What is Happening?

Making sense of the week behind us

Author’s Note: I recently enabled paid subscriptions. I have not yet decided how to divide free vs. paid content. My main goal is to grow a community here where we can learn and discuss together. The plan is to have free content where I can provide value to everyone. Eventually, I will experiment with adding paid sections to the end of posts.

If you want to support me with a paid subscription, I will make sure I provide value. If you don’t or can’t, just know that I still appreciate you and will make sure you’re getting the valuable insights you signed up for too.

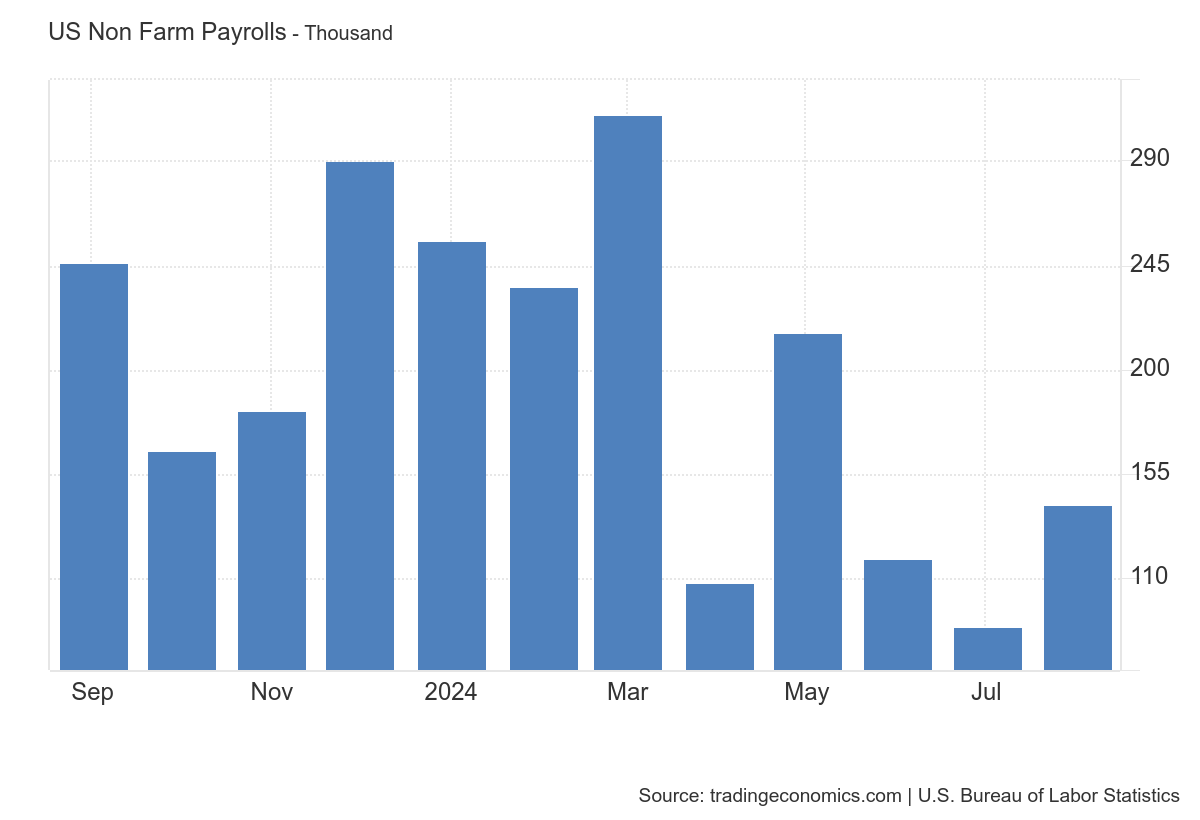

First things first, we got Non-Farm Payrolls today. According to the BLS:

Total nonfarm payroll employment increased by 142,000 in August , and the unemployment rate changed little at 4.2 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in construction and health care.

This came in below the market’s expected 165,000, and was one of the lower prints for the year.

Furthermore, the BLS actually revised June and July downward.

The change in total nonfarm payroll employment for June was revised down by 61,000, from +179,000 to +118,000, and the change for July was revised down by 25,000, from +114,000 to +89,000. With these revisions, employment in June and July combined is 86,000 lower than previously reported.

There was a lot of reason to believe that actually, expectations for the print going into it were lower.

Bloomberg’s “whisper number” Thursday evening was around 155k. That’s Bloomberg’s assessment of what traders are actually pricing in for the print.

With stocks having sold off and experienced volatility all week, I reckoned the “acceptable” number to be lower, around 145k.

