The Stock Market Is The Economy

And the economy is the stock market

Author’s Note: I plan to continue releasing free content where I can provide value to everyone. Posts will include premium content for paid subscribers at the end of emails or as separate write-ups.

The Fed cut 50bps exactly as we predicted on Tuesday. It’s always scary to put your calls out there in real-time, especially for a binary event like the Fed rate cut.

If you’re wrong, you’re going to be exposed in a heroic fashion very quickly. If you’re right…

Well if you’re right, probably no one will notice.

Let’s check in on those calls in detail.

Accountability Corner

I’m quoting directly from the post, which is a pretty good clue that the predictions were good!

50bps

How many times have you had a friend bring you an impossible dilemma, one which they feel utterly unequipped to handle, asking for your advice? It’s probably happened a thousand times.

As often as not you know the choice they are going to make before they do. Even as you watch them agonize over the decision.

That’s a bit how I feel about the Fed this week. They may well be inwardly torn, but I believe Powell wants to cut 50bps, and I see no reason to believe Powell won’t get what he wants in the end.

Powell wanted 50bps, he got 50bps. How did I know he wanted 50bps? A few reasons:

Powell’s Jackson Hole speech made it very clear that he is watching and worried about the jobs data.

The July NFP report came out a few days after the Fed decided not to cut. It was pretty clear to me that, had they had that report, they would have cut.

Powell likes to overweight data in the Beige Book. The last Beige Book was the worst since 2020.

The whispers talking us up to 50bps that came out last Friday could really have only come from Powell.

The Big Reversal

The Fed essentially says “Goldilocks at any cost,” implying that they are 100% committed to doing what it takes to avoid a recession.

The market listens.

We start to see a reversal of all the trends I discussed above. QQQ becomes a favored son again, commodities begin to rip, bonds reverse, and all the “defensives” see a sharp deflation.

Gold first rallies on the news, before starting a bleeding process that confounds everyone. Maybe it even sharply sells off. Why? Positioning…

…

It’s time for a reversal.

A few calls in here.

QQQ becomes favored son

Commodities begin to rip

Bonds reverse

Defensives see a sharp deflation

Gold spikes than sells off

In terms of actionability, the QQQ call was the big one, followed by short bonds, then long commodities, then not overstaying our welcome in Gold, and finally the retrace in defensives.

Members of the chat got the tactical details on those calls in real-time. Join below if you want the same.

I’m gonna give us 3.5/5 on this part. More importantly, 3/3 on the actual trades we put on, which we are all focused on longing QQQ/Commodities and shorting Bonds.

The Economy

Over the last two weeks, we have taken meaningful steps towards Goldilocks. Still, I think it’s a good time to check in on the economy.

Obviously, job data has been weak. Non-farm Payrolls are considered a “coincident indicator” in that they explain the current state of the economy but do not necessarily predict its direction.

