Is The AI Trade Over?

The "Show Me" Phase

AI Drag ≠ AI Doom (but the market just raised the bar)

Friday was one of those sessions where the index move doesn’t look dramatic until you open the hood and realize half your watchlist is bleeding. The S&P finished down ~1.1% and the NDX was closer to -1.9% , but momentum got hit hard because the damage was concentrated right in the AI nerve center: Broadcom and Oracle.

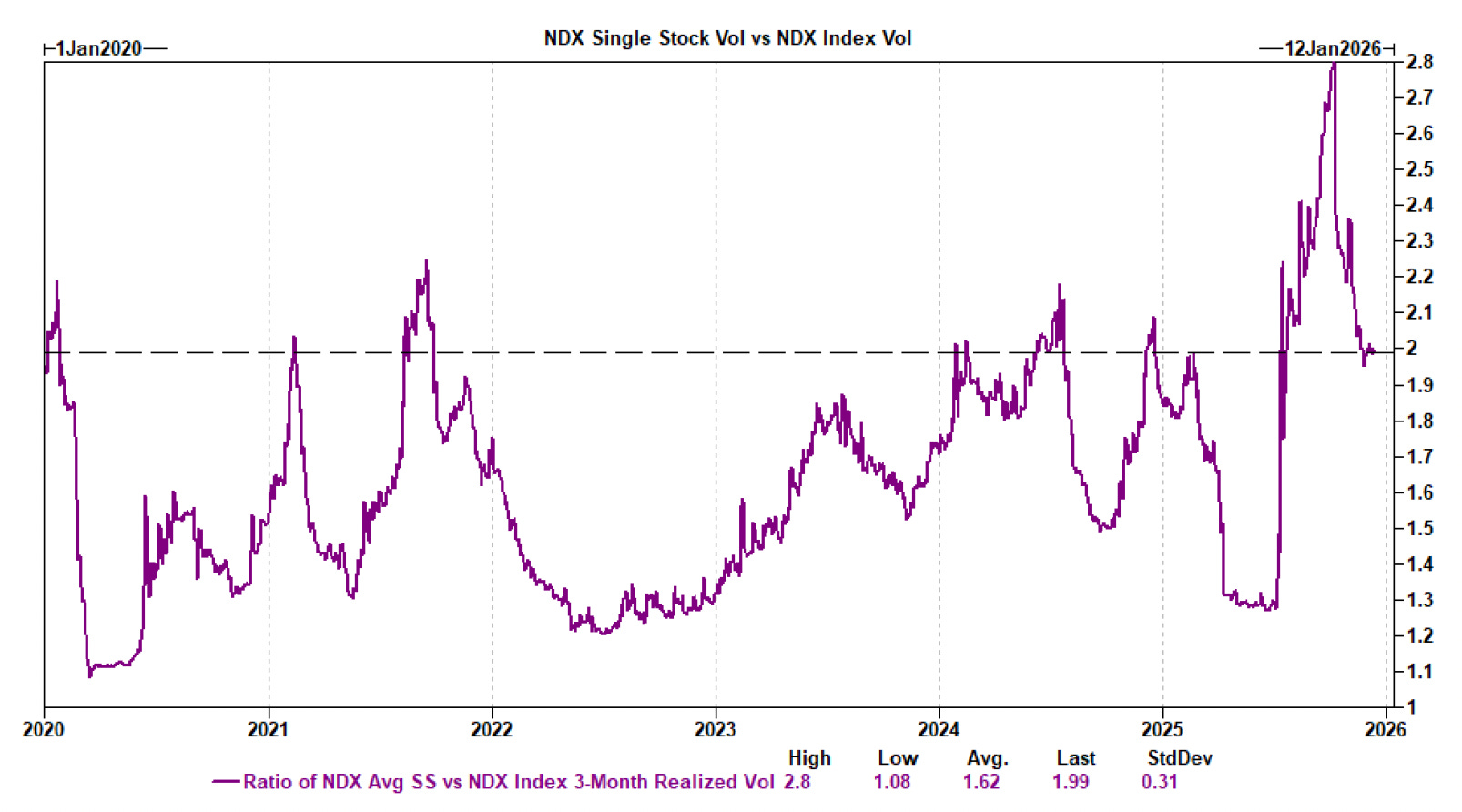

Part of why this keeps happening: the market is living in a world where single-stock volatility is doing its own thing while index vol stays weirdly contained. Over the last three months, the average single stock in the NDX has been about 2x as volatile as the index. So you can get a day where the market feels like a bar fight, while the index barely moves.