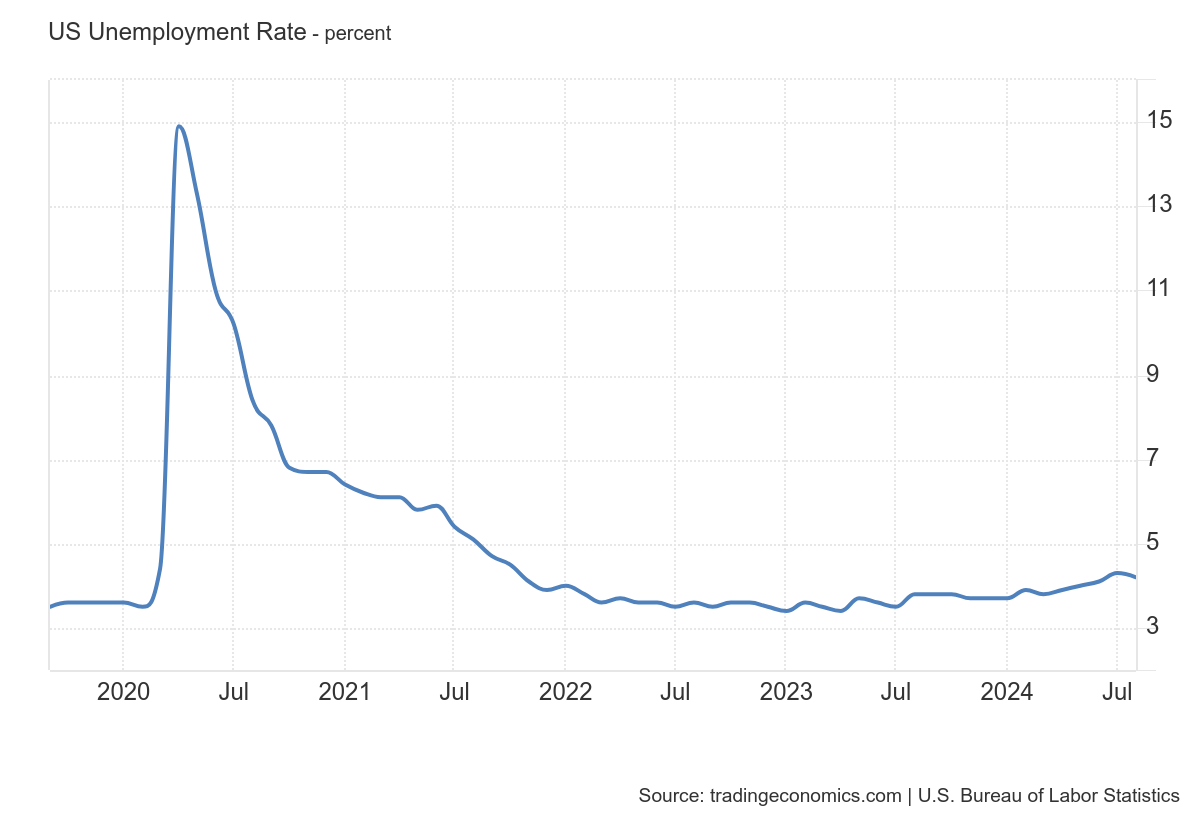

Importantly, everyone hoped to see unemployment move back down to 4.2 percent, which it did.

That’s a nice, but uncertain break to the upward trend that has been forming the last few months.

Nevertheless markets reacted badly, in what has become familiar fashion on these economic data days the last 6 weeks.

The major indexes and BTC all finished the day on the lows, with continued selling after hours.

Stole this from the excellent

Kevin Muir

.

It’s genuinely notable to see this PA to end the day because it’s been so unusual all year.

Yields

In the background of the drama playing out in equities, quite a bit was happening in bonds as well.

Yields moved around violently after the number, with the 2Y and 5Y eventually gaining to give us lower yields.