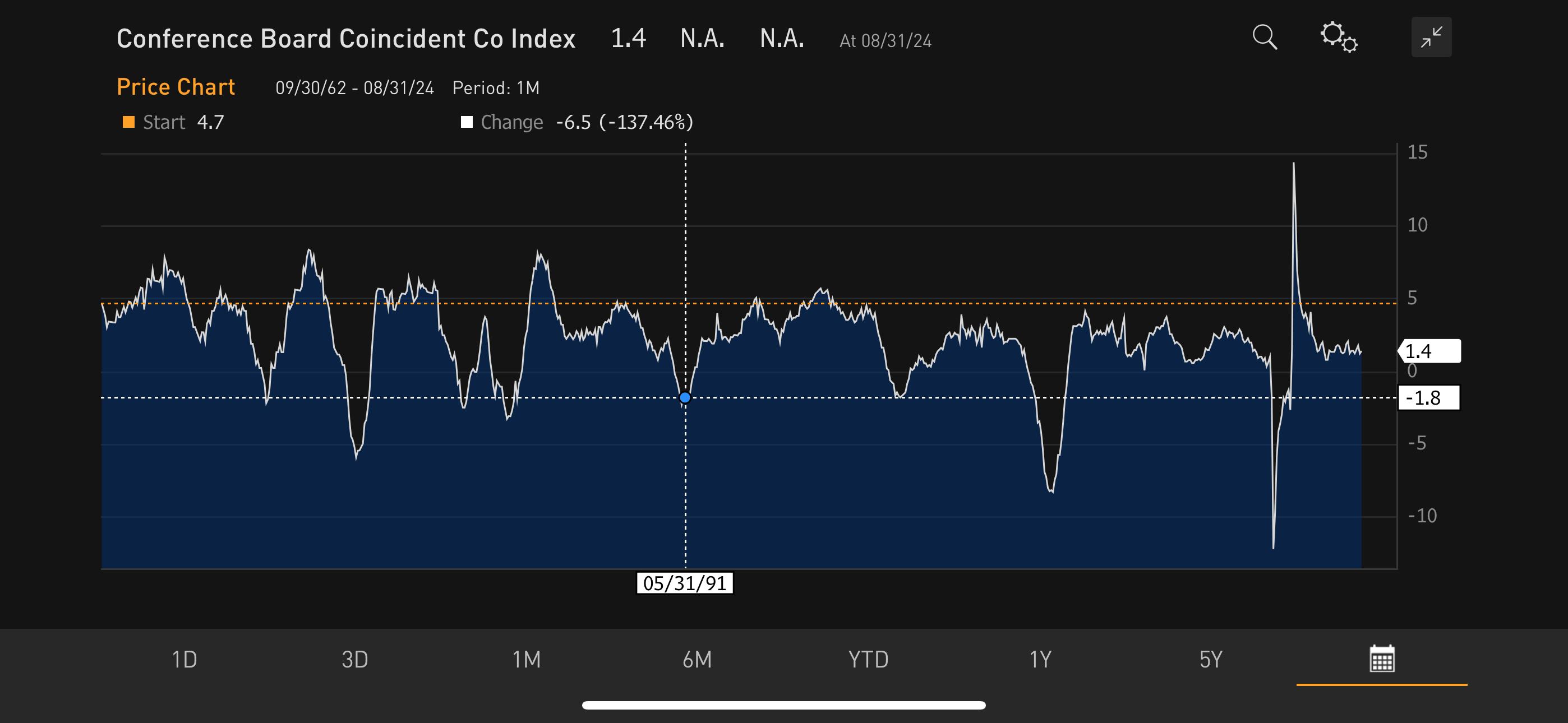

A weighted index of coincident indicators paints a fairly robust current picture of the economy, even as NFP reports have continued to weaken.