That’s good news for trader but not-so-great news for people who are “buy and hold” the wrong names.

Speaking of wrong names this week…

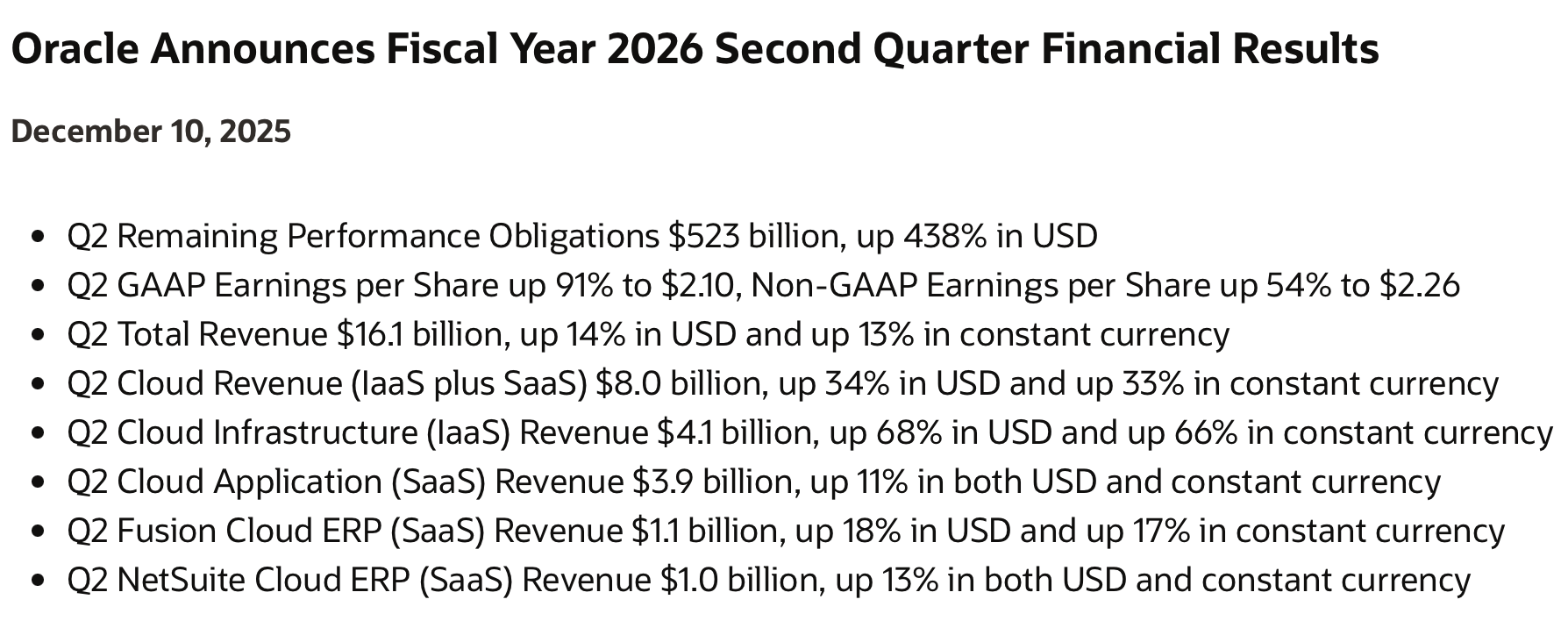

Oracle: the market stopped clapping for “spend”

Oracle reported earnings Wednesday and while they were “fine” on the surface they disappointed on the whole. They grew revenue slightly less than analyst expectations, they guided higher on Capex spend for 2026, and also pushed out the timeline for that Capex spend to pay for itself.

Oracle’s sin was spending in a way the market no longer wants to reward. The interpretation from the market was blunt: ORCL “spent too much” (raised FY26 capex), and the market is no longer rewarding off-balance-sheet spend.

