Victory Lap

Let's take a moment to enjoy and jinx ourselves

I’ve been writing a lot about Goldilocks, inflation rolling over, and risk assets being the place to be, even as all the other people I follow have warned for caution (with a few notable exceptions).

Here’s a quote from my April 17th post. Granted, it took a bit longer than I forecasted.

What will happen is one day soon everyone will wake up and decide that it’s over. We will have a 150 bps up day in the indexes, a 8% day in BTC etc.

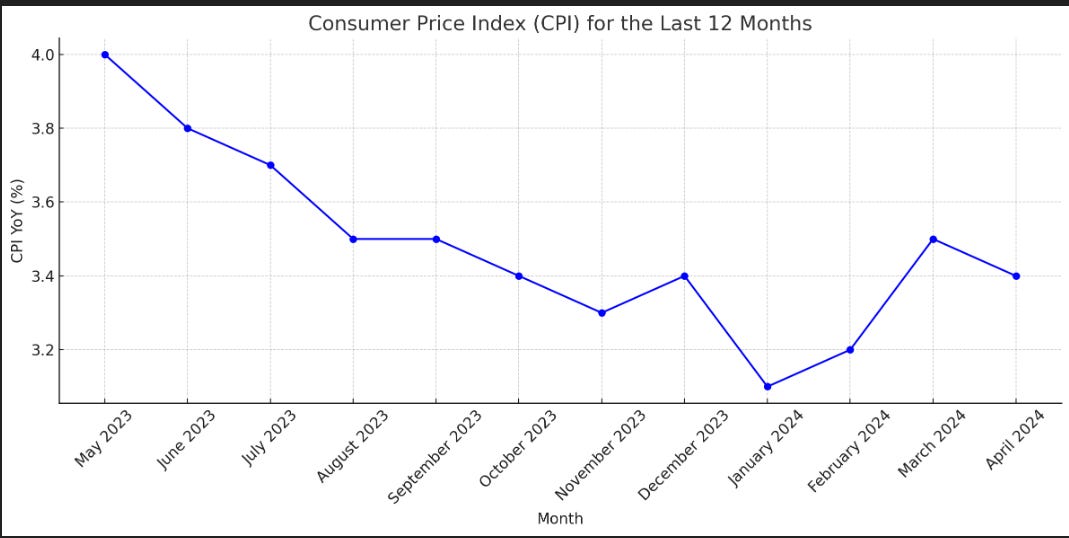

And here is a chart of today.

Can you spot the CPI print?

Digging In

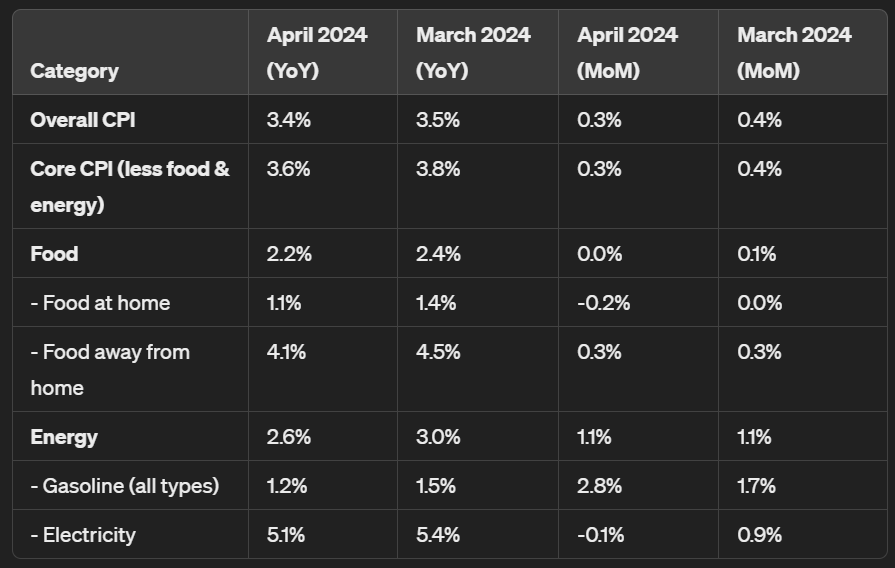

Now that I’ve thoroughly jinxed us, let’s look at the CPI print and see what we can come up with. Here’s a few charts:

You can certainly see why the market reaction was euphoric. After the last CPI we were looking at what might have been the beginning of a trend shift. Now, we are looking at something that looks much more like an aberration.