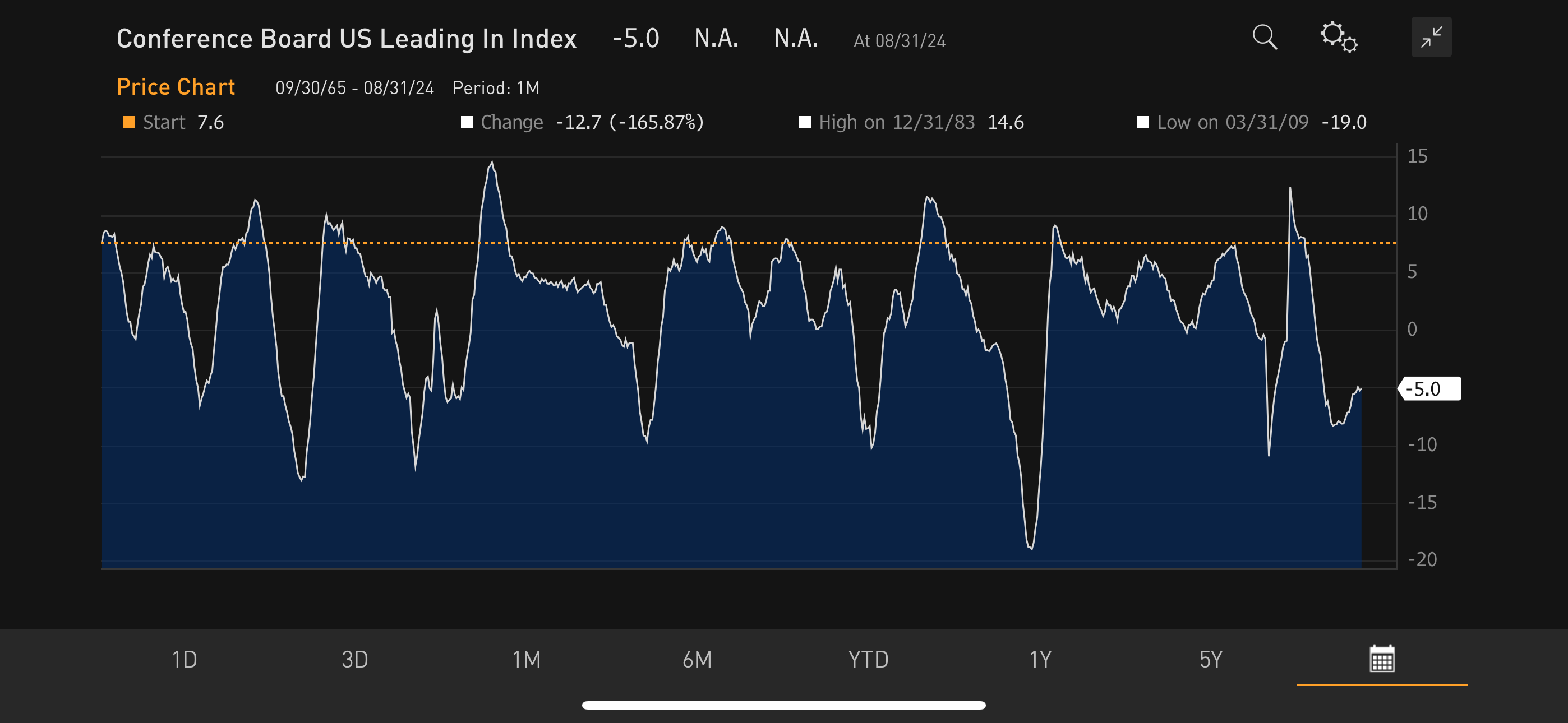

Meanwhile, leading indicators have actually been ticking upwards, albeit from low levels.

Over at Variant Perception they are seeing the same thing, with their leading indicators ticking upwards after making lows earlier this year.

Why they compare it in their chart to the Conference Board coincident index instead of the Conference Board leading index is beyond me.

Maybe the two look a little too similar if they do that.