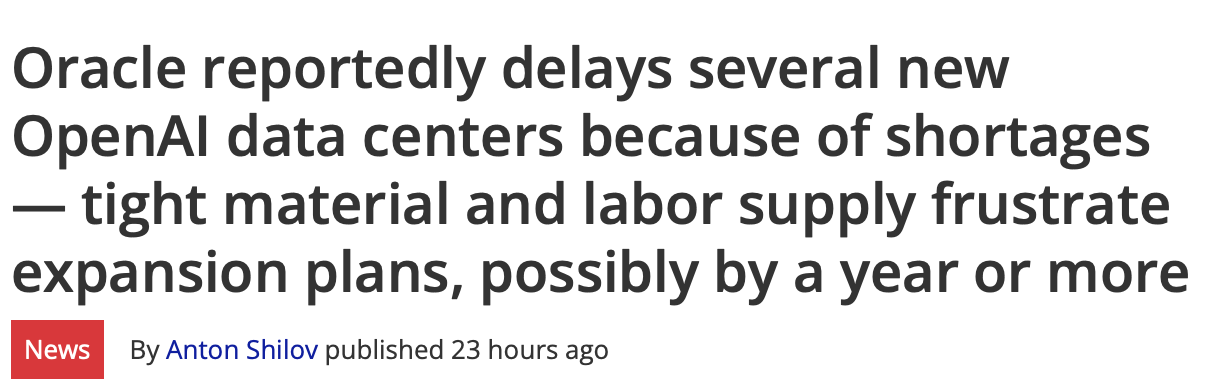

And then on Friday we got the extra gasoline: a report of Oracle datacenter pushouts (even if it was refuted later).

For most of the last few years “Capex up” has been the goal. Investors wanted to see major AI-related build outs happening and they rewarded stocks accordingly. But ever since Meta got punished for their major Capex increases the tone has been different, and Oracle found out just how different. We are in the “show me” phase of the build out.

Investors want to see roic (return on invested capital) increases, not ic (invested capital) increases.

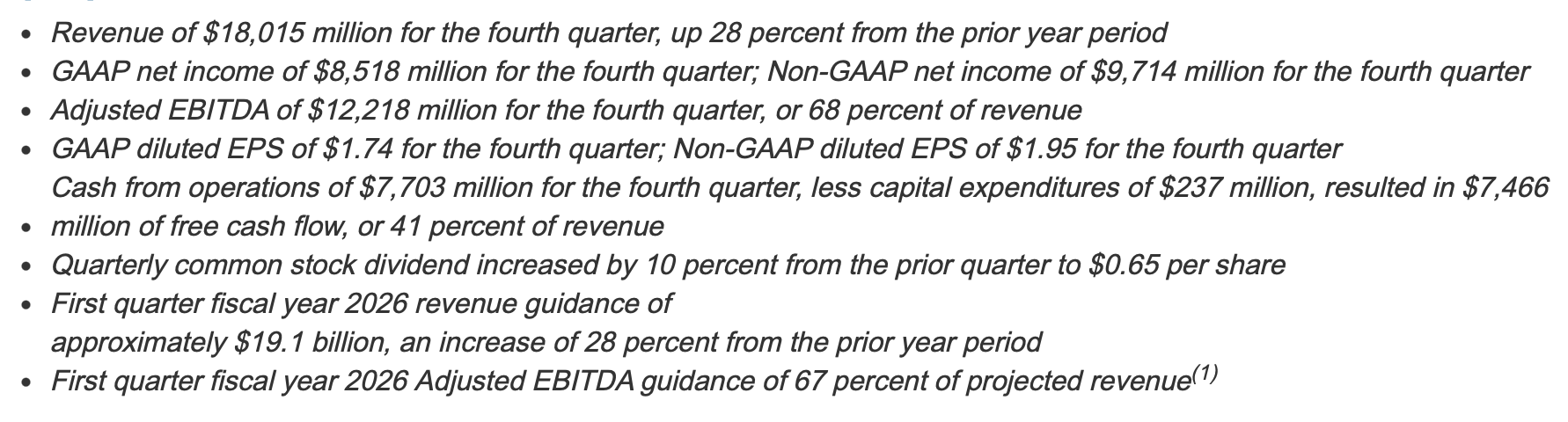

Broadcom: the numbers were fine… expectations weren’t

Broadcom is the cleaner example of what’s happening to the whole AI complex: the direction can still be right, but the setup can be wrong.

The headline numbers were objectively constructive. AVGO beat, guided Q1 above expectations, and signed a 5th customer (who a Broadcom officer said wasn’t OAI) for its custom AI accelerator. They also talked about significant real demand in the market. The company noted Anthropic placed an additional $11B order for FY26 .

And yet… the stock got hit anyway because the market wanted the one thing that mattered most for a crowded AI winner: the forward declaration. Management wouldn’t give an FY26 guide yet , and they didn’t update their prior 40%–60% FY26 AI revenue growth commentary, despite saying AI revenue is accelerating (65% in FY25 and ~100% in Q1) . In other words: the facts were good, but the incremental move in expectations (the second derivative) wasn’t good enough relative to positioning.