Core CPI looks even better, and keep in mind that the MoM numbers are seasonally adjusted.

Powell has been banging the drum that policy is “sufficiently restrictive,” starting at the Fed Meeting May 1st, which is something I’ve agreed with.

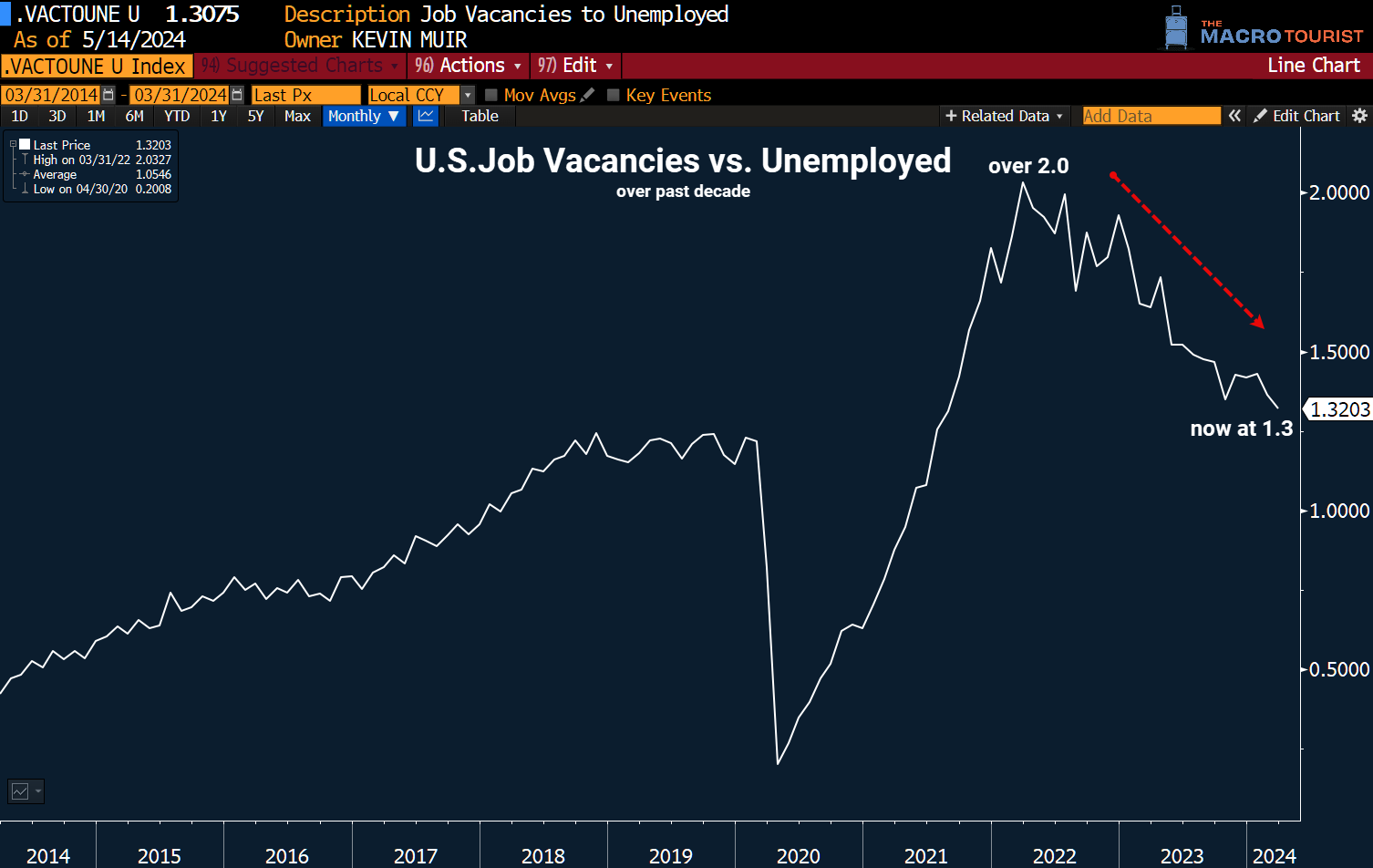

The exceptional Kevin Muir has some great charts in his post from yesterday where he discusses whether or not Powell is right. I’m going to steal a few, I hope Kevin doesn’t mind.

Powell has explicitly mentioned that the labor market is cooling off. Below is the ratio of vacancies to unemployed people.

Powell has discussed wages deflating, below is a chart showing that.