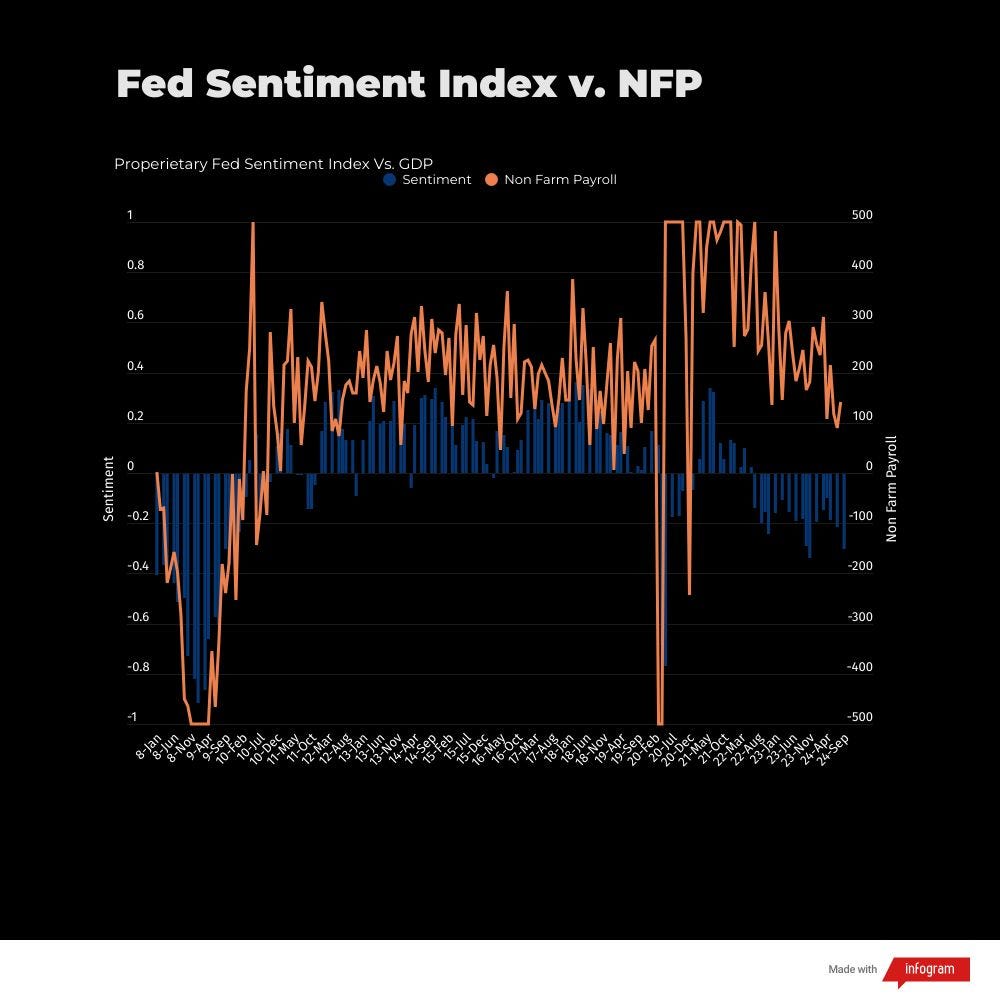

This data does not match my proprietary indicator, which is at its lowest level since the Fed Pivot in 2023.

This indicator is a big part of why I have argued that the Fed needs to cut 50bps. The last time we were at this level, Powell pivoted, the data began to improve, and stocks went on a heroic run.