Good news can still be a sell if it’s “good” against reality but “not good enough” against expectations.

So… is the AI trade “done” for a while?

I don’t think Friday answered that. But it did tell us a few things. It told us what questions the market is asking now, and it told us how stretched positioning had become.

Friday felt to me like a degrossing into low-liquidity. Unfortunately, these degrossing days don’t tell us much about the future direction of the trade, so we are left waiting and watching. Sometimes these degrossing days sharply V-reverse (although that’s usually due to news), sometimes the trade moves on from the local losers (IE AVGO and ORCL get left behind and the hot money rolls into the perceived winners) and sometimes these days mark the start of a months-long drawdown or consolidation.

Not very helpful unless we can parse them apart.

Here’s how I’m trying to parse that question.

3 Things to Watch and Consider

The Core Infrastructure: The infrastructure names have been strong for years and the market still believes in the them, it’s just getting more selective. While Broadcom and Oracle stumbled on high expectations, Nvidia remains the anchor. The demand signal for Blackwell remains “off the charts,” confirming that the hyperscaler capex cycle is still in the early innings. The market is punishing inefficiency (spending without immediate return), not the infrastructure trade itself.

The “Broadening Out” (Software & Services): The most bullish signal this season wasn’t in chips, it was in monetization. I wrote previously about the “three pillars” of the AI trade, and how we needed to see the software/services segment bring in revenue. Well, we are finally seeing AI capex translate into that revenue. AppLovin and Meta proved that better models immediately yield better ad conversions. CrowdStrike showed that AI is non-discretionary for security, and Google’s cloud re-acceleration confirms the enterprise is moving from “testing” to “deployment.”

Dispersion (The “Good” Decoupling): In a panic, correlations go to 1.0. Everything gets sold together. The most important signal to watch next week is whether the “winners” can ignore the “losers.” If Oracle or Broadcom have another red day, does Nvidia/Goog hold up? Does AppLovin stay bid? We want to see a market that punishes specific failures but rewards specific execution. If the baby stops getting thrown out with the bathwater, the correction is over.

And to tie it back to what you felt in your P&L: into year-end, this also looks like positioning and risk management layered on top of the fundamental questions. There’s been a sense that investors are trimming the “AI winner” complex and playing more defense around ROI/Capex concerns.

My Vibe

Friday wasn’t a signal that “AI is over”; it was a signal that “AI has to re-prove itself.” The market just told us that spending (Oracle) is no longer a bullish signal unless it creates immediate profit, and that “good” earnings (Broadcom) are a sell signal if you’re priced for perfection or if any side-bars introduce doubt (No FY26 guide, “fifth customer” mystery).

One critical detail: Volatility didn’t panic. Despite the S&P realizing 2x the expected move, implied volatility barely budged, and pros were heavy sellers of vol by the afternoon.

That’s the single biggest point in favor of this being about “rotation” rather than an “ending” of some kind.

The Bottom Line: The AI trade isn’t dead, but the “blindly buy the basket” phase is. We are moving from investors being rewarded for holding any form of AI Beta (everything goes up) to Alpha (stock selection matters).