And this last one is an important labor market sentiment indicator, it’s the number of people quitting their job. Usually you don’t quit your job unless two things are true:

You’re confident you can find another, better job

You have enough savings to live on while you look, etc.

What Do These Charts Mean?

It’s very difficult for anyone to have looked at these charts and not believe that policy is “sufficiently restrictive.”

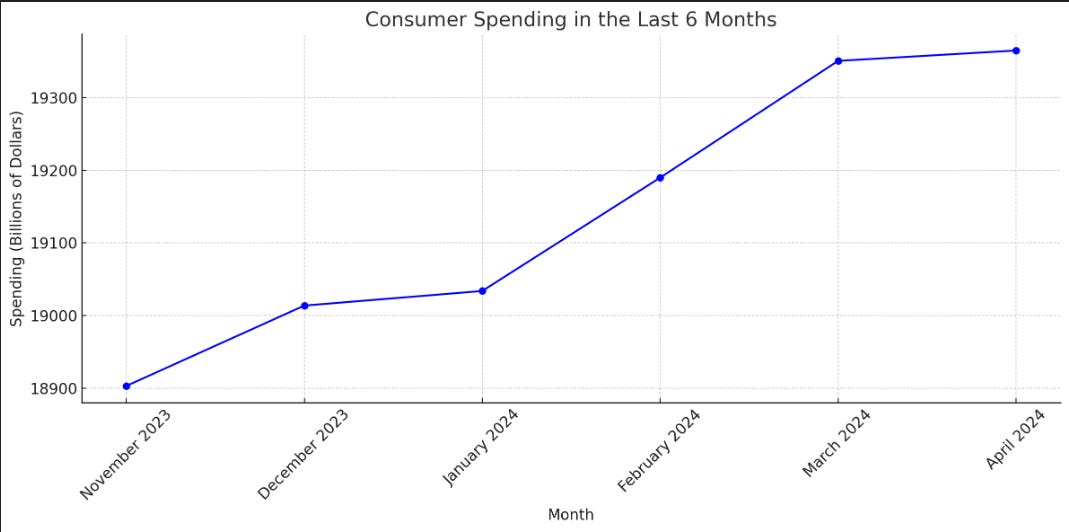

I’ve written this elsewhere many times but the health of the US consumer is the health of the US economy. Consumer spending, which includes expenditures on goods and services by households, accounts for approximately 70% of the U.S. Gross Domestic Product. 70%!

And the health of the US consumer is entirely dependent on the job market.

There are some caveats to that, which have actually contributed this time around to a bumpier move down than you might otherwise expect. For instance, the health of the US consumer is also the health of the housing market, because a strong housing market leads to a powerful “wealth effect” and during this hiking cycle the housing market has been artificially propped up by people having locked in low rates.

But at the end of the day if the average US consumer is earning less then the economy will swing downwards.

So far consumer spending is staying pretty healthy. That might seem a bit surprising given the job data above, but remember that so far we are simply cooling from a very hot job market.

What Next?

So, we were right about inflation. We made a good call, and now we need to think about what is next.

In my last piece I argued for 6 months of Goldilocks. Something like that is still my base case. But we need to continue to watch two things:

How much is the economy slowing, and is it going to get bad enough to affect risk assets?

What sorts of exogenous shocks could startle markets and send us on a leg down.

So far I’m seeing some rumblings about point1, but nothing that concerns me. This is important to continue to monitor.

A good measure of how much we need to worry about this will be watching how the market reacts to “bad” economic news. Do we pump or drop on high jobless claims? Do we pump or drop on a high unemployment number? Etc. That’s a good proxy for understanding what the market is paying attention to.

Point 2 is more difficult. There are multiple land wars in the world at the moment that could blow over into larger, regional conflicts. There is Taiwan. There are unseen stresses in the banking system. Hell, there’s the ever present threat of an accidental nuclear conflict.

In theory, spotting these things before they happen is one of our strong suits. I spotted and traded Covid, and the Ukraine invasion well. But there are no guarantees, and that’s why we aren’t big believers in leverage here.

So we will continue to watch both concerns above, and stay long risk assets.

What’s Next Here at Mind The Tape

Citrini is really great at identifying thematic trends and capitalizing on them to do better than the market. I would like to start coupling my macro approach to identifying what types of assets we want to own with narrowing in more specifically on ones that will outperform the category. Hopefully I’ll have some work on that for you all soon.

Good luck out there.

Please also always remember... none of this is financial advice. I’m not a professional. I quite literally don’t know what I’m doing.