in more until we have three cuts this year.

If we continue to see high inflation and soft economic data, it’s reasonable to assume that a hawkish Fed will end this bull run. That’s something to watch out for.

And this bull run was, in my opinion, always going to end with the most epic momentum unwind of all time.

Maybe we’re seeing the start of that. Maybe we’re seeing the start of that. Or maybe it’s a hiccup. The truth is anyone who tells you they know for sure is lying.

My current base case is that this is a hiccup, and Momo might be worth a knife catch here or soon. Call me an optimist, but I’m a huge believer in AI, a skeptic of sustained inflation, and a believer in the robustness of the US economy.

Nonetheless, I’ve degrossed considerably. Not so much because I think we are headed for a bad outcome but because I think the ingredients are in place for a hiccup in equities that might quickly take us down 5-10%. It’s worth remembering that corrections like that are commonplace in bull markets.

I’ll be watching the momentum factor closely.

Good luck out there.

P.S. It’s good to be back

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here. The information is presented for educational reasons only. Investment positions listed in the newsletter may be exited or adjusted without notice.