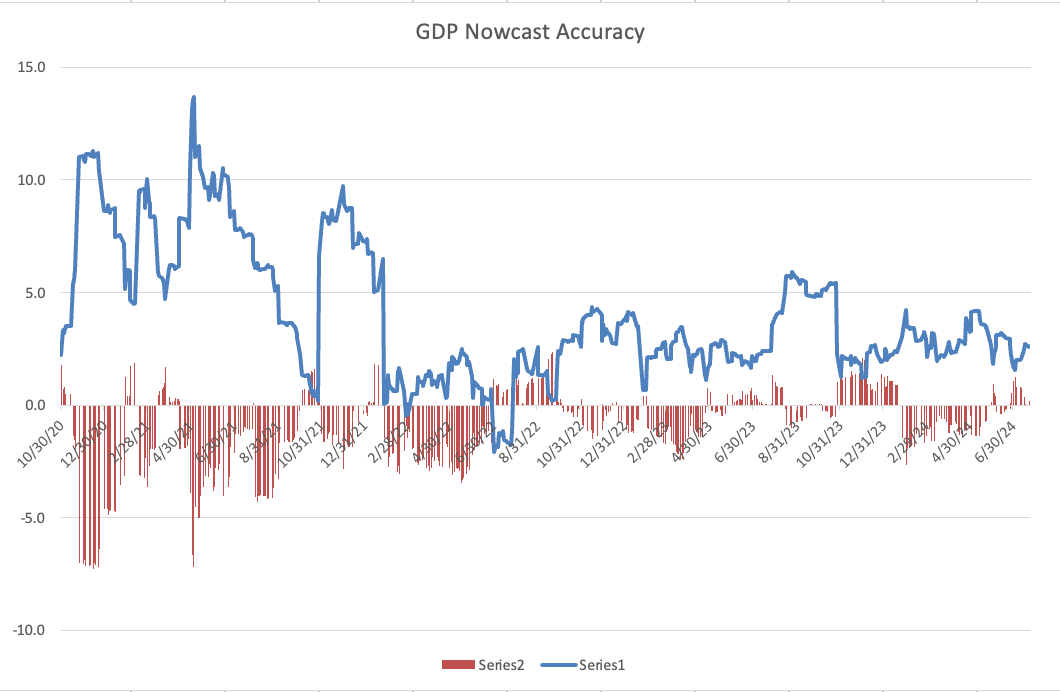

GDP Nowcast

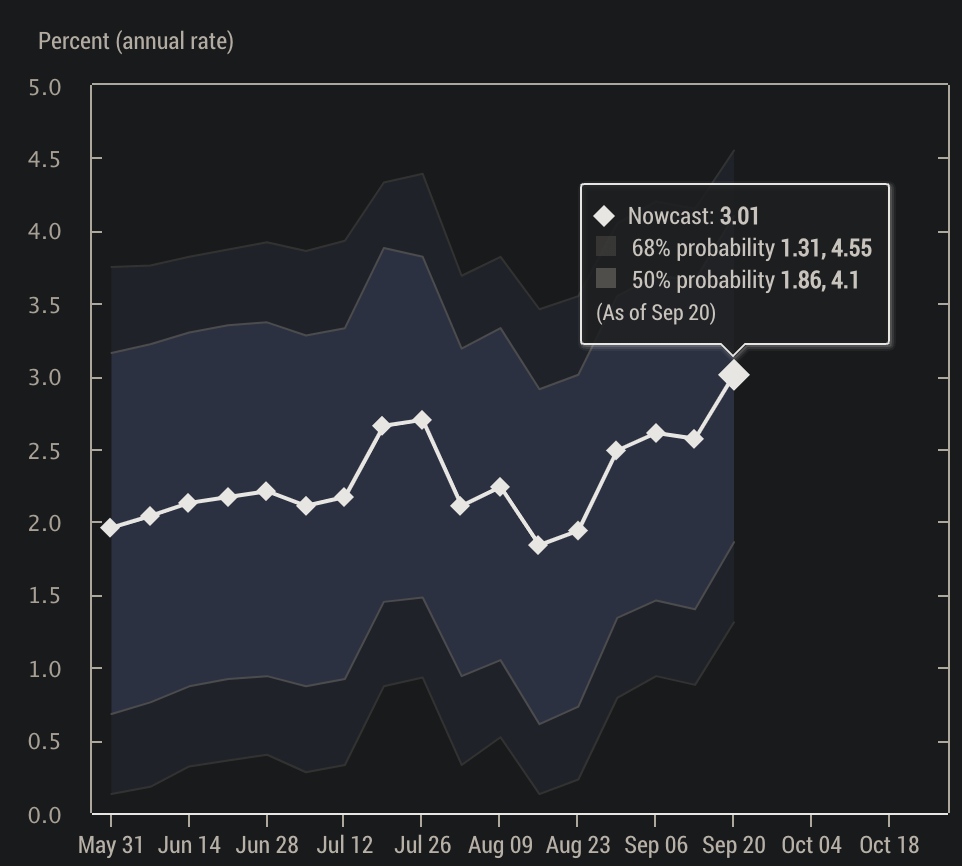

We got an excellent GDP Nowcast release from the New York Fed today.

Their estimate of GDP is ticking up strongly from the August lows.

It’s important to remember that a Nowcast is an error-prone forecast. Below is a chart of previous nowcasts with red error bars showing how much the final number differed from their projections.

This is what makes it so difficult to rely on these real-time data points. They won’t deteriorate until we sense that things are deteriorating elsewhere.

Powell Presser

"Intuitively, most — many, many people anyway — would say we are probably not going back to that era where there were trillions of dollars of sovereign bonds trading at negative rates, long-term bonds trading at negative rates. My own sense is that we are not going back to that.”

This quote stood out in the Powell Presser. It’s one of many quotes in which Powell tried to counter the idea that we are returning to the era of free money. That led plenty of commentators to describe the Fed’s move as a “hawkish 50bps,” which, as put so succinctly today, doesn’t exist.

Powell’s protestations remind me of a situation that comes up when you’re dating a girl. When you’re on a date, and the girl tells you, “I don’t sleep with guys on the first date,” a young man will think, “damn, I guess I’m not getting any tonight,” whereas an experienced guy will realize that his chances just went up. The fact that she’s talking about it at all increased the odds and the more you can get her to talk about it, the better.

My read on Powell is the same. The more he gets out there and tells us how we aren’t going to maintain this pace of cutting, the more he talks about how we aren’t going back to the era of free money, the more likely it is we head there in a hurry.

Partly, this is just a matter of conditional probability. He is only talking about it because it is looming ever closer.

There is also some market psychology involved. The more he says it, the less inflation expectations are entrenched, and the more likely he is to be able to do it eventually.

We need interest rates to get low before people freak out about the fiscal situation. That “people freak out about the fiscal situation” is an ever-looming concern over the head of the Fed and the Treasury.

The tougher Powell talks, the looser he can be.

Pun intended.

Looking Forward

As we head into the next week, we should take a second to appreciate where we are. Thursday was my best trading day ever. We have correctly called:

Sell the Nonfarm Payrolls in July.

Buy the dip in August.

Don’t get shaken out on the previous round of recession fears

Fed 50bps

Now, we are staring down the barrel of an actual Goldilocks outcome.

Next week is one of the quietest for economic data in a long time. There are many prints of middling importance, none of which are likely to be big movers.

I remain long equities (especially large-cap tech), long commodities, and short bonds.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here. The information is presented for educational reasons only.

Good thoughts. What's also interesting is that there is another 75bps worth of cuts priced into the next 2 meetings by the end of the year.