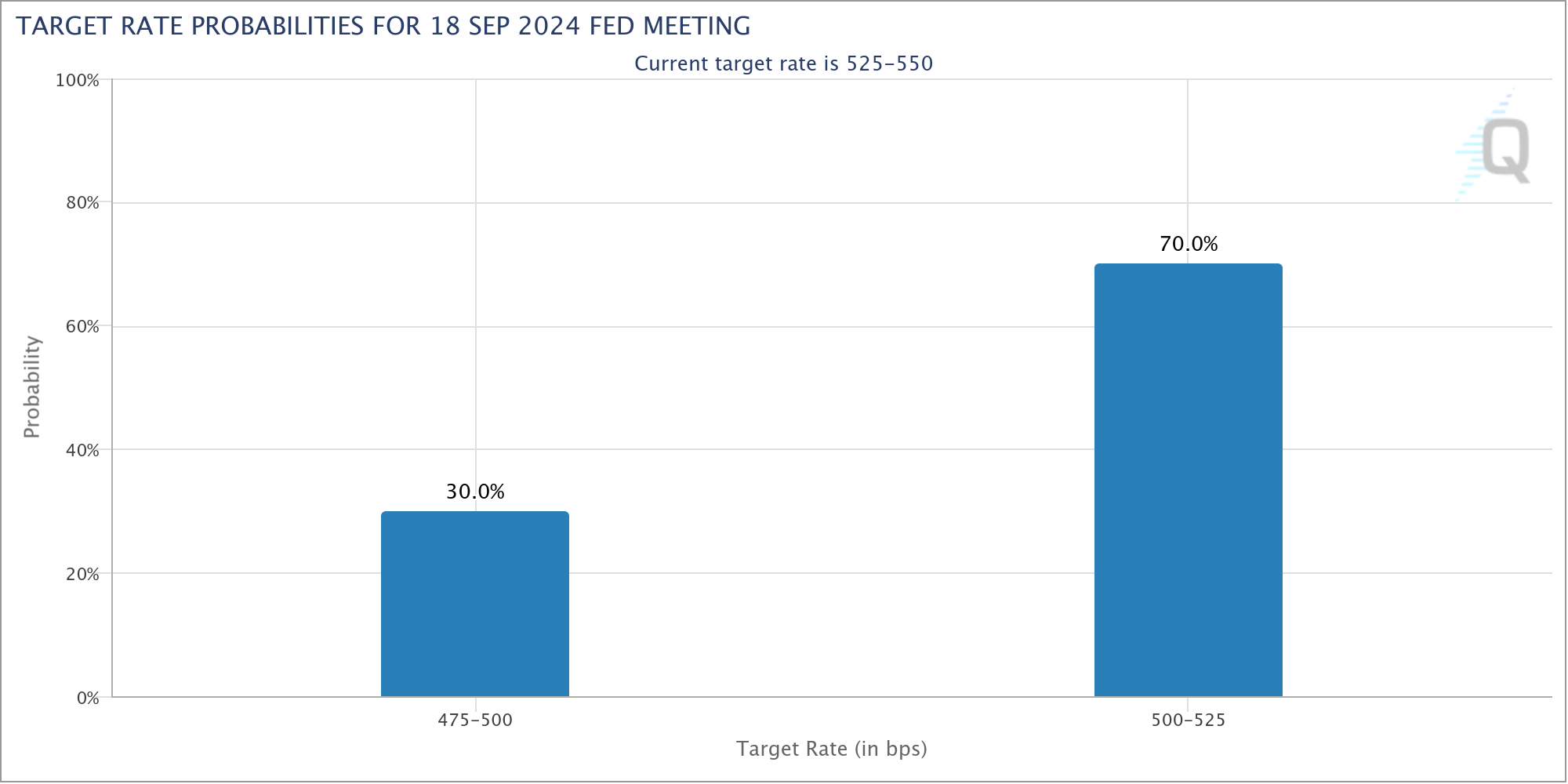

A lot of this whipsaw effect was due to Fed speakers. Williams was the first up, and he chose to talk the market down from pricing in 50bps in September.

Waller wasn’t much better. Goolsbee had some dovish moments, but he’s Goolsbee so it didn’t matter too much.

We finished the day back to 70/30 25/50bps on the next cut.

Where Are We Going?

I’ve been urging calm again all week which has proven not to be the right course of action. It would have been much better to panic early, right when they released that cold ISM Manufacturing print.

I still don’t really understand why the ISM Manufacturing print set us off. I’ve laid out pretty clearly why manufacturing isn’t all that meaningful to the economy anymore:

It’s only 10% of GDP.

It’s been “recessionary” for over a year now.

Then, on Thursday, a “good” Services report wasn’t enough to save us.

Today… well, you all know what happened.

It’s alarming how identical every one of these charts looks.

This is what happens in a bear market. Correlations go to 1, as they say, and everything moves together.

The place to hide out has been bonds, which have crushed all week.

(A 2.84% gain is crushing in the bond world)

We are in a tough spot. We didn’t panic early, nor did we hedge on the highs, and now we are faced with the prospect of reducing exposure on the (current) lows.

The truth is that the job market and the economy are deteriorating. They have been for some time.

It’s only really beginning to show up in the data now.

I previously (in 2022) wrote on Twitter that the Fed needed to trigger a recession to lower inflation.

That pessimistic forecast hasn’t come to pass. We have brought inflation down significantly while the economy is still growing.

But the market is trading like it needs to see 50bps to believe we will avoid a recession.

After considering the totality of the data, I’m starting to think they might be right.

I previously wrote that we needed to see the Fed cut in July. I believed that we needed to cut before the job market began to deteriorate.

The job market is beginning to deteriorate.

I’ve written previously that once the data has clearly deteriorated, it is usually too late. At that point recession is here, and the markets have adjusted.

Markets also have a good nose for recession, starting to fall before the data truly deteriorates.

This week feels eerily similar to what I see in these charts.

The mark of a good trader is the ability to recognize when you’re wrong. The mark of a great trader is being able to flip and take the other side (correctly) in those moments.

I’ll be mulling that over this weekend.

If you like what you read here please subscribe.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here.