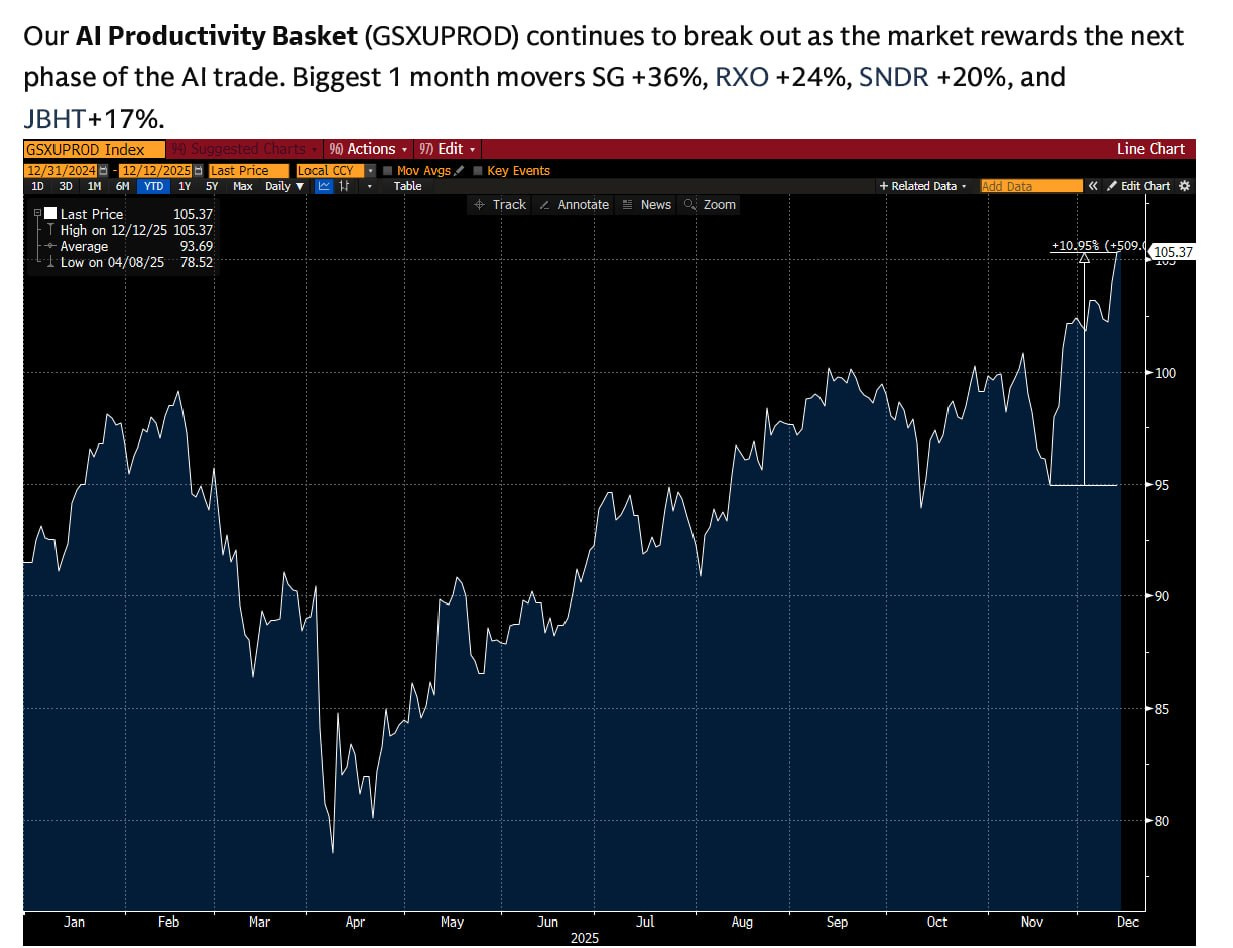

This is the most interesting chart I saw this week because it shows so clearly that the “AI Beneficiaries” basket has been crushing for the last two months even while the “AI Infrastructure” names have lagged.

I think the takeaway here is clear: you want to be more disciplined about hunting for value in the infrastructure names that have already won a lot, and look for beneficiaries of the AI build out.

Gemini 3 Pro is so good. For most business use cases the “AGI” is already here, it just isn’t evenly applied yet.

I’m digging into the private equity companies and have initiated small positions on them (BX/APO/KKR). I believe they should be beneficiaries of a reaccelerating economy and they will be ruthlessly efficient about applying AI to their businesses.

Private equity names have been beat down for a while and this might represent a good entry point.

I’m also nibbling on SAAS providers like TEAM/CRM and potentially others. They have also been quite beaten down because they’ve been widely considered to be “AI losers” but I think there is a good chance that enterprises will get their first workable “AI Integrations” through the providers they already work with.

Final Thought: The “Easy” Trade Is Gone

If there is one takeaway from this week, it is that the “Blind Buy” era of AI is over. The tide is no longer lifting every boat; it is drowning the ones with holes in them (like Oracle’s spending) and lifting the ones with engines (like AppLovin’s cash flow).

This dispersion creates volatility, but it also creates opportunity for active management. I expect the gap between “winners” and “losers” to widen significantly into year-end. That is exactly the kind of environment we want to be in.

Good luck out there, let’s see what Monday brings.

Disclaimer: The information provided here is for general informational purposes only. It is not intended as financial advice. I am not a financial advisor, nor am I qualified to provide financial guidance. Please consult with a professional financial advisor before making any investment decisions. This content is shared from my personal perspective and experience only, and should not be considered professional financial investment advice. Make your own informed decisions and do not rely solely on the information presented here. The information is presented for educational reasons only. Investment positions listed in the newsletter may be exited or adjusted without notice.